What makes a great index? A typical response might be “performance” – particularly with reference to smart beta indexes which may offer the potential for enhanced index returns over traditional market capitalization indexes. But performance isn’t the only — or even the most important — way to gauge the value of a benchmark. The better index, therefore, isn’t necessarily the one with the best returns; rather it is one that clearly defines the universe of securities it is measuring, doing so consistently with disciplined, transparent methodology.

The Russell 2000® Index is a prime example. It is a market cap-weighted index, designed for a single purpose: to provide investors with a tool for measuring the performance and characteristics of the small-cap segment of the U.S. equity universe. It has become the most widely followed small cap benchmark in the U.S. institutional marketplace because of the accuracy with which it reflects this small-cap sector. It does this by adhering strictly to several basic rules:

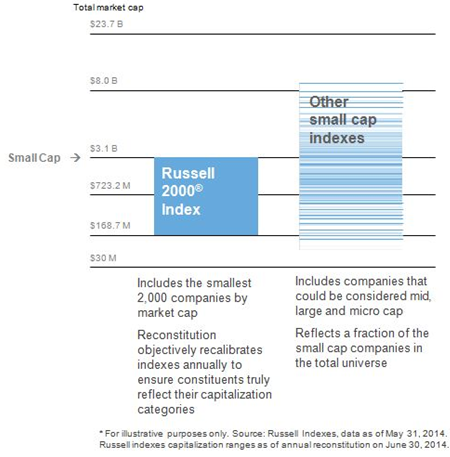

The Russell 2000 Index is comprehensive. Many competing indexes claim to represent the small cap segment of U.S. equities, but none are fully comparable: some are subsets, some have gaps, and others blur the lines between small stocks and large/mid cap stocks. The Russell 2000 comprehensively covers the investable U.S. small cap market.

Market coverage of the Russell 2000 Index vs. other indexes

{kind=link}

The Russell 2000 stays home. Smart beta indexes are specifically designed to efficiently increase or reduce exposures to certain factors like quality, value, momentum and volatility. The Russell 2000 is intended to be a factor-neutral basket of stocks, and doesn’t employ any rules that intentionally produce factor tilts like those found in many smart beta indexes. If an investor has a belief about a certain factor there are no shortage of options with which to complement their intended allocation to U.S. small cap stocks. But if they want exposure to the broad universe of U.S. small cap stocks, the Russell 2000 was built and is maintained for this purpose.

The Russell 2000 is unbiased. The Russell 2000 follows a transparent and rules-based methodology, not subjective decision making. It doesn’t include (or exclude) a stock when a committee reaches consensus, but only when the market decides the company is of sufficient size. There are no preferences for specific companies or sectors over others because the methodology’s singular goal is to identify the 2000 stocks that reflect the entire U.S. small cap market.

Ultimately, investors should choose indexes as tools that allow them to best research and execute their personal asset allocation and investment decisions.

To learn more about the Russell 2000, with links to quarterly reports and other small cap videos and content, please visit MethodologyMatters.com. Yes, your index methodology matters.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.