By David Dziekanski, Portfolio Manager and Michael Venuto, CIO, Toroso Asset Management

Embrace the Chaos

The results of fiscal policy are starting to come through the economist statistics, and they appear to be very strong. We are going to get some sort of infrastructure bill, and likely a less than anticipated tax increase. Now that we are a year past the initial Covid crisis and possibly halfway through our next market cycle, investors are having mixed perspectives and emotions. If you are waiting for the proverbial shoe to drop you might need to keep waiting. If you take anything away from this commentary, we hope it’s this: things actually look great in the economy on a macro basis. Potential market outcomes in the next 2 years could be anything from absolutely spectacular to a never-ending risk of disaster (potentially even a single liquidity crisis buried in the depths of some overleveraged family office). To the average investor, last year proved that the market and the economy are two very different things. Strength in one does not always carry through to the other, although we expect it will over the coming months. We are likely about to climb an insane wall of worry for the next few months, with a mounting list of concerns that could derail this.

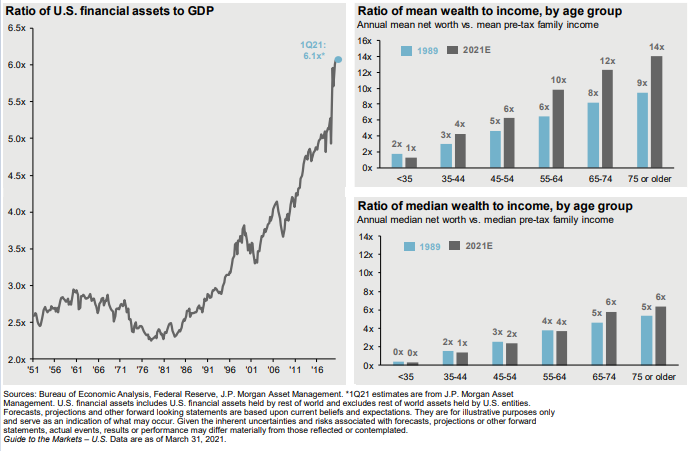

Some investors have made more wealth in the past year than they could have ever imagined. Others have FOMO from not making more, and a whole lot were completely left on the sidelines, furthering socioeconomic inequality in our society. Even policies meant to help the masses ended up in the pockets of the few. Regardless, the money is in the system. We are left with a K shaped recovery for both companies and households, except the upper right portion of the K has gone parabolic.

Structural Market Thoughts:

- Trust in establishments of all kinds is eroding. In the tech rally of the late 90’s and early 2000’s, we looked to our companies and institutions to provide us with guidance and protection. The government supported its constituents, the Federal Reserve protected the economy for the average American, and the news was a trusted source. We believed the government had our best interest in mind. Fast forward 20 years, and the freedom of information brought by the age of social media has ruined most trust in the establishment; enter blockchain.

- Most market participants have figured out what the QE means for assets, and no one wants to fight the Fed anymore. Retail is playing it in the options market. Why not bet big knowing the Fed has your back on most financial assets? Every time there is volatility, there is inevitably some portion of the Fortune 500’s and the 1%’s that get even better access to credit than they did before through lower interest rates. Banks are eager to lend at unheard of rates, giving these entities and individuals ample cash to deploy right when fear and volatility peaks. It’s ironic that when we spent so much time restricting which individuals and entities have access to credit in an effort to protect the “little guy,” we unintentionally put that same group at a significant disadvantage when credit is most useful: in times of market volatility, not at market highs. When volatility spikes, the only loans that appear safe are those belonging to the 1% and Fortune 500. There goes another layer of the middle class. The retail mindset is to try and get there before the big money comes in. There’s no bigger oligopoly in the world than the democrats and republicans in the United States, and politics and markets are as intertwined as ever, further emphasizing the case for cryptocurrencies.

- Echo chambers are everywhere. Almost all echo chambers believe their collective viewpoint is correct, rather than others. Most echo chambers have gained significant wealth in the past year betting on their unique perspectives. Since everything from real estate to baseball cards and dogecoin have skyrocketed, they have all somewhat been proven right. This further exacerbates their entrancement in their particular echo chamber, and causes FOMO for not capitalizing on it more. The whole world is now a stock & crypto picking savant – if you are fearful this all feels like the tech bubble, you are absolutely right; except for a few things. These growth businesses are much more real than the dot com bubble, crypto currencies are at a much different place today than 2017, and the Fed has proven to indirectly do all that it can to support asset prices.

