By Robert Serenbetz, from the Multi-Asset Solutions Team at New York Life Investments

Slowing economic growth has weighed on corporate sales and profits. The MAS team believes further negative guidance will likely prompt market volatility throughout the rest of the year. As a result, we have reduced our equity exposure, favoring investments less exposed to wage pressures, global trade disruption, and manufacturing weakness.

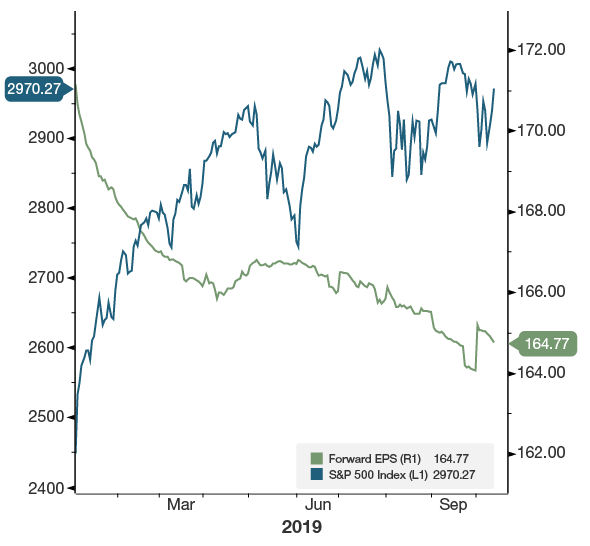

Weaker earnings are not reflected in S&P 500 Index valuations

{kind=link}

Source: New York Life Investments Multi-Asset Solutions team, Bloomberg, S&P. As of 10/15/19.

Analysts already anticipate a weak corporate earnings season. Current FactSet estimates suggest that S&P 500 corporate profits may decline -4.1% versus this time last year. Yet the price of the S&P 500 Index doesn’t yet reflect this weakness. Why? Expectations for 2020 profit growth remain high – upwards of 10%.

We are concerned that S&P 500 Index earnings may display weakness beyond the third quarter 2019. September’s weak ISM reading for both services and manufacturing (47.8 and 52.6 respectively) suggest that economic growth will continue to slow. Meanwhile, the yield curve and payrolls are sending worrying signals of an impending recession. We believe investors and analysts may be too optimistic on earnings-per-share growth in the year ahead.

{kind=link}

Source: New York Life Investments Multi-Asset Solutions team, Bloomberg, S&P, Institute for Supply Management. As of 10/15/19.

What’s causing weak earnings?

The late cycle economic environment lends itself to growing margin pressure primarily through rising labor costs, but the trade war has also exacerbated these pressures. Weaker than expected inflation data suggests that a substantial share of tariffs is being absorbed across supply chains via margin compression and currency market adjustments.

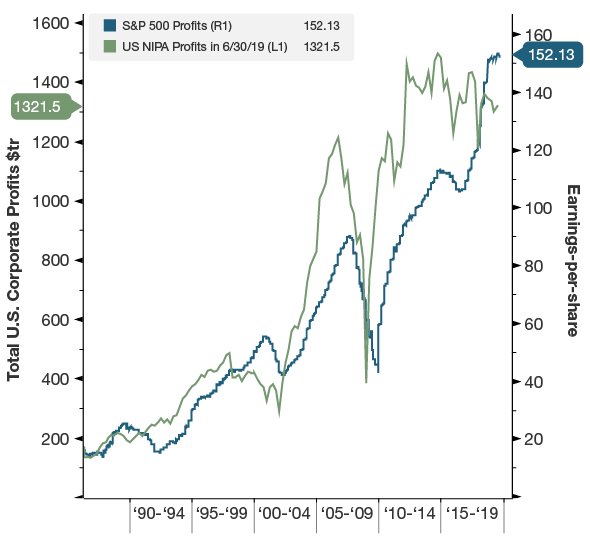

The National Income and Product Accounts (NIPA) profits, which include a broader universe of companies in the US economy than the S&P 500, have already peaked, and appear to be on the decline. Importantly, NIPA profits tend to lead S&P profits. We expect that current divergence forewarns that S&P 500 profits may weaken.

{kind=link}

Source: New York Life Investments Multi-Asset Solutions team, Bloomberg, S&P, Bureau of Economic Analysis As of 10/15/19.

Unsurprisingly, small-cap earnings are fading. Reported profits are down nearly 9% on a trailing basis – the worst decline of this cycle. We expect declines to continue based on current economic fundamentals.

The Fed is lowering rates, won’t that help?

We are skeptical that lower interest rates will be able to further support equity valuations or spur a significant pickup in growth. This is in part because interest rates are already low, and because we don’t expect bond yields to fall significantly further without a catalyst. That means that any weakness in forward S&P 500 is likely to prompt a decline in the index’s price to earnings ratio.

Bottom line

Investors’ continued optimism about corporate earnings for the S&P 500 doesn’t fit with our take on the weak global economic picture and the broader late cycle corporate profit trends. This is the key reason why we continue to think U.S. equities will face more trouble before the end of the year.

In our portfolios we have reduced equity exposure, favoring investments less exposed to wage pressures, global trade disruption, and manufacturing weakness. These investments tend to be in defensive (non- cyclical) sectors. They also tend to be higher in quality with strong balance sheets and stable earnings growth.

This material represents an assessment of the market environment as at a specific date; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

This material contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

“New York Life Investments” is both a service mark, and the common trade name, of the investment advisors affiliated with New York Life Insurance Company.