These systematic issues in calculation are no secret, and we think a Q2 GDP measurement acceleration is likely already factored into market prices. Again, one has to wonder how much good news is priced in. We think we are in for a grind on the way to higher market levels, and risk matters.

Overall, the U.S. economy appears to be on a stable, though sluggish, growth trajectory. For example, recent headlines focused on the very poor May 2016 U.S. labor report that showed only 38k new jobs were created in May, and revised the previous months’ figure down an additional 59k jobs.

Related: Risk First: Why The Global Economy Should Continue to Grow

Adding to growth concerns is the latest ISM Non-Manufacturing Index, which measures the service side of the U.S. economy, and suggested a significant decline in the rate of growth. The service sector makes up the majority of the U.S. economy and the index declined from 55.7 for the April reading to just 52.9 in May, and is down 5.4% from a year ago. While a reading above 50 suggests expansion of the U.S. service sector, the indication is that the rate of growth for this very important part of the economy has slowed.

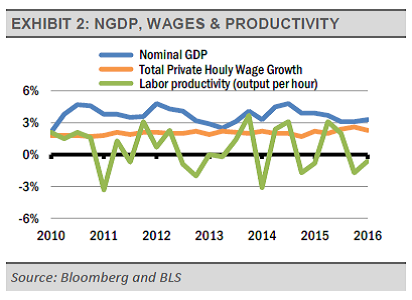

Looking at these and other data points leads us to think that nominal GDP growth (GDP measured without inflation adjustments), which we think can be a good proxy for sales revenue growth, will remain near the low end of its post-financial crisis range. With that in mind, the increasing pressures we see on hourly wages, combined with the lack of productivity growth, means that corporate earnings and profit margins should remain under pressure. We expect economic growth and asset prices to grind higher over the near-term, but not to breakout significantly higher or lower.

{kind=link}

Gary Stringer is the CIO, Kim Escue is a Senior Portfolio Manager, and Chad Keller is the COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management LLC and has not been verified or audited by an independent accountant.