According to recent research from Robeco Asset Management’s David Blitz: “hedge funds have hitched their wagon to stocks with large equity-price swings—a misguided strategy over the long haul.” These findings were reported in a recent Bloomberg article.

In an interview, Blitz said, “The fact that hedge funds are positioned like investors in high-volatility stocks, this does not contribute positively to their returns.”

![]()

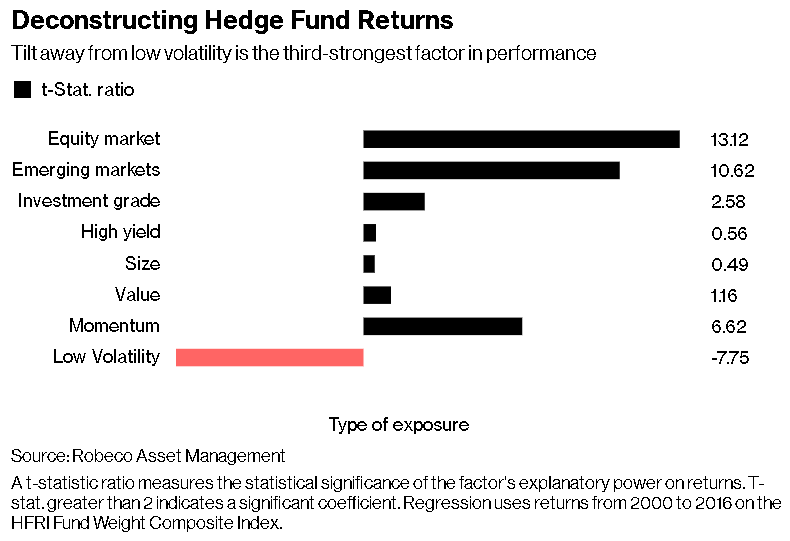

Blitz says that moving away from a low-volatility factor represents one of the “top three drivers of fast money performance.” While the article acknowledges that the low-volatility factor has periods of underperformance, quant investors point to the long-term success of the strategy (since 2000, the article reports, the factor has outperformed the S&P 500 by 119 percentage points).

But tracking the low-vol factor can be tricky, and the strategy can suffer from overcrowding. “In 2016,” the article reports, “a volatility blow-up was blamed on investors who piled into the strategy and then rushed for the exits.” That said, the article notes that hedge funds are well positioned to take advantage of the low-vol factor since they have “fewer leverage constraints, so can buy the boring stocks, deploy debt, and post higher returns.”

For more trends in fixed income, visit the Advisor Solutions Channel.