Through the first half of 2015, no fixed income exchange traded funds are among the top 10 asset-gathering ETFs. There were not any bond funds on the list of the 10 worst ETFs as ranked by outflows, either.

However, with 10-year Treasury yields up 24.3% over the past 90 days and fixed income managers, investors and traders continually eyeing a late-year rate hike by the Federal Reserve, now looks like an ideal time to consider alternatives to the widely followed Barclays U.S. Aggregate Bond Index.

“For most of the last 30 years, investors in the Agg consistently generated mid- to high-single digit returns because 10-year Treasury bonds were yielding at least 4% until the financial crisis in 2008.1 However, beginning in 2011, rates on the 10-year began to decline, and currently hovers just above 2%.2 In this environment, it is increasingly difficult to use a standard bond portfolio to generate the kind of returns, let alone income, that many investors require,” according to a new research note from State Street Global Advisors (SSgA).

ETFs that use the aggregate bond approach are wildly popular. The Vanguard Total Bond Market ETF (NYSEArca: BND) has $27.2 billion in assets under management and the iShares Core U.S. Aggregate Bond ETF (NYSEArca: AGG), which tracks the Barclays Aggregate Bond Index, is a $24.7 billion ETF. The Barclays Aggregate Bond Index has some drawbacks.

As SSgA notes, that index excludes high-yield corporate bonds and, like so many equity-based ETFs, is cap-weighted, meaning it tilts toward the largest issuers, namely Uncle Sam.

“The index is market-cap-weighted, i.e., it tilts to the biggest bond issuers. As a result, the Agg’s allocation to US government debt—Treasuries and Mortgage Backed Securities, two fixed income asset classes that are highly sensitive to rising rates—has climbed to more than 60%.The Agg’s largest individual sector allocation is to Treasuries, one of the lowest-yielding sectors in the US fixed income market,” said SSgA. [Time to Jump for Junk Bond ETFs? Maybe]

An added risk is that the Barclays Aggregate Bond Index has seen its duration climb by more than a year to 5.5 years since 2009, according to SSgA. That could make the index vulnerable to rising interest rates. Duration measures a bond’s sensitivity to interest rate changes.

While the allure of an aggregate bond ETF is obvious, such funds deliver cost-effective exposure to a broad swath of the fixed income universe, advisors and investors can use multiple ETFs for even broader coverage while mitigating duration issues. [Big Demand for Bond ETFs]

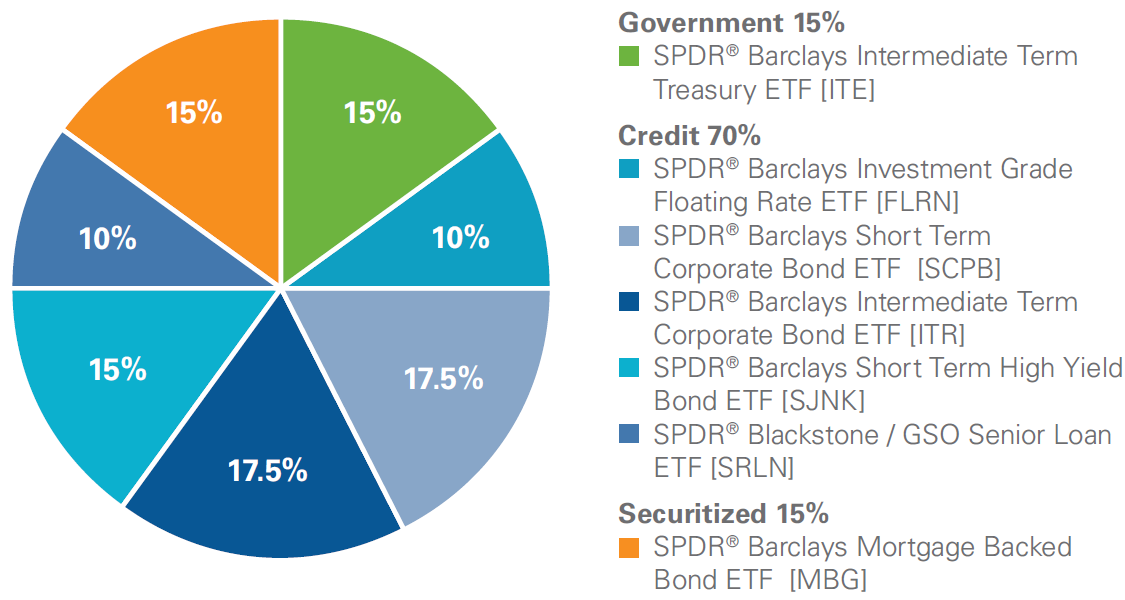

A hypothetical fixed income ETF portfolio proposed by SSgA includes 15% exposure to high-quality U.S. government debt by way of the SPDR Barclays Intermediate Term Treasury ETF (NYSEArca: ITE) as well as a 15% weight to mortgage-backed securities with the SPDR Barclays Mortgage Backed Bond ETF (NYSEArca: MBG).

The hypothetical portfolio also heavily tilts toward credit with 70% of its weight devoted to corporate bond funds, including some high-yield fare.

The SPDR Barclays Short Term High Yield Bond ETF (NYSEArca: SJNK) is one member of the portfolio and a worthy one at that with a 30-day SEC of 5.37% and a modified adjusted duration of 2.41 years. SJNK’s duration is lower than that of traditional junk bond ETFs, potentially making the fund a better high-yield bet if and when interest rates rise.

SJNK’s exposure to energy issuers is also below that of its longer duration rivals, an important factor to consider as credit markets price in the impact of flailing oil prices on high-yield energy issuers from that sector. [Warnings for Junk Bonds With Big Energy Exposure]

SSgA Model Bond Portfolio

{kind=link}

Chart Courtesy: SSgA