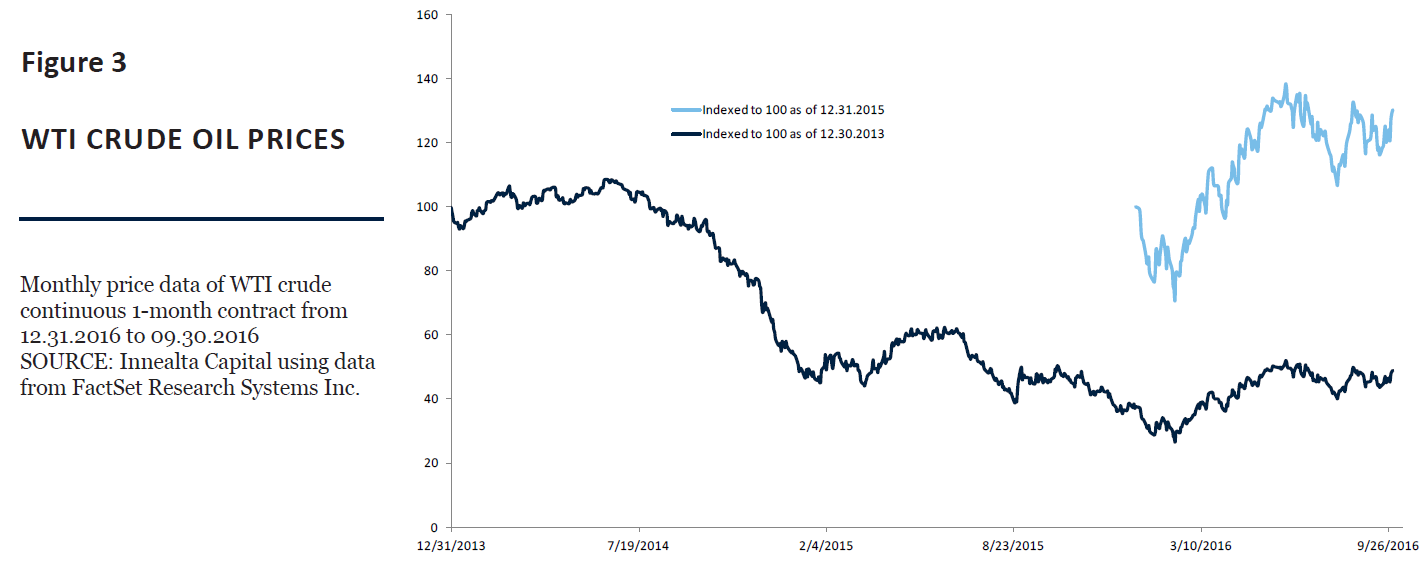

From a shorter-term perspective, oil has increased approximately 30%, while from a longer-term perspective, oil prices would need an increase greater than 100% to reach it former peak.

{kind=link}

EARNINGS REVIEW

Outside of monetary policy decisions, the next big market event relates to the Q3 2016 corporate earnings announcements season.

So far, market expectations estimate another quarter of year-over-year earnings declines. Should this be the case, it will be the first time we experience six consecutive quarters with year-over-year earnings declines since the 2008 recession.

Additionally, 16% of S&P 500 companies have already issued negative earnings per share (EPS) guidance, compared to only 7% that have issued positive EPS guidance.

The largest detractor of earnings growth in the S&P 500 continues to be the energy sector, which is still experiencing the effects of relatively low oil prices. Nine of the now eleven sectors are expected to report year-over-year sales growth.

The estimated sales growth rate for Q3 2016 is 2.6%, which is 0.1% higher than the same estimate from the beginning of the quarter. As of the end of September, the forward 12-month P/E ratio of the S&P 500 is 16.6, down from 16.9 one month ago. With earnings season fast approaching, it will be interesting to see which

sectors ‘hit’ and which sectors ‘miss’ earnings.2

LOOKING FORWARD

The calendar of future macroeconomic data will follow the traditional pattern. The Bureau of Labor Statistics releases September’s Employment Situation report on October 7th, Alcoa Inc. kicks off the earnings season on October 11th, and the FOMC publishes its minutes from the September policy meeting on October 12th.

Retailers in the U.S. are gearing up for the seasonal boost in spending from holiday shopping sprees; a phenomenon that has on average benefited the retail sector in the month of October since 2009, as measured by the S&P Retail Select Industry Index.2

The combination of earnings announcements, the upcoming unemployment statistics, and other macroeconomic data will provide insights for the Fed, which meets only twice more in the balance of 2016.

SUMMARY

During September, the market absorbed unexpected news within oil markets, digested expected results from central banks, and saw further dispersion in world currencies relative to the dollar.

The unexpected news of an OPEC supply freeze on 09/28/2016 reversed the negative intra-month performance and helped WTI crude oil and the S&P 500 energy sector to post +0.80% and +1.34% returns in September, respectively.

Across monetary policy, the FED and ECB matched market expectations with no change in target rates or monetary intervention. The Bank of Japan, however, did not meet market expectations of new stimulus; they announced targeting the yield curve with remaining purchases.

Relative to the dollar, the British pound continues to decline as “Brexit” fears remain, while the Japanese Yen continues to strengthen as the Bank of Japan offered no incremental increase in monetary stimulus.

In October, United States corporate earnings will be an important economic new data point, which will surely capture the attention of investors.

This article was written by Innealta Capital, a participant in the ETF Strategist Channel.