The Payroll Report from March 4 showed sizable growth of 242,000 in total non-farm employment. The headline number was considerably above the street estimate of 190,000 and well above the January advance of 172,000 jobs. The prior two months figures were revised higher by 30,000 jobs. This month’s advance is similar to an average gain of 241,000 for the last three months; higher than the 220,000 average for the past 6 months and well above the 190,000 average since the employment numbers bottomed in February of 2010.

Once again there were important areas of strength. The overall labor force rose by 555,000 exceeding the promising 502,000 from January. Those “not in the labor force” declined by a sizable 374,000 so the ‘true’ number was much stronger than the posted number as the change in nonfarm payrolls plus those coming back to the labor force came out to 616,000. An expanding economy tends to attract more people to the labor force, seeking employment.

The “Household Employment” figure moved up 530,000 after a jump of 615,000 the prior month before and represented the fifth month in a row of robust numbers in this category. The household survey provides a broader picture of employment including agriculture and the self-employed. Together with the ‘headline’ non-farm payroll number they provide a more complete picture of the labor market.

“Part time employment for economic reasons” was flat at 5.988 million. This figure had been down the past two months and down more than 700,000 from a year ago. This tends to indicate that more job seekers are finding full time positions.

The unemployment rate (U3) also remained flat at 4.9% although the broader U6 unemployment rate, which some describe as the “real” unemployment rate improved to 9.7% from 9.9% in January and the lowest level since May 2008.

The labor force participation rate measures the percentage of the working age population in the labor force. As was the case in January, it moved up slightly to 62.9%, the 4th month in a row it has increased. The participation rate decline since the 2008 financial crisis has been much discussed as it aided the decline in the U3 unemployment rate as it creates a smaller denominator when calculating the unemployment rate. Now it seems to be reversing. Meanwhile, the employment to population rate increased to 59.8% vs. 59.3% a year ago.

Private sector jobs grew 230,000 jobs and the government sector increased by 12,000 jobs. Within the totals, the strongest areas of job growth could be found in education and health services (up by 86,000), and retail (54,900 increase). Despite the strong gains in retail, “goods producing jobs” (manufacturing) declined by -15,000 having risen by 40,000 in January. Those under 25 years of age and those above 55 years added 314,000 jobs, more than double the main cohort of 25-54 years which added 153,000.

Average hourly earnings were $25.35/hour in February, a gain of 2.22% from a year earlier, a slight disappointment, as it was a bit slower growth than what was recorded in January, a gain of 2.54% year over year. Average Hourly Earnings were 3c below the January result. January had advanced 12c over December. Hours worked declined modestly, down 0.58% M/M and Y/Y. Clearly there is some wage inflation although it’s increasing at a moderate pace.

{kind=link}

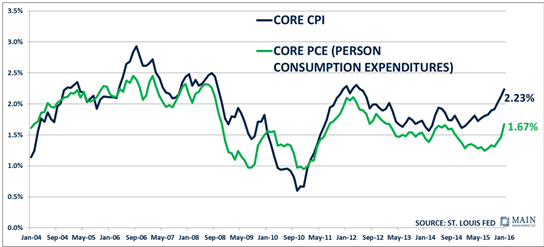

However it seems as though labor market strength is having a notable impact on other inflation indicators. The Core CPI, which excludes food and energy, is climbing to levels not seen since prior to Lehman’s collapse. Perhaps even more significantly, the PCE (Personal Consumption Expenditures) a gauge closely watched by the Fed, has turned sharply higher.

The odds of a Fed rate increase in March may negligible, yet as the year progresses and the aforementioned trends hold true, it’s hard to imagine the Fed not raising at least once.

A pioneer in managing all-ETF portfolios, Main Management LLC is committed to delivering liquid, transparent and cost-effective investment solutions. By combining asset allocation insights with smart implementation vehicles, Main Management offers a unique approach that translates into distinct advantages for our clients, including diversification, tax awareness and cost efficiency. For more information, visit http://www.mainmgt.com.