An equal-weight approach is essentially factor neutral, despite its minor tilt to smaller size and value, and gives no credence to technical, fundamental, or price-driven factors. It is therefore less predictive in nature. At Swan, we believe predicting the market is difficult if not outright impossible. While some evidence can be generated to support any prediction, there is truly no way to know how technology, utilities, and materials will perform going forward.

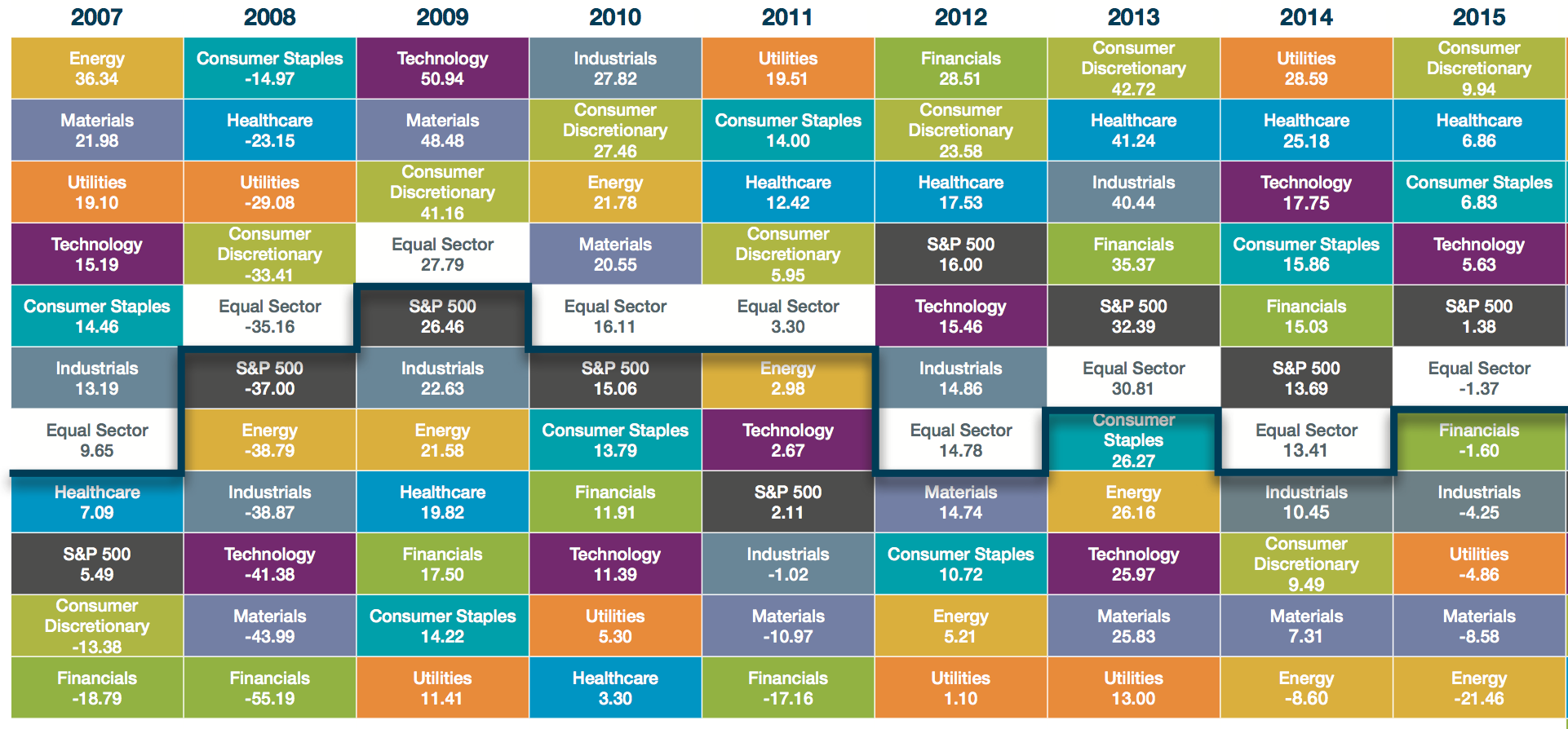

In addition to being factor neutral, equal weighting captures another important stock price behavior: mean-reversion. An equal weight portfolio has built-in “alpha” as it must be rebalanced periodically; the portfolio is in effect buying the losers at “low” prices and selling the winners at “high” prices, which benefits automatically from short-term mean-reverting price behaviors. This buy low, sell high approach is what drives the improved performance numbers behind more frequent rebalancing. Profits are always being taken and discounts are always being bought. In the Financial Crisis, EQW was buying financial stocks as they fell and selling them later as they rose. A more recent example, EQW was consistently buying energy stocks as they fell in 2015 and has been selling them throughout its strong bounce in late 2016 as the sector rises in comparison to the other sectors. This is referred to as a mean reversion strategy and there is an ample amount of research spanning many decades that support this concept (i.e., the benefits of rebalancing).

The underlying principle of mean reversion is that investors can and will behave irrationally, resulting in stock prices that take large swings away from their fundamentals. Although this behavior does not lead to extremes all the time, the strategy patiently waits until it does and then takes advantage of any illogical market moves, like the Tech bubble in 2000. This means it can routinely underperform for long stretches of time when the market is driven by strong trends and momentum. For example, the three worst performing sectors over the last 3 and 5 years have been Energy, Materials, and Utilities. Over the past 10 years, only Financials has been worse. The contrarian mean reversion argument is that these three important overweight sectors to an EQW approach likely won’t remain the worst performers forever and the recent EQW underperformance could come to an end. By nature though, an equal-weight approach will likely trail during strong bull markets such as the current 7-year bull market. In a strong bull market, usually a few sectors begin to lead out and take the market higher.

