Our largest recent reallocation of funds was to European low volatility and small cap stocks. The ECB’s more aggressive QE policy means that about €80 billion in newly printed money will be injected into financial markets every month, and a comparable amount of safe assets like government bonds will be purchased and removed from financial markets. More money circulating in financial markets and fewer safe assets available for purchase tends to benefit low volatility equity assets, since the money has to go somewhere and low volatility stocks are often perceived to be the next safest alternative to bonds. We believe that additional financial market liquidity due to QE should also disproportionately benefit small cap European equities, as should the accelerating economic recovery suggested by Europe’s recent GDP statistics.

Related: Housing Recovery – The Next Generation Joins In

We continue to have significant Japanese exposure, but have focused on the one sector of the Japanese market that has benefited from Japan’s flawed implementation of NIRP – real estate. The Japanese government is borrowing at negative interest rates at maturities beyond 10 years. These negative rates have pulled mortgage rates in Japan down to about 1.5%. Since Japanese homeowners receive tax benefits equal to almost 1.5% of their mortgage balance, Japanese real estate can be financed at virtually no net interest cost. Real estate prices in the major Japanese cities are rising fast and finally getting back to the levels seen in 1989/1990. These price gains are fueling a construction and renovation boom that we believe will be sustained by negative rates even if the economy continues to struggle. According to a May 8th report from Evercore ISI, Japanese housing starts have risen 13.7% over the past two months.

{kind=link}

Our other most significant Japanese position is in small cap Japanese stocks. Our due diligence trip to Japan in 2015 convinced us that smaller Japanese companies are innovating and outcompeting the established “Japan, Inc.” dinosaurs. We believe that process will continue irrespective of the monetary policy missteps of the BOJ.

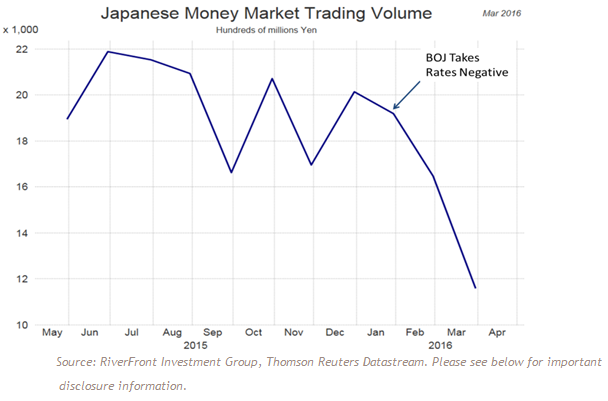

We recognize that the BOJ’s inaction at its April meeting may have been motivated by the upcoming G-7 meeting and Japan’s desire to avoid being vilified at that gathering as a currency manipulator. The harsh rebuke for Japan’s currency policies in Treasury Secretary’s Lew’s recent congressional report and the tone of the current US presidential campaign would appear to validate these fears. Once this meeting concludes, Kuroda may try to get Japanese monetary policy back on track and the yen back down to a comfortable level for Japanese companies. However, after its recent mistakes we are not inclined to extend Japanese policy makers the benefit of the doubt. We will need to see both better policies and a positive market reaction to those policies before returning to a higher weighting in Japan.

Michael Jones is the Chairman and Chief Investment Officer at RiverFront Investment Group, a participant in the ETF Strategist Channel.

[1] “Japan’s Negative-Rate Experiment is Floundering.” Eleanor Warnock and Mayumi Negishi, WSJ.com (April 14, 2016). http://www.wsj.com/articles/japans-negative-rate-experiment-is-floundering-1460644639

Important Disclosure Information