While the article notes it’s too soon to know whether this is the beginning of a bigger shift toward value, it offers the following arguments supporting the end of value’s “dark winter:”

- Rising rates are usually good for value—they push up the discount rate that investors apply to future cash flows, so the valuations of growth stocks dip more than that of value stocks.

- Earnings and valuations are out of sync—”By definition, the earnings growth of value stocks tends to be lower than that of growth stocks. As a result, value stocks typically trade at a discount to growth.” But lately, the discount is much deeper than usual, it says, adding, “If you believe that earnings matter for stock valuations, this discount appears unjustified. When it corrects, we believe value stocks will post strong performance.”

- Widespread sector opportunity—”we’re finding underappreciated stocks today in diverse sectors from consumer discretionary to technology to materials.”

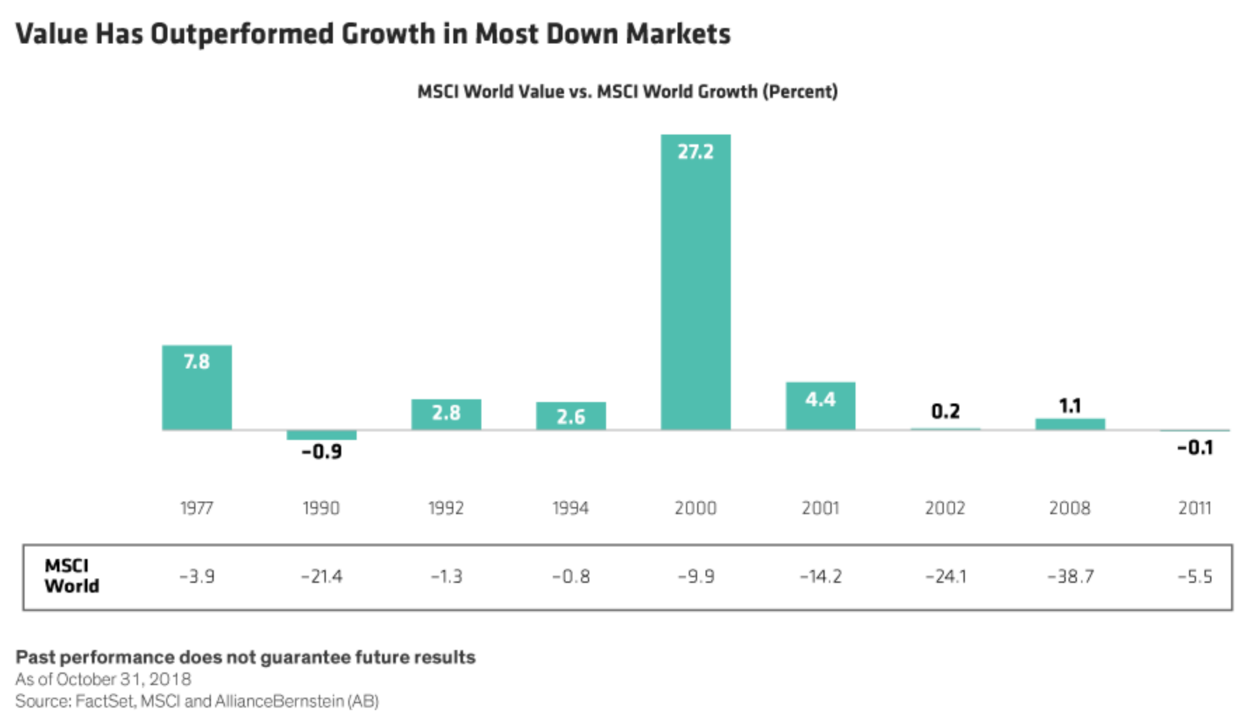

The article notes that value has outperformed growth in most down markets and suggests that these stocks could protect investors from volatility because “with cash-flow yields so high today, cheap stocks of companies that generate ample cash have a helpful buffer against further steep falls in valuation.”

Volatility also presents opportunities for value investors, the article concludes: “When markets are falling, stocks of strong companies also get hit. Investors who swim against the tide to buy cheap stocks with solid and underappreciated businesses can take contrarian positions to capture powerful returns in a potential value equities recovery.”