We think that the plunge in oil prices since the last Federal Reserve meeting may have allayed the Fed’s short-term inflationary concerns for the time being. As a result, we believe that the Fed is very likely to put further interest rate increases on hold until at least their March meeting. Any delay in Fed tightening may help stabilize the oil market by reducing upward pressure on the dollar, and help improve sentiment in the equity markets. A pause in Fed rate increases is likely to be accompanied by additional easing moves by the ECB and BOJ. ECB President Mario Draghi strongly hinted in his comments following their January meeting that turmoil in the oil market could prompt additional stimulus measures, and the obvious deflationary pressure of oil at $30 per barrel may silence German opposition to more aggressive ECB action. The BOJ faces even more imminent need for policy moves, as falling oil prices are reversing the progress Abenomics has made toward increasing Japanese inflation expectations

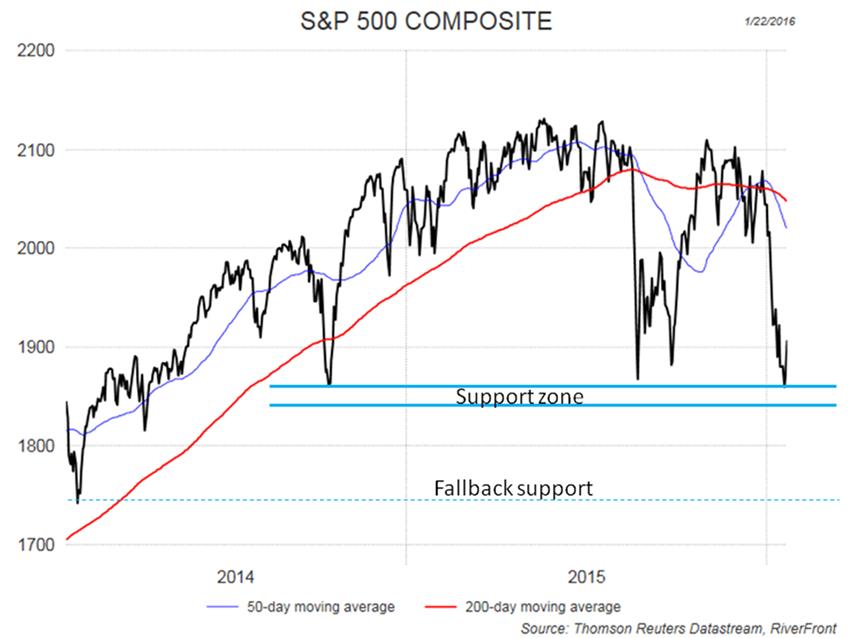

In addition to attractive valuation and potential for policy stimulus, the positive support for equity markets is enhanced by an improving technical picture. RiverFront raised as much as 30% cash in our portfolios as the S&P 500 broke successive stop losses at 2050, 1980 and 1940. When raising this cash, we established 1840-1860 as the likely support zone for equity markets. On January 20th, this support was broken in a sudden dramatic drop during intraday trading, but buyers came in before the close and the market ended above our support levels. We believe this behavior resembles “capitulation” trades that have often marked the end of market corrections. The odds of higher markets levels calculated by our technical trading model also increased after these market gyrations, and we have started putting money back to work.

As shown in the chart below, the S&P 500 at a level of 1840-1860 represents strong technical support; but, if these levels do not hold, the market could experience an additional drop of as much as 5 to 6% before finding additional support around 1750. We recognize that by starting to put money to work now we might not catch the absolute bottom in equity markets, but with both our fundamental and technical processes calling for higher markets we are staying true to our investment disciplines.

{kind=link}

This is Not 2008

Attractive valuation, additional monetary stimulus and strong technical support will not prevent further market declines if investors become convinced that collapsing oil prices will produce a debt crises similar to the one experienced in 2008. We believe that the economic impact of the energy industry and the size of its debt problems is much less significant than the housing/mortgage crises of 2008.

From an economic perspective, the oil and gas exploration industry is a fraction of the size of the housing industry. According to the Bureau of Labor Statistics, US employment in the oil and gas exploration has fallen over the past year from a little over 200,000 to about 184,000. By comparison, employment in the home construction industry fell from a peak of 7,400,000 in 2005 to less than 4,500,000 at the depths of 2008. The jobs lost in the housing industry during the Great Recession were 10 times greater than total jobs in oil and gas exploration. The oil and gas industry supports many more jobs in related fields like pump manufacturers, trucking firms and capital equipment manufacturers, but jobs in industries related to the housing market are even more economically significant (e.g. appliances, furniture, carpeting). We believe that the housing market will enter 2016 with significant positive momentum, fueled in part by higher disposable income made possible by lower prices at the pump. Continued recovery in housing can more than offset problems in the oil patch, in our view.

The debt problems of the energy industry are similarly dwarfed by the size of the mortgage crises of 2008. According to a report by Ed Westlake at Credit Suisse, “in four years of $100/bbl oil, the global oil and gas industry has taken on a quarter of a trillion dollars in debt.”[1] While $250 billion in speculative energy debt is a daunting figure, it pales in comparison to the magnitude of the 2008 US mortgage crises. Mortgage debt soared to over $11 trillion by 2008, and in the next few years over 9% of these loans became more than 90 days delinquent. Even if 100% of the debt taken on in recent years by the global oil industry were to default (a highly unlikely occurrence, in our view) these defaults would be less than 25% of the nearly $1 trillion in mortgage loans that went bad in the Great Recession.

Not only is the size of the energy debt not comparable to the 2008 mortgage crises, the banking industry is less exposed to these risks. Regulators allowed banks to leverage mortgages 25 to 1, and leverage AAA mortgage backed securities 50 to 1. This regulatory incentive encouraged banks to overinvest and overleverage in supposedly “safe” mortgage debt. By contrast, energy lending is well recognized as high risk and banks must back these loans with far more capital than was the case with mortgages. Banks have therefore been far less active in energy lending than was the case with mortgages, and any defaults represent much less of a threat to the global financial system, in our view.

Investment Implications

RiverFront’s investment discipline seeks to combine art and science into the management of our client portfolios. The science of our approach is our Price Matters® discipline, and this process suggests that equities, especially developed international equities, are priced to provide attractive returns over the next 5 years. The art in our management process is the short term technical and fundamental analysis that guide risk management and the timing of our reinvestment decisions. Both the art and science of our discipline suggest that the current pull back has run its course and it is time to reinvest the cash that we have accumulated. As with every investment decision at RiverFront, we have a risk management plan in place in case of assessment of market conditions proves overly optimistic.

Michael Jones is the Chairman and Chief Investment Officer at RiverFront Investment Group, a participant in the ETF Strategist Channel.