- Story telling created a lot of multiple expansion in 2020; 2021 will be more data driven. We’ve written about the book Sapiens a number of times in our commentaries over the last 2 years. This is due to the importance of storytelling in markets. Storytelling is why we felt comfortable getting aggressive in March 2020. In a world where value is attributed more and more to the potential of what a particular entity could be in the future, storytelling is more important than ever. Where would Tesla be today without Elon Musk’s storytelling? In reality, Tesla’s rise is really a shift in the story, from a car company to maybe the world leader in Artificial Intelligence and advanced battery storage. In 2021, tech companies have to show real growth and blow out numbers during earnings season. A lack of blow out numbers could be disastrous.

- Battle for world power on two fronts between US vs China. On one side you have the battle for power and control, on the other innovation and GDP, all of which are intertwined into a circular web. In the fall, there were a lot of talks about monopolistic behavior from big US tech. More recently, you have China pulling the Ant Group IPO in fear of it wreaking havoc on its bloated financial institutions. One of the biggest questions to shape markets over the next few years is how each country plans to handle their tech giants. Letting them grow to compete globally against the other’s tech giants inevitably hurts most other sectors of your markets. At the end of the day, it’s simple math. Our tech giants are larger, their consumer base is larger; it’s inevitable that a few of theirs become larger than a few of ours.

- Throw consumption expectations out the window for the new crypto millionaires. There’s really no way to model consumption patterns from the wealth created in the crypto space. These individuals and entities amassed this wealth by betting against the status quo and society. They likely don’t have a massive 401k’s, and many aren’t buying insurance. They may be more drawn to cheap energy sources than they are to the status quo in major cities.

- When will crypto come for FAANG? It seems too early for this today, but with all of the news around Apple’s app store and the fee they charge to other companies accessing their network, it’s hard to believe there won’t be a blockchain solution for such things one day.

Short-term Inflation over longer inflationary concerns

Everything from food to real estate, lumber, oil, semiconductor chips and your Dawn dish soap is going up in price. Hopes are that this is a short-term blip that levels out a year from now, but the potential for real inflation is here. Industrial production is lagging in part due to labor shortages, and businesses are scrambling to catch up. This may ultimately lead to overly stocked inventory in the future, but we are 6-18 months away from that being a problem.

If we truly are in the midst of multiple innovation curves across many industries, we may actually begin to grow our way out of the black hole of debt we appear to be in. This is not the most likely outcome Toroso sees, but it is a potential one. Asset prices are at such high levels that many 65+ years of age may move into retirement, which would tighten the labor force and maybe cause wage inflation for younger workers.

{kind=link}

Market Risks and Rewards

It is far from guaranteed, and seemingly less likely each week that we will reach herd immunity from Covid, with new strains popping up in various parts of the world. Does this cause another exodus from cities? Does it even really matter for markets and the economy? Maybe just for our collective sanity. The amount of hidden leverage in the system is massive, creative, complex and, quite frankly, not really fully understood by any one group. Consumer Confidence & the use of leverage has soared – typically a bad time for risk assets with a less friendly Fed.

With the bad, there is also plenty of good. Retails sales increased 9.8% in March month over month. The Federal Reserve Money Supply M2 is up 25% year over year (descending from a peak of 27%), and innovation is occurring across pretty much every industry, despite being led by just a few.

Overall, not much has changed in our approach. We successfully rotated into more reopening & value trades over the last few months to barbell our growth names, but in general, the approach remains the same. High active share is king, and within that, diversify, diversify, diversify. Bet big on high growth and value, allocate heavily to alternatives, rebalance without emotion and expect pockets of volatility. With the amount of leverage in the system today, the days of 5-15% corrections are in the past; they will be of higher magnitude in the future.

US EQUITIES

Zombie companies still exist out there, and many are being bid up in the recent rotation to Value. Much of the Russell 2000 exists without profits. Broad indexes should still be invested in with caution. One big difference between truly high growth areas and value is that 6 months of no price appreciation means two very different things. One has low single digit growth rates while the other can exist in the mid-teens. 6 months without price appreciation in Growth markets may result in a 10% decline in current fundamentals. While financials and energy have been on a tear, a continued rally in all things commodities is unlikely. Materials for chips and houses aside, with the growth in electric vehicles and alternative energy, each new peak in Oil prices is likely to be lower than the last, leaving much more downside than upside for crude. Overall, the S&P 500, led by the iShares S&P 500 ETF (IVV), returned 11.83% as of April 31st. Large cap value is 5% ahead of large cap growth, and small cap is beating all, up 20.4% through April. Value has outperformed momentum by almost 14% this year. We recommend high active share in both Growth and Value areas.

{kind=link}

International Developed & Emerging Markets

MSCI ACWI ex US, measured by the iShares MSCI ACWI ex US ETF (ACWX), was up 6.48% through April. iShares MSCI EAFE ETF (EFA) was up just 6.62%, while the iShares MSCI EM ETF (EEM) was up just 4.56%. International developed equities are the value play of all value plays, or a perpetual value trap lead by an unhealthy banking system hooked on the ECB. They are definitely further behind the US in its vaccination rollout. Emerging Markets as a whole, similar to Europe and the US, are full of zombie companies. Despite this, there is still massive potential in the tech / Internet of Things space that is primarily coming from the Emerging Markets and China.

