“The underperformance of MXN and EM Asia is of course easily explained by the focus of President-elect Trump,” Citi said. “We don’t think Mexican rates can decouple, at least before an extraordinarily large rate hike out of Banxico.”

If Citigroup is right, the short-term selling may still have legs. Moreover, Citi anticipates the fallout may be even worse than the 2013 selloff, despite generally stronger fiscal positions in emerging economies.

“While it is not clear how much of this protectionist part of President-elect Trump’s platform can be implemented, it is clear that any move in this direction would add further impetus to inflation in the U.S., and would also redistribute growth from emerging markets to the U.S.,” Citi added. “This would suggest that EMFX can actually perform worse than in 2013, relative to U.S. assets. Furthermore, a potential trade war with China would undermine the commodity consumption by China and offset the positive impact from the U.S infrastructure spend.”

Investors can also hedge against a further pullback in the emerging markets through inverse ETF options. For instance, the ProShares Short MSCI Emerging Markets (NYSEArca: EUM) takes the inverse or -100% daily performance of the MSCI Emerging Markets Index, the benchmark to EEM. The ProShares UltraShort MSCI Emerging Markets (NYSEArca: EEV) follows the -2x or -200% daily performance of the Emerging Market Index. Additionally, the Direxion Daily Emerging Markets Bear 3x Shares (NYSEArca: EDZ) tracks the -3x or -300% performance of the benchmark.

For more information on the developing economies, visit our emerging markets category.

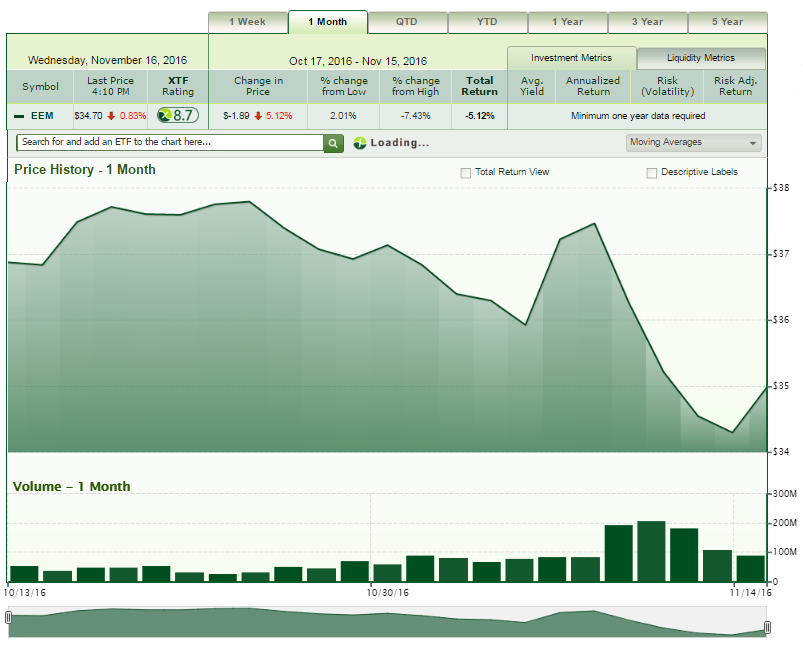

iShares MSCI Emerging Markets ETF

{kind=link}

Chart courtesy xtf.com