As has been widely noted, fixed income exchange traded funds have been investor favorites to start 2016. Five such funds are among the top 10 asset-gathering ETFs on a year-to-date basis, but those ETFs are U.S. government debt funds.

With bonds in style and equities slumping, investors might want to consider spicing up fixed income portfolios with the SPDR Barclays Convertible Securities ETF (NYSEArca: CWB).

Convertible bonds are a type of hybrid fixed-coupon security that allow the holder the option to swap the bond security for common or preferred stock at a specified strike price. Due to the bond’s equity option, convertible bonds typically pay less interest than traditional corporate bonds. The fund, though, does not convert its holdings into shares, but investors are exposed to the equity premium due to the way the bonds are priced. [A Bond ETF To Diminish Volatility and Boost Yields]

When the equities market dips, convertibles moves away from the price at which they can be exchanged for the stock and act more like fixed-income assets. On the other hand, as equities rise, convertibles will act more like stocks. Consequently, the asset class can have smaller up and down swings.

“The past three years have marked the resurrection of a vibrant market for new convertible issuance. The years 2013 and 2014 each delivered nearly $50 billion of new issuance. In 2015, 82 new issues totaling $39.3 billion came to the U.S. convertible market, while approximately $40.4 billion was redeemed through redemptions and maturities, according to Bank of America Merrill Lynch,” reports Edward Silverstein for MarketWatch.

Companies, notably those with speculative-grade debt ratings, like convertible bonds because they can raise money at rates lower than those on ordinary bonds.

Other CWB advantages include convertibles’ status as the top-performing bonds when rates rise and an expense ratio of just 0.4%, more than 70 basis points below the average actively managed convertible bond mutual fund.

“As a result, the preponderance of new issuance over the past three years has been from non-investment grade companies. In addition, we expect new issuance from investment-grade companies to remain depressed until the yield on the 10-year U.S. Treasury exceeds 3.5%,” according to MarketWatch.

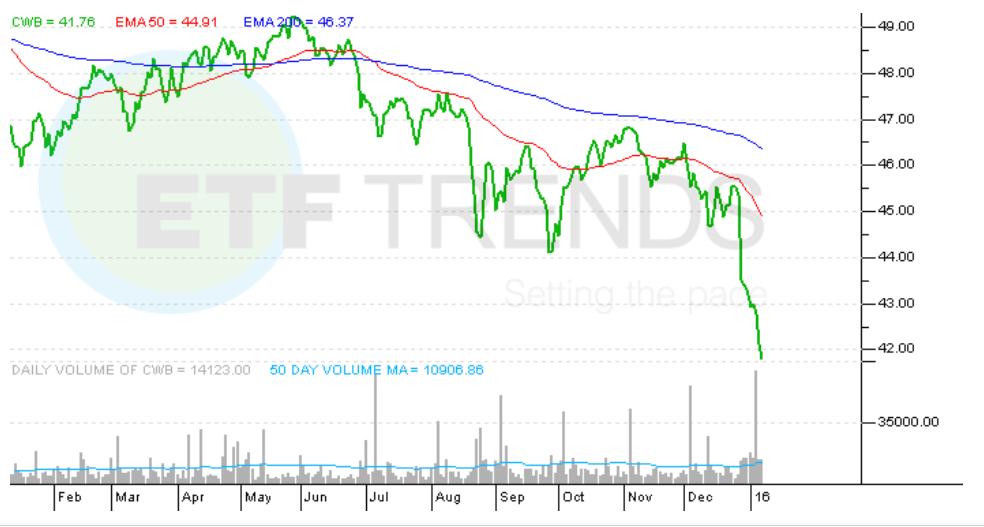

SPDR Barclays Convertible Securities ETF

{kind=link}