Life Insurance

Andrew Kail, Head of Financial Services at PwC, said:

“The financial services sector is arguably the most internationally competitive industry in the UK. It’s essential that London and the regional centres across the country collectively remain among the pre-eminent international hubs for financial services and global business.

“There are understandable concerns around the shockwaves created by Brexit alongside dealing with the impacts of regulation and technology. Addressing how these issues manifest themselves must be at the heart of firms’ contingency plans over the next six months.

“As the Brexit negotiations continue companies across the sector – who are providing vital services to customers, corporates and governments – have the chance to galvanise themselves and their clients against any potential fallout. This must be underpinned with prudent planning and skilful execution of their plans.”

Amid weak volumes growth and rising costs, profits in the sector as a whole were flat in the quarter to September, for a second successive quarter. Several sectors saw profits fall, with investment managers reporting the steepest drop since the financial crisis. Overall profitability is expected to grow in the three months ahead, but to continue declining for investment managers and building societies.

Investment intentions for the year ahead cooled over the three months to September. Financial services firms plan to raise spending on marketing and IT, although the pace of growth in IT spending is expected to slow, but they also expect to cut back land and buildings and vehicles, plant & machinery.

Firms cited a broad range of reasons to invest, including efficiency improvements, statutory legislation and regulation, and to provide new services. The main brake on investment spending remains uncertainty about demand and inadequate net returns.

Technology is altering recruitment, with over half of firms saying changes in headcount were being driven by technology-driven efficiency gains. Regulatory compliance, business transformation and Brexit were all seen as more important for recruitment strategies than the expected level of demand for services.

Meanwhile, the UK’s broader economic outlook remains fairly subdued, with GDP growth held back by weak household income growth and the impact of Brexit uncertainty on investment. For more detail, see our June economic forecast.

General Insurance

Insurance Brokers

Investment Management

Key Findings:

