Stocks and bonds have been on a tear in recent years. As interest rates fell to historic lows, the Barclays U.S. Aggregate Bond Index rose 4.84% between September 2008 and June 2015. The S&P 500 Index gained 11.22% over the same period, with U.S. stocks surpassing one record high after another. Investors who focused on stocks and bonds—in a 60/40 portfolio, for example—have been well-rewarded.

This kind of performance can’t last forever. Eventually, interest rates will rise and bond prices will fall. Given the Fed’s hints about short-term rate hikes, that day may already be at hand. Meanwhile, some pundits predict a stock market correction in 2015. The shift in momentum could be swift and dramatic—witness the spike in interest rates during the 2013 “taper tantrum” and the nearly 10% decline in the S&P 500 Index during October 2014—and any rebound may be long in coming.

Don’t let your clients wait until it’s too late. With both stocks and bonds near all-time highs, the downside risks are increasing. At the same time, market volatility has escalated. Liquid alternative strategies can help you hedge risk and reduce portfolio volatility, while providing you with the potential of a positive return, even when stocks and bonds experience large or extended periods of negative performance.

IndexIQ research has shown that the hedge fund universe, on average, has historically delivered between 3% and 6% over the risk-free rate (measured by U.S. Treasury Bills) with about one-third of the volatility of stocks (as measured by standard deviation) and a similar volatility profile to investment-grade corporate bonds (Source: Morningstar, 6/30/15). For example, before the 2008 financial crisis (between December 31, 1998 and August 31, 2008), the annualized return for hedge funds (represented by the Dow Jones Credit Suisse Hedge Fund Index) was 9.69%, or 6.03% over the risk-free rate. Past performance is no guarantee of future results, which will vary.

Pundits have suggested that hedge fund performance has been poor in recent years, compared to the S&P 500 Index. However, that performance profile is to be expected for two reasons.

- As mentioned earlier, hedge funds have historically delivered a return between 3% and 6% over the risk-free rate. Given that the risk-free rate has been near zero since 2008, the absolute performance of hedge funds has been—not surprisingly—between 3% and 6%. And, that was generated with far less volatility (as measured by standard deviation) than the broad equity market.

- Hedge funds are designed to hedge, not keep up with stock market performance. So, in a roaring market, when the S&P 500 Index seems to be going straight up, the average hedge fund is unlikely to keep pace. The big takeaway here is that as interest rates rise, the performance profile of most hedge funds should increase commensurately and at the same time, provide a similar volatility profile as corporate bonds. As such, liquid alternatives that use hedge fund strategies have the potential to add value in a rising rate environment, while helping to insulate an overall portfolio from equity market shocks.

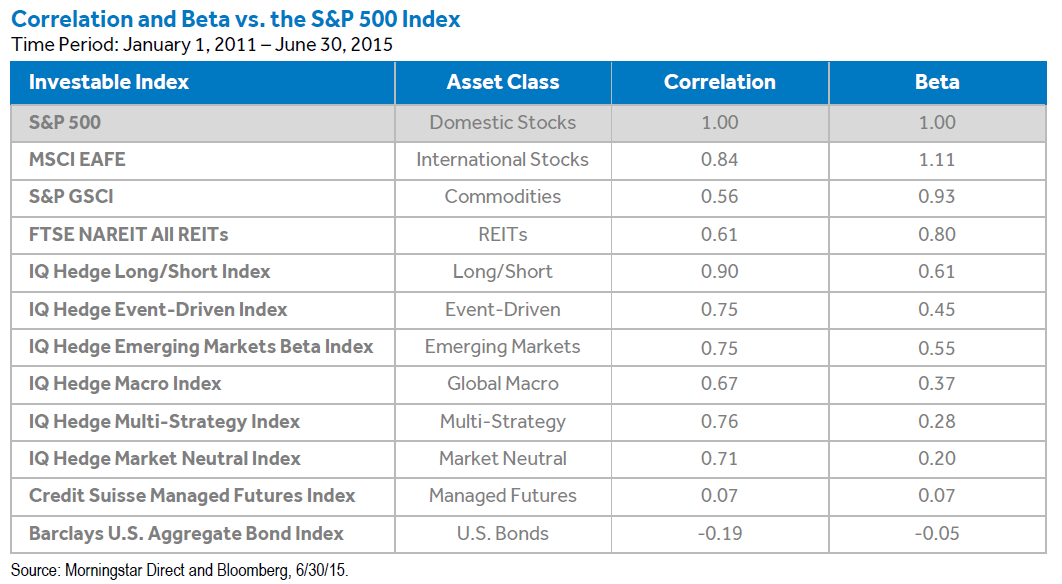

That said, not all liquid alternative strategies are appropriate for every portfolio. The first step is to determine what asset class you are trying to hedge and what kind of risk-adjusted return you are seeking to achieve. For instance, as you cansee from the correlation and beta chart below, the IQ Hedge Macro Index, representing a global macro alternative strategy,* exhibited moderate correlation with the S&P 500 Index. However, correlation measures direction and not magnitude, so beta can be used as a key indicator of diversification. During the same time period, managed futures (measured by the Credit Suisse Managed Futures Index) exhibited both a low correlation and low beta vs. stocks.

Generally speaking, then, if suitable, you might look for a managed futures strategy if you want something that might perform differently than the U.S. stock market. This approach would have been advantageous during 2008 when the S&P 500 Index declined -38.49% and managed futures generated a positive return of 18.33%. Past performance is no guarantee of future results. There may have been times when these strategies underperformed.

*Global macro uses macro analysis (i.e., political trends, macroeconomics, etc.) to help identify dislocations in equity, fixed income, currency, and commodity markets.

{kind=link}

Of course, hedging a total portfolio isn’t an all-or-nothing proposition. Clients should remain well-diversified, with exposure to both stocks and bonds. That said, there is no time like the present to deepen your conversations with clients about asset allocation. Some will be happy to hear from you, given elevated equity valuations and rumblings about higher interest rates. Others may need to hear from you, especially if they are trying to capture every last gain.

In my next post, I’ll discuss how to help clients hedge their fixed income exposure.

About Risk: There are risks involved with investing in any such products, including the possible loss of principal. Investors in the Funds should be willing to accept a high degree of volatility and the possibility of significant losses. The nature of the IQ Hedge products allows for potential benefits, which typically are not associated with traditional hedge funds.

The Funds’ investment performance, because they are funds of funds, depends on the investment performance of the underlying ETFs in which they invest. There is no guarantee that the Funds themselves, or any of the ETFs in the Funds’ portfolios, will perform exactly as their underlying indexes. The Funds are non-diversified and susceptible to greater losses if a single portfolio investment declines than would a diversified mutual fund. The Funds do not invest in hedge funds and are not suitable for all investors.

All ETFs are subject to market risk, including possible loss of principal. Diversification and asset allocation cannot assure a profit or protect against loss in a declining market.

This article was written by Adam Patti, Chief Executive Officer for IndexIQ.