By Court Hoover, JAForlines

President Trump has not disappointed on his promise to shake up Washington. He is moving at breakneck speed to fulfill his campaign promises, to the delight of his supporters and consternation of his detractors. We are somewhat concerned that he has not tempered the personal volatility exhibited on the campaign trail, which risks translating into market volatility.

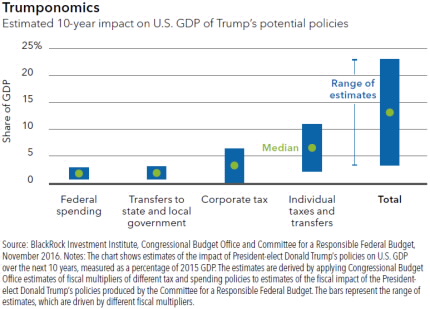

A bigger concern, however, is the policy priorities he has demonstrated in these three weeks. The most important parts of his platform to asset markets are tax reform and infrastructure investment. The chart below shows the economic impacts of various policies and clearly demonstrates the importance of Trump’s proposed tax reforms in particular.

Unfortunately, trade and immigration reform appear to be his highest priorities, both of which we view to have negative consequences for risk assets. Some markets have begun to reflect this disappointment: real US dollar interest rates have given up about half of their post-election increase, and the US dollar has given up nearly all of its post-election rally. Meanwhile, global equity markets have remained resilient.

{kind=link}

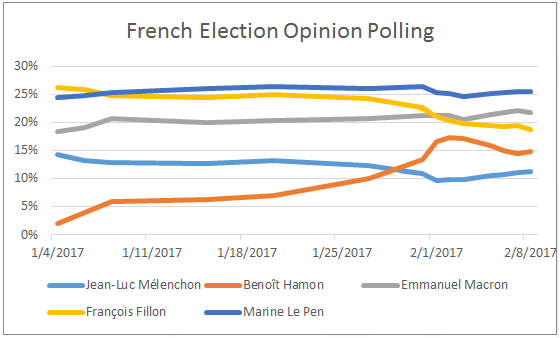

In Europe, the political environment has become less clear. Franҫois Fillon, the former front-runner for the French presidency and selfdescribed “Thatcherite,” has seen his campaign implode amidst corruption allegations that he hired family members as parliamentary aides without requiring them to perform any of the duties required by the positions, scuttling his chances to win the Presidency. Of the remaining candidates, only Emmanuel Macron would be greeted positively by markets.

The good news is that he now has a clear path to the Presidency, as it is unlikely that the far-right nationalist Marine Le Pen could win the second round head-to-head election.

{kind=link}

Those negotiations will require close scrutiny, as a €600bn per year trading relationship hangs in the balance. Despite these risks, we are optimistic that the political environment in Europe will improve over the course of the year, avoiding the pitfalls of a Le Pen presidency and catastrophic Brexit negotiations.

Our portfolios are positioned to benefit from the continued “Trump reflation rally.” This entails owning assets that

will benefit from an environment with greater economic stimulus in the US and global capital flows which reflect that.

{kind=link}

However, we have recently taken some profits and hedged the portfolio to some extent to protect our investors against disappointment in the speed at which policy reform is implemented.

Overall, our portfolios are allocated towards cyclical over defensive equities, and dollar denominated fixed income over foreign currencies. However, as a result of the high expectations for successful and timely implementation of President-elect Trump’s platform, we have increased our position in long duration US treasuries, which will benefit from disappointment in progress towards those goals.

{kind=link}

The bulk of our fixed income holdings are held in high yield bonds and preferred stock. This increases our portfolio’s yield and gives us exposure to cyclical assets which have benefitted following the US election. In addition, it gives us significant exposure to US corporate credit spreads, which should tighten as a result of

stimulative economic policy. We also continue to hold a position in US dollar denominated emerging markets bonds.

This helps diversify the portfolio while avoiding foreign currencies.

policies, against possible hiccups along the way.

{kind=link}

**Individual account allocations may differ slightly from model allocations.

*Some Emerging Markets allocation overlaps with regional allocations.

