Charles Schwab (NYSE: SCHW), the largest custodian of exchange traded funds, has their own suite of ETFs and was an early mover to make smart beta strategies an integral part of investors’ portfolios.

Tom Lydon, editor of ETF Trends, recently sat down with Anthony B. Davidow, vice president for alternative beta and asset allocation strategist at Schwab Center for Financial Research, and talked about how advisors and investors can utilize smart beta strategies in a diversified investment portfolio.

ETF Trends: Strategic beta – or smart beta – receives a lot of attention as one category of factor-based investing. Within the category, there are a number of different types, such as single-factor equal-weight or low-volatility, and perhaps the more common multi-factored, fundamentally-weighted indexes. Do you think investors and advisors understand the variations? Should there be more attention on how the strategic beta strategies differ from one another?

Davidow: We believe that there is a need for better education about strategic beta strategies. While they are often grouped together, equal-weight is very different from low volatility, which is very different from fundamental index strategies. There are even differences among like-strategies.

In our whitepaper, Strategic Beta Strategies: An Evolution of Different Approaches, we provide advisors with guidance on distinguishing amongst the myriad of options available in the market. We think that advisors should begin by understanding the screening and weighting. This helps in anticipating some of the bets and biases that may be introduced, and they’ll have a better sense how to incorporate them in their portfolios.

We also encourage advisors to take note of the underlying indexes, as there can be differences from one index to the next. We then encourage advisors to peel back the onion one layer at a time, evaluating sector allocations, market-capitalization and value-growth tilts.

ETF Trends: You are believers in fundamentally-weighted indexes, but not necessarily as a replacement for market-cap indexes. Can smart-beta index strategies coexist with traditional market-cap index funds within an investment portfolio?

Davidow: We believe that certain smart beta strategies may serve as a compliment to traditional market indexes. Specifically, we believe that fundamental and market-cap indexes are “Better Together.” Market-cap indexes have a larger cap bias, and tend to outperform in environments that reward the biggest (most popular) stocks. They are typically the lowest cost solution and exhibit little to no tracking error. Fundamental Index strategies have been shown to generate excess returns over longer intervals. They will be slightly higher cost than their market-cap equivalent and will exhibit higher tracking error. Based on our research, the combination offers attractive risk-return characteristics.

ETF Trends: If an advisor or investor is supplementing a portfolio with smart-beta or factor-based strategies, what is your general guidance in terms of asset allocation between market cap, fundamental, and active management?

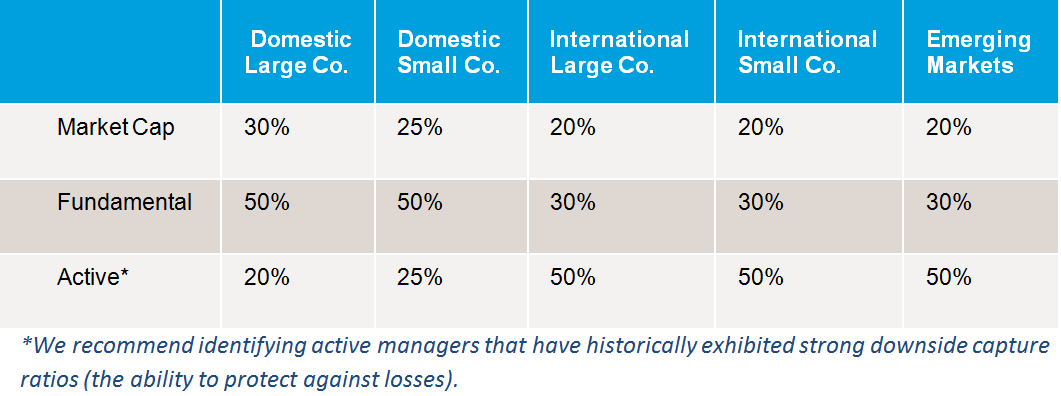

Davidow: Based on our research, we recommend combining active, market-cap and fundamental index strategies. We have found that the combination historically provided better risk-adjusted results. Below please find our recommended allocations across the various sub-asset classes.

{kind=link}

Our research has shown that there is little persistence of active managers generating excess returns in the most efficient markets; therefore we would recommend a higher allocation to Fundamental Indexing for their alpha potential. In the less efficient markets (Emerging Markets), we would recommend a higher allocation to active managers with strong downside capture ratios. Depending upon the market environment, and/or personal views, advisors can adjust the allocations.

ETF Trends: In your paper “Why Fundamentals – Why Now?” you make the case that given where we are in the market cycle, now could be an opportune time to consider fundamentally-weighted strategies. Does the recent market environment change your point of view?

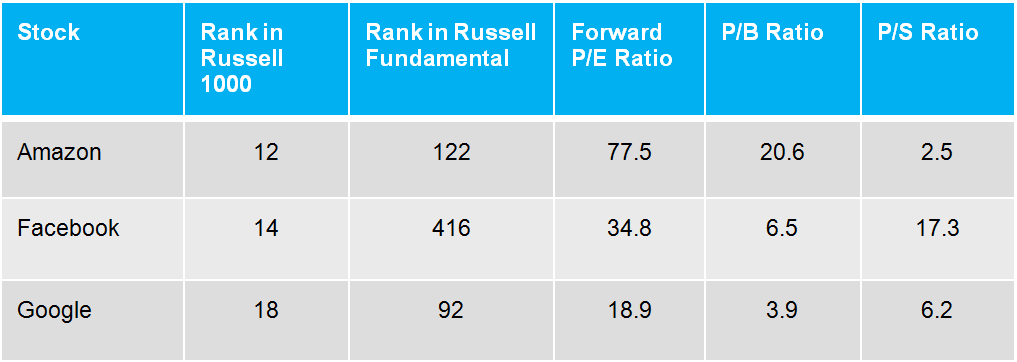

Davidow: In our paper, we make the case that in the early phases of a bull market “a rising tide lifts all ships.” As the bull market matures, we believe that savvy investors pay more attention to strong companies with sound fundamentals. Many of the popular stocks like Amazon, Facebook and Google have large weights in the market-cap indexes without regard to their valuations.

{kind=link}

We believe that fundamental indexing makes sense given the ‘stretched’ valuations and recent market uncertainty. We believe that fundamentals matter.

ETF Trends: Fundamentally-weighted indexes have been around for a long time. Why do you think they are taking off now?

Davidow: A number of factors have led to the increased interest in Fundamental Index strategies. The most important is the fact that these strategies have been battle-tested. Unlike some of the newer strategic beta strategies, the RAFI Fundamental Index strategies are celebrating their 10-year anniversary, and the ‘live’ data has matched the simulated returns presented in the original research. Another important factor is education. The industry has done a better job educating advisors and investors about the merits of these strategies.

ETF Trends: You’re out in the field, talking to clients and advisors all the time. What are they asking you about smart beta strategies?

Davidow: In the early days, the discussions focused on “Do these strategies work?” Now the discussions have become “How do I distinguish amongst the strategies?” and “How do I use them to build portfolios?”