While the VIX may suggest “complacency” with a $12 or $13 handle as it has had lately, we sense that a “Risk On” mentality would be a false conclusion to make here based on other signs we are seeing in the markets.

We already pointed out the larger redemption activity in Small Caps via IWM (iShares Russell 2000, Expense Ratio 0.20%) and the fund itself sliced viciously through its 50 day MA yesterday

without batting an eye.

Today it is not faring much better, down about 0.65% and trading at its lowest levels since earlier this month. On this sloppy trading activity we have seen a notable $1.7 billion flow out of the fund which is not an inconsequential amount given the fund’s total asset base (about $29 billion) and especially with the current swoon in price. Elsewhere, it is hard for us to ignore the plunging prices in the High Yield Corporate Bond arena as well, which we also monitor as a good reflection of whether we are in a “Risk On” or “Risk Off” environment.

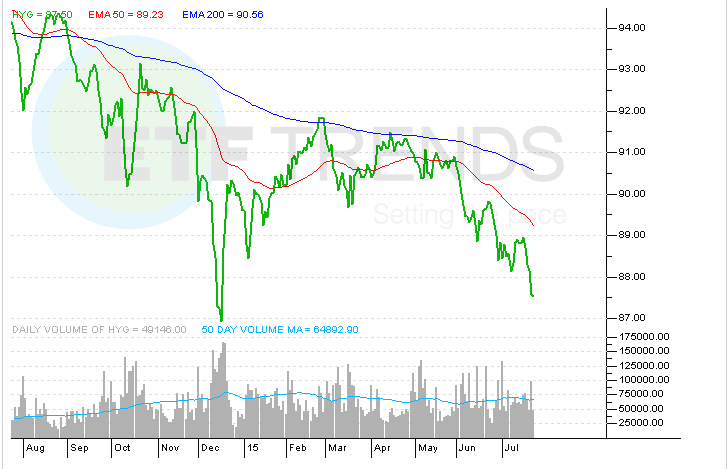

The charts of the two largest High Yield Corporate Bond ETFs, HYG (iShares High Yield Corporate Bond, Expense Ratio 0.50%, $14.2 billion in AUM) and JNK (SPDR High Yield Bond, Expense Ratio 0.40%, $9.9 billion in AUM) should be very concerning to Bond bulls in the HY Corporate space, as we are currently trading at 2015 lows and have given up a lot of ground just in the past six trading sessions.

HYG for example sliced through its 200 day MA with reckless abandon and has not looked back since. Interestingly, fund flows given this swoon have not been gigantic yet, as JNK has seen about $285 million leave via redemption activity while HYG’s flows have been relatively flat in the trailing one month period even with the evident selling pressure.

The yields of HYG and JNK have climbed to 5.46% and 5.89% respectively, but we are not exactly seeing managers race to buy these ETFs, at least not yet and we suspect that the plunge in Oil prices and its effects on the Oil Services and Exploration equity markets is certainly not helping the cause here.

For it is well known that many Exploration companies are issuers of what is considered “Junk” debt, and this unabated price pressure in Oil and energy prices cannot be ignored. The Fed has commented on how they believe that lower oil prices are a “net positive” for the economy in the past, but interestingly we have not heard such rhetoric from them yet this time around, but cannot rule such future comments out of course since the Fed tends to speak about the “economy” several times a week whether there is a rate decision or not these days.

iShares iBoxx $ High Yield Corporate Bond ETF

{kind=link}

For more information on Street One ETF market commentary and ETF trade execution/liquidity services, contact Paul Weisbruch at pweisbruch@streetonefinancial.com

Street One Financial is an educational/research firm utilizing the Broker Dealer services of Precision Securities, a FINRA registered Broker/Dealer.