The recent rallies in global equities, high yield bonds and commodities are neither a head-fake, nor a signal that the road ahead is clear in our view. While the markets have gained and underlying fundamentals have improved, we think risk management is still very important in this type of environment. Defensive equity and investment grade bonds look to us as areas to potentially protect principal in the near-term. We are not overly concerned with interest rate risk at this time. We think that market forces will keep long-term interest rates grounded for the time being.

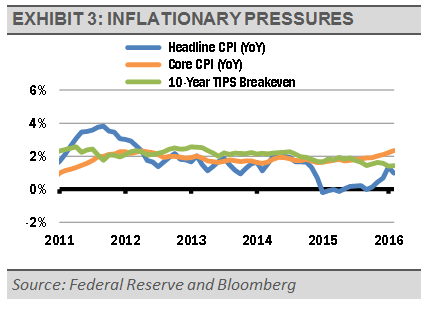

Although inflationary pressures may be building, we think that the recovery in survey-based inflation, is fragile.

Any additional Fed rate hikes can quickly tame inflation pressure, while sluggish nominal GDP growth will provide an additional cap to inflation expectations and long-term interest rates. We think this weakness in potential inflation is better captured by market-based measures of inflation expectations, such as the 10-Year Treasury Inflation-Protected Securities (TIPS) breakeven spreads, which suggest that inflation risk is receding and not likely to meet the Fed’s target for core inflation.

{kind=link}

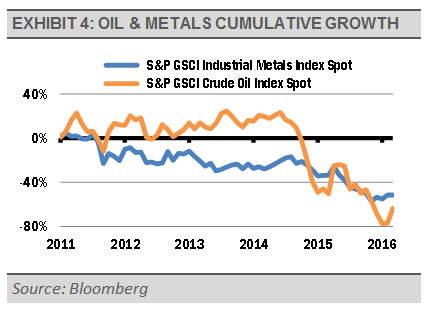

With the pace of Fed interest rate hikes slowing, which has resulted in softening of the U.S. dollar and China seemingly stabilizing, commodity prices may have formed a bottom during the first quarter. We think there is a long-term relationship between the price of oil and industrial metals.

Oil fell so fast that it went from being expensive relative to industrial metals to overly cheap, in our view. As a result, the decline in oil may have been overdone. We think oil needs to appreciate to roughly $50 a barrel to return to its normal price relationship with industrial metals. We also continue to be skeptical about the investment potential of gold. Gold may represent trading opportunities from time to time, but we think the long downtrend in the price of gold will continue.

Gary Stringer is the CIO, Kim Escue is a Senior Portfolio Manager, and Chad Keller is the COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management LLC and has not been verified or audited by an independent accountant.