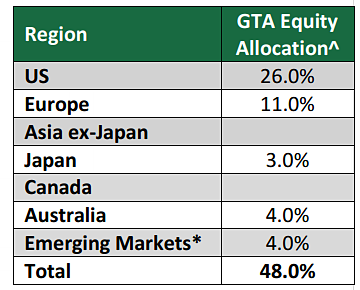

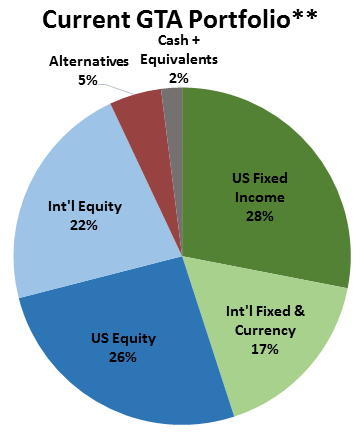

^Excluding GTA’s 52% fixed income, alternative, and cash positions.

Our equity portfolio favors cyclical over defensive sectors in order to benefit from the acceleration in economic growth likely upon implementation of President-elect Trump’s economic policy platform. In the US we favor financials, technology, biotech, defense, and small cap. Financial stocks have been hurt by persistently low interest rates and a flattening yield curve, and a reversal of that process will support them.

Additionally, we expect the regulatory environment to improve under a Trump presidency. US technology companies are the most innovative in the world and will continue to expand their scope into new industries, displacing many older companies and industries through the process of creative destruction.

Small caps are more US-centric than the broader US equity market. They tend to have much less foreign exposure, both in terms of production and sales, and therefore will benefit from Trump’s “US first” policy philosophy. Biotech stocks have underperformed in expectation of healthcare reform. They therefore represent good relative value and also potentially serve to protect the portfolio against underwhelming progress made towards reform in Washington. We have initiated a position in US defense stocks.

US allies are reconsidering their dependence on the United States for military protection, and will therefore seek to build up their own defense in the coming years. We have trimmed our position in small caps in order to protect the portfolio against disappointment in progress made in Washington. Internationally, we hold positions in European, Japanese, Australian, and Mexican equities.

European equities, and particularly financials, offer strong relative value and should be supported as the political environment becomes clearer over the course of the year. Fiscal and monetary stimulus in Japan will continue to put downward pressure on the Yen, which will support the Japanese equity market. We have maintained our position in Australian equities which are also supported by pro-growth fiscal policy and a recovering commodity market.

Following a major selloff in Mexican equities as a result of Trump’s victory, they offer deep value and a cheap way to protect the portfolio against disappointment in reform implementation. We continue to hold a position in gold. Its status as an alternative currency should support it as global central banks continue to pursue extremely aggressive policies. Furthermore, as an asset with low correlations to most others, it helps lower overall portfolio volatility.

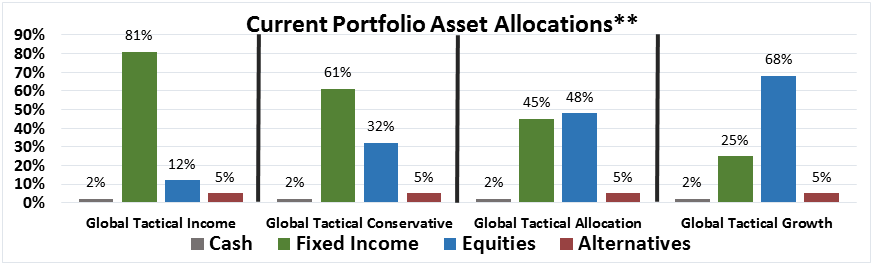

Global Tactical Income Positioning Our Global Tactical Income Portfolio uses the same global macro framework as our other three Global Tactical Portfolios, but due to its income and capital preservation investment goals, its holdings differ to some degree. It does not participate in some equity allocations, and owns some additional fixed income holdings.

Currently, GTI owns Treasury inflation-protected securities and Build America Bonds, in addition to the fixed income holdings common across all four portfolios. These holdings help reduce volatility, while increasing diversification and limiting concentration. Its equity exposure avoids Australia and Mexico in order to reduce volatility.

This article was written by the team at JAForlines, a participant in the ETF Trends Strategist Channel.