Once beloved income-generating asset classes, master limited partnerships and sector-related exchange traded products have tumbled in unison with oil and natural gas prices this year with some analysts expressing view that it is still too early to embrace downtrodden MLPs.

At the crux of the matter, investors are worried that a traditionally attractive dividend-paying asset would no longer be able to maintain its steady payouts as U.S. oil output starts to decline after the steep drop-off in crude prices.

MLPs earn money by transporting energy or storing the products. Since revenue is based on volume, MLPs may be less sensitive to crude prices. However, with crude oil prices near seven-year lows, investors are growing concerned about the energy industry’s ability to keep pumping oil.

“Our view is that it is still too early to buy the MLPs. There are many concerns about bankruptcies in the energy sector coming,and both Evan Calio and Adam Longson are incrementally negative about oil dynamics in the near term. Many yield-seeking investors, particularly on the retail side,are very overweight this group,and there may be substantial selling in front of us,” according to a Morgan Stanley note posted by Amey Stone of Barron’s.

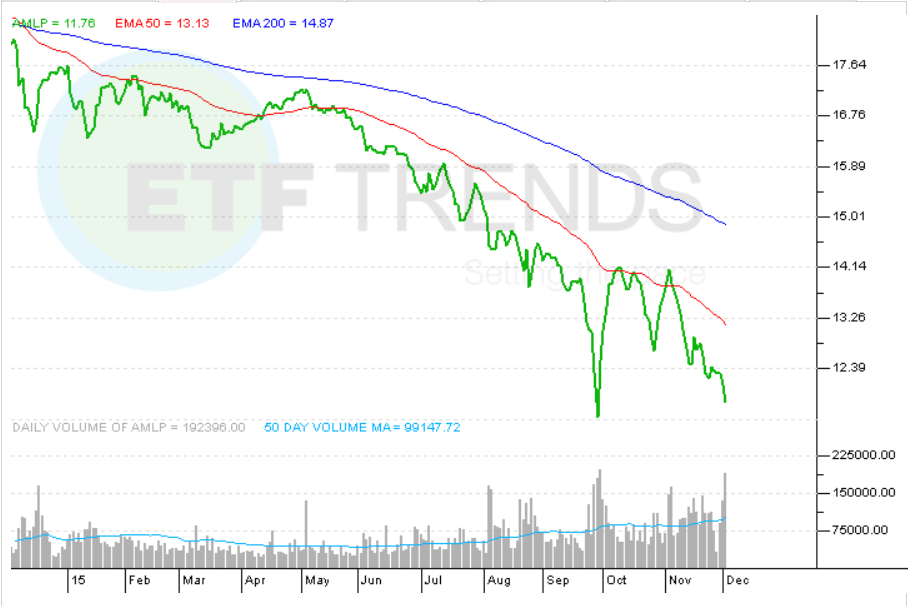

The JPMorgan Alerian MLP Index ETN (NYSEArca: AMJ) and Alerian MLP ETF (NYSEArca: AMLP), two of the largest MLP exchange traded products, are sporting an average one-year loss of about 38%.

In the recent crude oil sell-off, investors did not distinguish MLPs from other energy-related assets and dumped the asset as crude oil prices plummeted.

MLPs primarily deal with the distribution and storage of energy products, so their business model is less reliant on the commodities market since MLPs profit off the quantity of oil and natural gas they are able to move around. Consequently, MLPs have historically shown a weaker correlation to energy prices over longer periods as MLPs act more like energy toll roads, profiting on the volume of oil moving through their pipelines.

Some market observers are concerned that some of the holdings in AMJ, AMLP and other MLP exchange traded products could follow Kinder Morgan (NYSE: KMI) and slash dividends as an avenue for conserving cash.

Alerian MLP ETF

{kind=link}