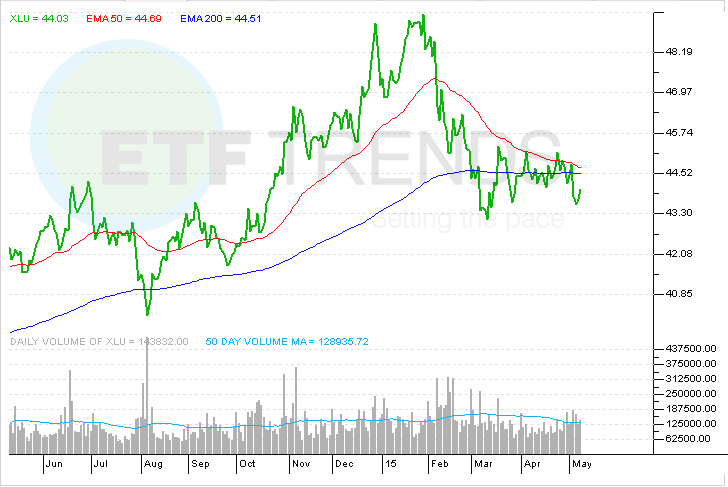

Just a few months after wrapping up 2014 with a nearly 29% gain, good enough to make it the best of the nine sector SPDR exchange traded funds, the Utilities Select Sector SPDR (NYSEArca: XLU) is saddled with a 6% year-to-date loss.

That makes XLU, the largest utilities ETF by assets, this year’s worst performer among the nine SPDRs. XLU’s struggles, and those of rival utilities ETFs, underscore the notion that rate sensitivity for select asset classes is a legitimate concern at a time when so many market observers cannot resist the temptation of saying 2015 will finally be the year the Federal Reserve raises interest rates. [Rate-Sensitive ETFs get Jammed Up]

Still, 10-year yields Treasury yields have traded slightly lower this year, but there is a case for embracing utilities and ETFs like XLU on the basis of steady earnings growth despite the sector’s slow-growth reputation.

“Many view utilities as a no-growth business given little change in U.S. electricity consumption in recent years. However, earnings growth has averaged 4% annually in the past decade and profits could grow at a similar rate in coming years as utilities upgrade or replace aging transmission lines and power plants. Much of the U.S. utility infrastructure is more than 40 years old,” reports Andrew Bary for Barron’s.

The $6 billion XLU yields almost 3.5%, the highest among the nine sector SPDRs, and several of the ETF’s largest holdings yield more than 4%. That is the case for Southern Co. (NYSE: SO), Consolidated Edison (NYSE: ED) and Duke Energy (NYSE: DUK). That trio combines for nearly 20% of XLU’s weight.

Utilities high yields and steady earnings growth does not come cheap. “In late January, the median U.S. utilities valuation hit the highest level ever since Morningstar began covering utilities,” according to Moringstar‘s director of utilities equity research. “The February swoon cut that premium in half. We also cut our cost of capital assumption in our discounted cash flow valuations to reflect historical inflation and real interest rates, bringing valuation premiums down another 10%. As of mid-March, utilities’ median valuation was only slightly above market prices and in line with valuations in late 2013 before the 27% run in 2014.” [A Contrarian View of Utilities ETFs]

The sector trades “for an average 16.4 times estimated 2015 earnings. However, the sector is at a 5% discount to the Standard & Poor’s 500 price/earnings ratio based on projected 2015 earnings,” according to Barron’s.

Rising rate fears continue to chase investors from utilities ETFs. Last month, investors pulled a combined $533 million from consumer staples and utilities ETFs, according to State Street data. As of May 5, investors had pulled over $835 million combined from XLU and the rival Vanguard Utilities ETF (NYSEArca: VPU). [Trouble for Bond Proxy ETFs]

Utilities Select Sector SPDR

{kind=link}