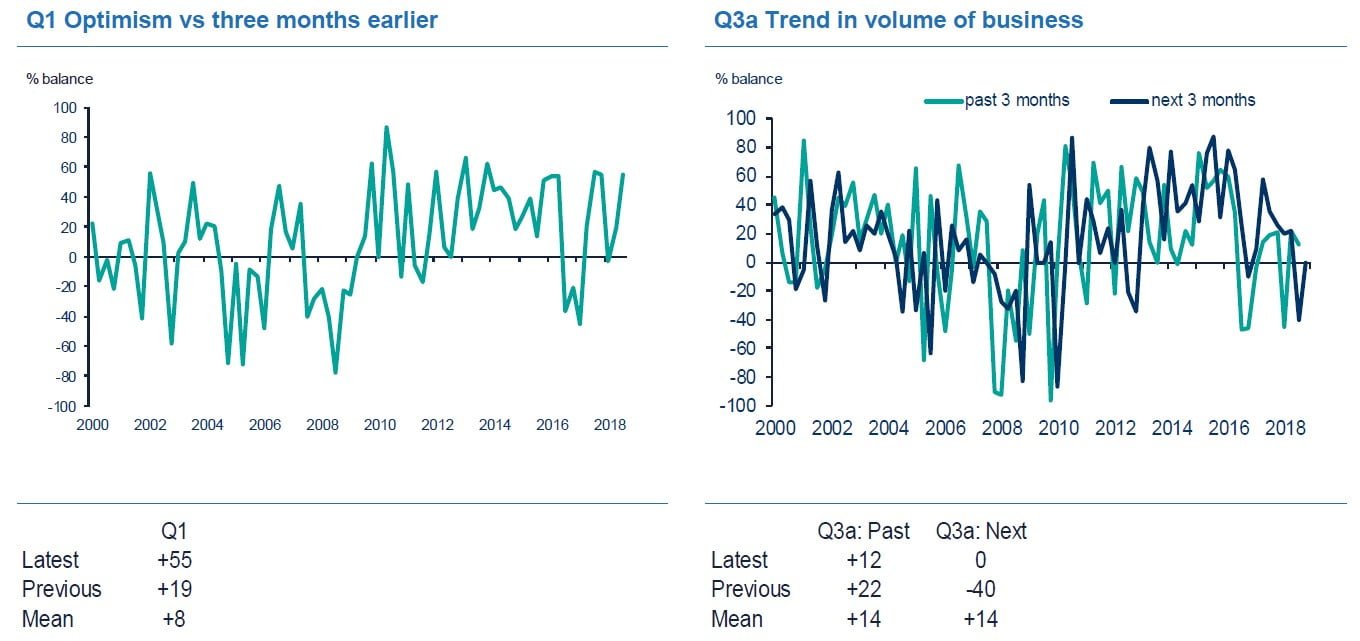

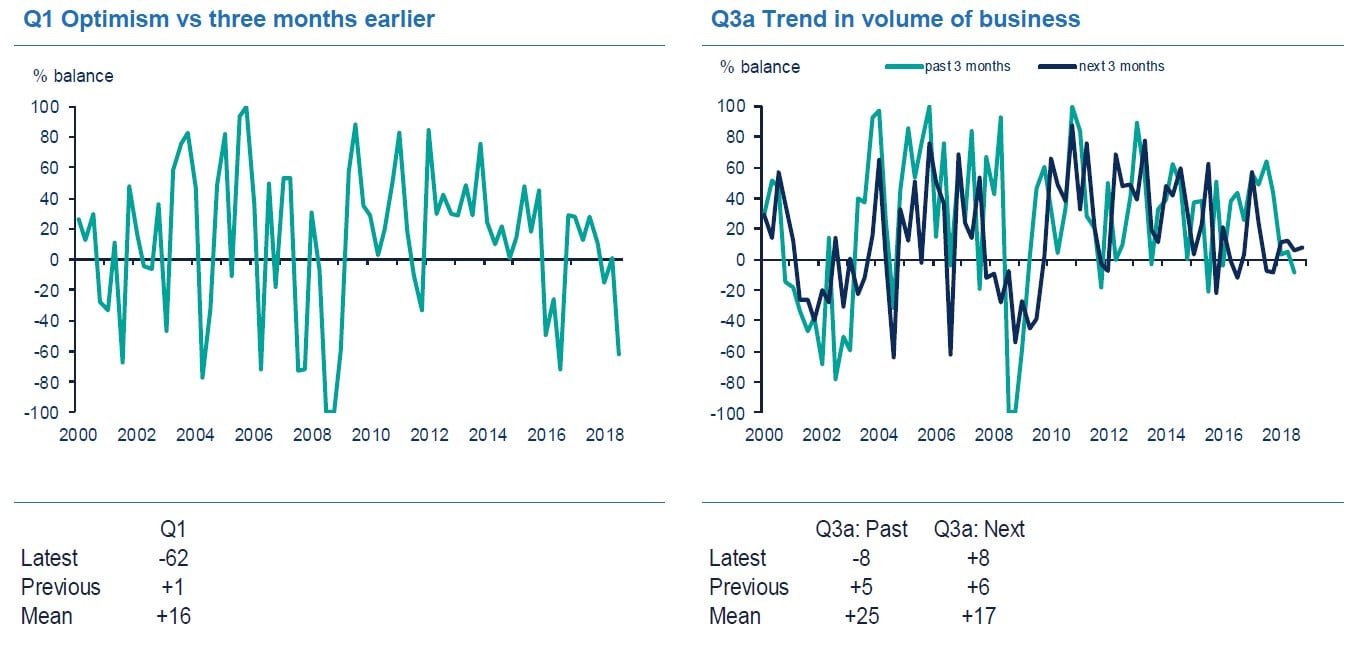

- Optimism in the financial services sector dropped sharply (-30%), the tenth quarter of declining sentiment in the last eleven quarters (the exception was the first quarter of 2017). This marks the longest period of flat or falling sentiment since the global financial crisis of 2008

- 6% of firms said they were more optimistic about the overall business situation compared with three months ago, whilst 36% were less optimistic, giving a balance of -30% (compared with -4% in the quarter to June). Barring December 2016 (-35%), this was the steepest drop since the financial crisis (-34% in March 2009)

- 23% of firms said that business volumes were up, while 11% said they were down, giving a balance of +12% (up from -4% in the quarter to June)

- Looking ahead to the quarter to December, business volumes are expected to be flat: 15% of firms expect volumes to rise next quarter, and 14% expect them to fall, giving a balance of +1%, the weakest since December 2009 (-13%)

Incomes, Costs and Profits:

- Overall profitability was flat in the three months to September, with 20% of firms reporting that profits had increased and 21% saying they fell, giving a balance of -1%. This followed a similar picture in the previous quarter (+4%), but profits are expected to improve in the next three months (+16%)

- Income from fees, commissions and premiums was largely unchanged (+1%), but income is expected to fall in the quarter ahead (-13%)

- Income from net interest, investment and trading fell (-13%), with a slight increase expected in the next three months (+5%)

- Total operating costs rose (+17%) and average costs increased at the fastest pace in four years (+21%). Both total costs and average costs are expected to rise next quarter (+16% and +15% respectively).

Employment:

- 20% of financial services firms said they had increased employment, while 17% said that headcount fell, giving a balance of +3%, disappointing expectations (+15%)

- Numbers employed are expected to hold steady (0%) next quarter.

Investment over the Next 12 months:

In the year ahead, financial services firms expect to increase spending on IT and marketing, but to cut back on other forms of capital spending:

- IT: +49% (a drop from +70% in the quarter to June)

- Marketing: +31% (a rise from +20% in the quarter to June)

- Vehicles, plant and machinery: -15% (down from -9%)

- Land and buildings: -18% (down from +5%)

The main reasons for authorising investment are cited as:

- To increase efficiency/speed (75% of respondents)

- For replacement (68%)

- Statutory legislation and regulation (66%)

The main factors likely to limit investment are cited as:

- Uncertainty about demand or business prospects (60% of respondents)

- Inadequate net return (55%)

- Shortage of labour, including managerial & supervisory staff (26%).

Business Expansion Over the Next 12 Months:

The most significant potential constraints on business growth over the coming year are:

- Level of demand (58% of respondents)

- Statutory legislation & regulation (52%)

- Availability of professional staff (48% – a survey record high).

Recruitment and Skills in Financial Services:

- Over two-fifths (42%) of firms had found it more difficult to recruit and retain workers over the past year, but half had not (50%). In response, various actions are being taken:

- Change advertising (25%)

- Invest in artificial intelligence and automation (21%)

- Provide training (12%)

- Increase wages (7%)

- The most acute skills shortages in the year ahead will be felt in the recruitment of workers in:

- IT (72%)

- Compliance/audit (35%)

- Risk management/actuarial/claims (34%)

- Firms said changes in headcount were being driven by:

- Technology driven efficiency gains (58%)

- Business transformation (55%)

- Regulatory compliance (51%)

- Brexit (30%).

For more trends in fixed income, visit the Advisor Solutions Channel.