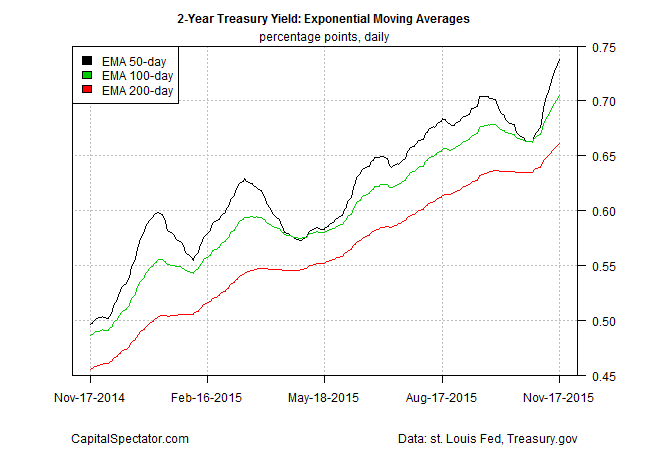

The latest hawkish shift in the 2-year yield is especially conspicuous via a set of exponential moving averages (EMAs) this month.

But if the central bank is planning a rate hike in December, the change in the monetary weather will likely be mild. Note that the annual rate of change in the real monetary base (M0) moved into positive territory last month for the first time since May. We’re still a world below the roughly 20-40%-plus annual increases that marked the full-throttle stimulus of quantitative easing in 2013 and 2014. But after winding down QE to something approximating a neutral state, the Fed is reluctant to go much further at this point on the road to a hawkish transition. Note that tightening episodes in previous decades aligned with real M0 falling in year-over-year terms by as much as 9%. By that standard, the current squeeze is quite mild.

“There is nothing that derails a December Fed rate hike in today’s data [consumer price index and industrial production],” Thomas Costerg, an economist at Standard Chartered Bank, told Reuters on Tuesday. “Inflation is starting to turn a corner and manufacturing production remains resilient.”

The market’s on track with that view. Fed fund futures are pricing in a roughly 70% probability that the policy rate will move above the current zero-to-0.25% target next month, according to CME data.

That’s a reasonable forecast… at least until the next economic report.