{kind=link}

Fixed Income

As we mentioned in previous commentaries, the Federal Reserve officially became co-investors in the bond side of a 60/40 portfolio in 2020 (the equity side may come in future market disruptions a la Japan). The Fed stepped in and bought shares of iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) and iShares iBoxx $ High Yield Corporate Bond ETF (HYG), and US bond markets may never be the same again. iShares Core US Aggregate Bond ETF (AGG) is off to a terrible start, returning -2.63% for the year through April. Long-term treasuries measured by the iShares 20+ Year Treasury Bond ETF (TLT) returned -11.89%. Yields on treasuries may have topped out for the year, but we still wouldn’t get too aggressive on the lower credit side of the spectrum. What’s very interesting is the breakdown in strong negative correlation between Momentum / QQQ and treasuries that we saw last year, with inflation expectations rising. The Fed has stated that interest rates will remain low for years. We see a risk that the Fed will need to step in sooner than anticipated and raise interest rates, which is far from a major 2022 concern. Active is preferred here as well; broad indexes are highly weighted in debt, rated just above default, which will be a problem if the Fed-induced merry-go-round even shows slight signs of stalling.

{kind=link}

Alternatives

It’s been a painful year for all things alternative. Gold, measured by SPDR Gold Shares ETF (GLD), was down -6.65% for the year, as were treasuries. The dollar is up just slightly on the year and commodities, measured by the Invesco DB Commodity Index Tracking ETF (DBC) is up 22.16%. We can make a case for a run in precious and industrial metal, all things tied to semiconductor chips, and potentially even see lumber at elevated levels persisting, but the oil run has likely dissipated.

A hypothetical high-active-share reconstruction of a traditional 60/40:

- 5% Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL)

- 5% PIMCO 25+ Year Zero Coupon US Treasury Index ETF (ZROZ)

- 10% Saba Closed-End Funds ETF (CEFS)

- 5% AGFiQ US Market Neutral Anti-Beta (BTAL)

- 10% SPDR Gold MiniShares Trust (GLDM)

- 10% SPDR S&P Kensho New Economies Comps (KOMP)

- 10% Davis Select Worldwide ETF (DWLD)

- 10% Emerging Markets Internet & Ecommerce (EMQQ)

- 10% Ballast Small / Mid Cap ETF (MGMT)

- 10% Amplify Transformational Data Sharing ETF (BLOK)

- 10% Sofi Gig Economy ETF (GIGE)

- 5% Distillate US Fundamental Stability & Value ETF (DSTL)

Conclusion

There truly is a lot of data pointing to a strong reopening. What will be interesting to see is whether people’s desire to increase spending on everything from services to leisure will lessen some of the retail influence the market experienced while we were all stuck at home. Everything from travel to dinners, hotel occupancy, and mortgage applications are on the rise. Invest cautiously, though it look like we are headed for record earnings on the S&P 500 in 2021.

{kind=link}

Disclaimer: This commentary is distributed for informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice. Nothing in this commentary constitutes an offer to sell or a solicitation of an offer to buy any security or service and any securities discussed are presented for illustration purposes only. It should not be assumed that any securities discussed herein were or will prove to be profitable, or that investment recommendations made by Toroso Investments, LLC will be profitable or will equal the investment performance of any securities discussed. Furthermore, investments or strategies discussed may not be suitable for all investors and nothing herein should be considered a recommendation to purchase or sell any particular security.

Investors should make their own investment decisions based on their specific investment objectives and financial circumstances and are encouraged to seek professional advice before making any decisions. While Toroso Investments, LLC has gathered the information presented from sources that it believes to be reliable, Toroso cannot guarantee the accuracy or completeness of the information presented and the information presented should not be relied upon as such. Any opinions expressed in this commentary are Toroso’s current opinions and do not reflect the opinions of any affiliates. Furthermore, all opinions are current only as of the time made and are subject to change without notice. Toroso does not have any obligation to provide revised opinions in the event of changed circumstances. All investment strategies and investments involve risk of loss and nothing within this commentary should be construed as a guarantee of any specific outcome or profit. Securities discussed in this commentary and the accompanying charts, if any, were selected for presentation because they serve as relevant examples of the respective points being made throughout the commentary. Some, but not all, of the securities presented are currently or were previously held in advisory client accounts of Toroso and the securities presented do not represent all of the securities previously or currently purchased, sold or recommended to Toroso’s advisory clients. Upon request, Toroso will furnish a list of all recommendations made by Toroso within the immediately preceding period of one year.