True, the current market carnage reflects more than just rising U.S.-Sino tensions. A hawkish Fed, a backup in yields, fears surrounding peak earnings, Italian credit problems, U.S.-Saudi tensions—all of these variables have knocked the global markets for a loop this month.

But these factors are more cyclical than structural, and therefore are not as threatening to the capital markets over the medium term as is the fundamental rupturing/reordering of U.S.-Sino relations. China would rather deal with a cyclical slowdown, or even a recession, than have to adjust/revamp its economy in lieu of a tectonic shift in the U.S.-led global economic order of the past 70 years.

Remember, modern-day China grew up and prospered in the western liberal order the administration appears to be bent on dismantling. Prior to the administration, America’s approach to China was grounded in the belief that as China prospered and flourished, as millions more people achieved middle-class status, China would become more like the U.S.—or more liberal and pluralistic. Through greater economic convergence with the West, China would become a “responsible stakeholder” and embrace market and Western economic principles.

The gamble, however, appears to have failed. China, to a large degree, has played by its own rules. Noncompliance with many provisions of the World Trade Organization, championing large state-owned enterprises, intellectual property right violations, unfairly titling the domestic playing field against foreign companies—all of these characteristics suggest that China was never really serious about becoming the partner the West desired.

While the last quarter century in the U.S. has been about engaging China, that era is over. The two largest economies in the world are now rivals—a seismic shift the capital markets are only now beginning to price into assets. Recall that at the beginning of the year, the consensus was that Washington would push China hard on trade, accept some limited and symbolic wins, declare victory and move on. That scenario looks like a pipedream now—the U.S. and China seem destined for a long cold war.

Aftershocks

The adversarial stance of the U.S. toward China is just what Beijing can ill afford at the moment, in our opinion. Real growth is slowing. Inflation is on the rise. Private- and public-sector debt levels remain elevated. The brutal swoon in Chinese equities has undermined consumer confidence and wealth. Business spending has been trimmed owing to rising costs related to higher prices and rising wages. Offshoring among domestic and foreign firms is on the rise. The nation remains stuck in “middle class” status, with diminished odds of moving up the development ladder given the mushrooming confrontation with the United States.

In addition, with growth slowing and the government in the “whatever it takes” mode to keep the expansion alive, the country’s goal of “high-quality” economic development has been pushed to the sidelines. Structural reforms (including financial sector liberalization, cracking down on the shadow banking industry, opening the capital account, internationalizing the currency) remain a priority but have been downgraded as Beijing adjusts to a global trade and financial environment far more inimical to the long-term interests and goals of the nation.

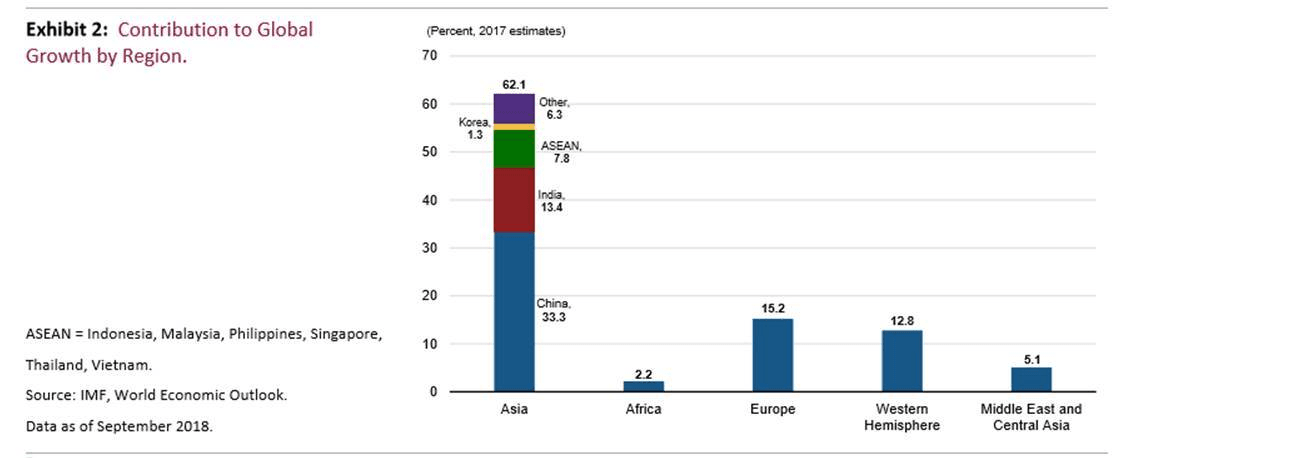

The upshot from all of the above: much-weaker-than-expected real growth from China over the near term, compounded by long-term challenges tied to a more combative United States bent on changing the structure of global trade and investment. This scenario is contributing to the current level of market volatility and intense downside pressure not only on Chinese equities but also on global equities. Remember: With China contributing to just over one-third of global growth last year, what happens in China doesn’t stay in China (Exhibit 2).

At risk to a prolonged U.S.-China trade war: real economic growth and earnings prospects in China, the United States and the world at large.

In the end, it’s finally dawning on investors that China confronts not only a much more fragile economic climate than previously thought, but also something perhaps even worse: the reconfiguring of the global economic order that has been so immensely beneficial to China’s development and emergence.