After dropping off from the June highs, Chinese equities and country-specific exchange traded funds may have dipped back to fair market value.

Alexander Redman and Arun Sai at Credit Suisse looked at four different indicators on pricing of MSCI China H-shares and B-shares after the Chinese market sell-off.

For starters, the macroeconomic regression model of MSCI China showed that deviation is now less than 1% after showing the market was 21% overbought during the peak on June 12, reports Julie Verhage for Bloomberg. The measure is based off current levels of U.S. ISM new orders, Chinese industrial production growth, year-over-year growth in property transactions and CPI inflation to predict market returns.

The earnings multiple of MSCI China is trading on a sector-adjusted 9.5 times 12-month forward consensus earnings multiple, or a 16% discount to its 20-year average.

The iShares MSCI China ETF (NYSEArca: MCHI), which tracks the MSCI China Index, is hovering around a 10.5 price-to-earnings. Other China H-shares-related ETFs are also trading at cheaper multiples. For instance, the iShares China Large-Cap ETF (NYSEArca: FXI), the largest China-related ETF that tracks Chinese companies listed on the Hong Kong stock exchange, has a 9.8 P/E and the SPDR S&P China ETF (NYSEArca: GXC) has a 10.4 P/E.

The China H-shares-related ETFs are also showing more attractive valuations relative to the China A-shares market where the Shanghai Composite and the small-cap Shenzhen Composite are still relatively expensive, even after the correction, trading at an average price-to-earnings ratio of about 20 and 50 times, respectively. [Interested in China? H-Shares ETFs Are a Cheap Play.]

The Credit Suisse analysts also believe that Chinese have “recoupled with its long-run association with MSCI China year-on-year performance” after a disconnect in June – earlier in the year, the market showed strong performance momentum but a large number of negative earnings revisions.

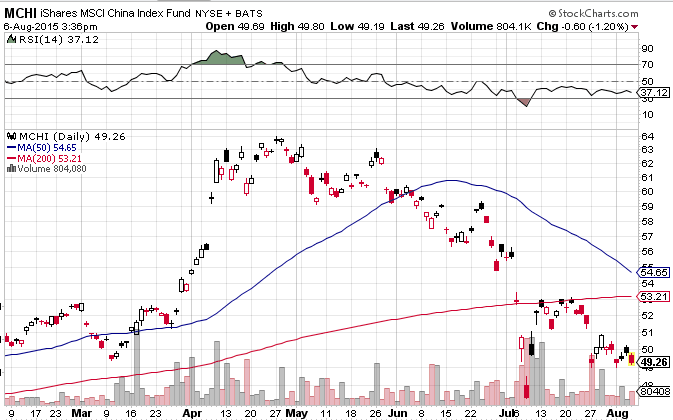

Technical indicators, such as the 200-day moving average and relative strength, also show that the market froth may have dissipated. The market experienced a rapid decline from trading at over 20% above 200-day to slightly negative. Additionally, the relative strength index of MSCI China has fallen off from overbought to near oversold levels.

iShares MSCI China ETF

{kind=link}

For more information on the Chinese markets, visit our China category.

Max Chen contributed to this article.