The rationale for raising interest rates has been somewhat of a moving target for the Fed over the past 3 years. At first, it seemed as though 6% unemployment was the threshold requirement. Once this level was attained, attention shifted to a 2% inflation target, with a particular focus on wage inflation.

Although inflation has been persistently short of the 2% level, significant near-term upticks in wages may have pressured the FED into their December 16th, 2015 rate hike. The Bureau of Labor Statistics (BLS) average hourly earnings for December indicate a year-over-year increase of 2.5%.

Moreover, BLS compensation per hour numbers (a measure of gross wages, benefits, and exercised stock options) came out at a 3.6% increase year over year for Q3, 2015. These are up from a revised 3.2% in Q2 (raised from the prior 2.2% estimate). That makes it a further increase from only 1.5% year over year in Q1, 2015.

Accordingly, these numbers indicate that wages and benefits are accelerating, and the consumer appears to be in good shape. Since the consumer represents around 70% of the US GDP, the strength of this segment should ensure that the economy can continue to grow (albeit slowly) at around 2%.

The Conundrum Facing the Fed When Raising Rates

The job numbers paint a similar picture. The Labor Department’s payroll number for December showed the economy added 292,000 workers. This exceeded the highest estimate in a Bloomberg survey. Furthermore, November’s payrolls were revised higher to 252,000 from a previous estimate of 211,000. Since 1999, there has been only one year in which more workers were hired.

In November’s ADP Employment Report, companies that employ 500-999 employees had the largest increase ever reported in the history of ADP keeping numbers. The service sector was the source of the largest increase, with 204,000 new jobs. This contrasts with an upwardly revised number in October of 174,000.

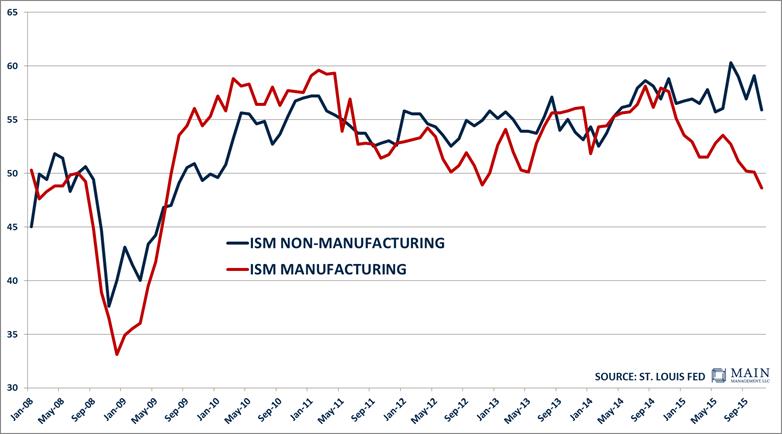

However, not all sectors of the economy have a resoundingly positive trajectory. This is particularly the case for manufacturing which paints a decidedly different picture. November’s ADP Employment Report indicates that the manufacturing sector added just 6,000 jobs. While small, this reverses the trend from the losses registered in the prior two months.

The ISM chart below underscores this point, with manufacturing experiencing a significant slowdown since September 2014 with the rest of the economy consistently within a narrow range in growth territory. Accordingly, it looks as though we have a two-speed economy with consumers doing fine and manufacturing flirting with recession.

{kind=link}

The Fed does not appear to ever have raised interest rates with the ISM manufacturing number below 50. It appears as though almost zero interest rates and service sector strength may have proved to be the compensating factors that led them to end this streak.

Were Hikes Right for the Economy?

Was the rate hike the right thing to do on December 16th? Following over 5 years of a Fed Funds rate of close to zero, such a move is probably long overdue. The global economy seems to be entering an anemic period, one that may not reverse itself in the near term due to aging demographics in the developed world. As a result, there may not be too many more appealing junctures on the horizon to raise rates.

Such a move is unlikely to curtail a strong dollar and may continue to hinder manufacturing, particularly as it relates to exports. That said, offering almost free money for seemingly indefinite stretches typically encourages excessive risk taking and increased probability of future bubbles. The economy is not strong, but likely solid enough to justify a move.

Will China’s early 2016 devaluation cause the Fed to second-guess its rate rise? Surely, at a minimum, it provides pause with respect to the proposed multiple rate hikes in 2016. On the other hand, at least it gives them the option to lower rates, should the global equity market rout of early 2016 persist.

Hafeez Esmail is the Chief Compliance Officer at Main Management, a participant in the ETF Strategist Channel.