Some proponents of cap-weighted argue that the world’s new economy is now driven by technology and healthcare. Although it seems apparent that these sectors should have a big impact on the economy going forward, this doesn’t mean that stock markets won’t overprice and inflate the value of the stocks within these sectors as more investors pile into a popular trade. Historically, stock markets tend to overvalue and inflate the popular, leading to ever increasing higher valuations and bubbles. If the current bull market continues for a few more years, led by Technology and Healthcare as it has been, the conditions will continue to point to an equal-weight approach as being more prudent and potentially beneficial for the long-term investor.

{kind=link}

Source: Alps and Bloomberg

In summary, equal-weighting of the sectors provides for better diversification, lower volatility, and the potential for better long-term performance as compared to cap-weighted. These benefits mostly occur through and after bear markets as overvalued and overweighted sectors correct. Although no one can predict the market, long-term and short-term evidence points to an equal-weighted approach being a more prudent and potentially beneficial choice over cap-weighted. This is why at Swan we allocate our core equity component in our S&P 500 Defined Risk Strategy to the SPDR Select Sector ETFs in an equal sector weighting. We believe this core equity position coupled with a long-term hedge and our option income component, are the best way to achieve consistent long-term risk-adjusted returns in today’s risky market environment.

Micah Wakefield is Director of Research and Product Development at Swan Global Investments, a participant in the ETF Strategist Channel.

CLICK HERE TO READ PART TWO!

Important Disclosures:

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan Global Investments offers and manages the Defined Risk Strategy for investors including individuals, institutions and other investment advisor firms. All Swan products utilize the Swan DRS but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results and comparing results among the Swan products and composites may be of limited use.

Swan claims compliance with the Global Investment Performance Standards (GIPS®). Any historical numbers, awards and recognitions presented are based on the performance of a (GIPS®) composite, Swan’s DRS Select Composite, which includes nonqualified discretionary accounts invested in since inception, July 1997 and are net of fees and expenses. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.

The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. All investment strategies have the potential for profit or loss. Further information is available upon request by contacting the company directly at 970.382.8901 or visit swanglobalinvestments.com.