Inflation is now at a 40-year high with a 7% gain year-over-year in the U.S., and inflation has also been trending higher in the Eurozone, hitting a record 4.9% in December. T. Rowe Price offers a solution for investors looking for pockets and opportunities of performance in high inflation environments within emerging market currencies.

Inflationary pressures are pushing central banks worldwide to respond by tightening their fiscal policy, creating a difficult investing environment for bonds, while pandemic woes and supply chain issues dampen economic growth, write Kenneth Orchard, portfolio manager in the fixed income division at T. Rowe Price, and Onur Uncu, quantitative analyst at T. Rowe Price in a recent white paper.

“Struggling growth coupled with persistent inflation demands a creative approach to bond portfolio management,” they write.

Emerging market (EM) currencies, particularly countries that are big exporters of commodities, generally outperform in inflationary times. The reason is two-fold: Inflation causes commodity prices to rise, and emerging markets can often offer larger opportunities for growth than their developed counterparts.

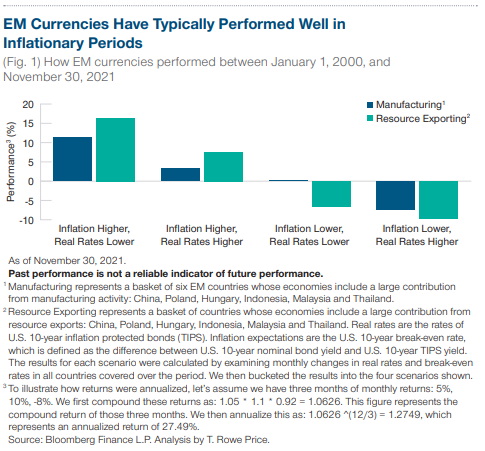

The active management firm has demonstrated the correlation between higher performance of EM currencies, especially of countries that are commodity producers, during times of expected inflation in the U.S. The authors compare the performance of EM currencies against expected high inflation and U.S. real rates, which usually reflect economic growth expectations.

Image source: T. Rowe Price

EM currencies performed best in times of rising inflation expectations and falling real rates, or times when growth was expected to be slowing, though they still performed strongly when both inflation and interest rates were rising.

“This suggests that resource-exporting EM currencies can improve bond portfolio returns during inflationary periods irrespective of whether real rates are falling or rising,” the authors write.

Taking a look at how EM currencies performed over the course of the COVID pandemic from May 1, 2020 to November 30, 2020, they found that EM currencies did well during times of increasing inflation expectation and decreasing growth. EM currencies, however, did not perform well during inflationary times with rising real rates, but this is most likely due to Federal Reserve fears in markets recently, a reaction that the authors believe may have been overdone when compared to historical performance.

The authors are careful to caution the risks in investing in EM currencies. “EM currencies tend to behave like ‘risk on’ assets and suffer in a sharp risk‑of environment along with credit. As such, we believe they should be treated as a substitute for credit risk in portfolios—not an enhancement,” they write.

For more news, information, and strategy, visit the Active ETF Channel.