Frontier markets have yet to shed their rough and tumble reputation. Perhaps countries with that designation, but just a year ago, the iShares MSCI Frontier 100 ETF (NYSEArca: FM) was one of the most prominent international exchange traded funds.

In the run-up to Qatar and the United Arab Emirates joining the MSCI Emerging Markets Index, FM, which as of May 29, 2014 allocated 38% of its combined weight to those countries, surged. Not only did FM soar, it delivered notable out-performance of the iShares MSCI Emerging Markets ETF (NYSEArca: EEM).

However, index changes are not harbingers of declining commodities prices and although FM shed two OPEC members in Qatar and UAE, it was still left cartel members Kuwait and Nigeria, two countries that now combine for 37% of the ETF’s weight. Not to mention, FM allocates about a third of its combined weight to countries rich in energy resources, including Pakistan, Kenya, Oman, Morocco and Kazakhstan. That is to FM participated in oil’s downside last year. [Oil Drains Frontier ETFs]

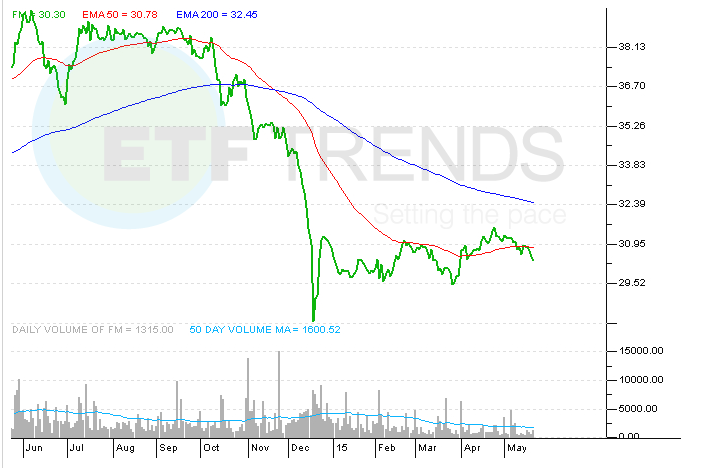

Still, FM managed to outperform EEM last year, as it did in 2013, but with the former down this year, this could be the first full trading year that the frontier fund lags its emerging markets counterpart.

“The investment case for frontier markets sounds enticing. Countries such as Kuwait, Nigeria, and Pakistan are at an earlier stage of development relative to emerging-markets economies. Many frontier-markets economies are entering a period of mid- to high-single-digit growth, thanks to a very low economic base, favorable demographics, growth in infrastructure spending, and, in some cases, abundant natural resources. And relative to emerging markets, certain frontier countries will benefit from the rapid adoption and dissemination of ‘new economy’ services such as mobile banking and mobile payments, which should contribute to growth in the medium term,” according to Morningstar.

That is the long-term view and one that could easily be validated with time. In the here-and-now, FM needs to see a sustained rally in oil prices. FM’s year-to-date loss nearly matches that of the Global X Nigeria Index ETF (NYSEArca: NGE). Until recently, Vietnamese stocks have been a drag on FM as the Market Vectors Vietnam ETF (NYSEArca: VNM) is off nearly 8% this year. [Quiet Rally for the Vietnam ETF]

Argentina is FM’s second-largest country weight behind Kuwait, but the 16.2% gained this year by the Global X MSCI Argentina ETF (NYSEArca: ARGT) has not been enough to prop up FM. Along with the new Global X MSCI Pakistan ETF (NYSEArca: PAK), ARGT, NGE and VNM are the single-country ETFs offering access to the nations found in FM’s lineup.

As Morningstar notes, FM still possesses its familiar advantages of low correlations and reduced volatility relative to the MSCI Emerging Markets Index. For example, NGE has a beta of just 0.64 to the MSCI Emerging Markets Index while VNM has a correlation to the S&P 500 of just 0.47, according to Market Vectors data.

“Over the past few years, during “risk-off” periods, volatility in emerging-markets stocks has been exacerbated by fickle foreign fund flows. With low levels of foreign ownership in frontier-markets lass has not been as susceptible to volatile foreign fund flows (except in extreme stocks and bonds, however, this asset c events such as the 2008 financial crisis). However, frontier markets’ correlations will increase should foreign ownership in frontier-markets stocks continues to rise,” according to Morningstar. [Now There’s a Pakistan ETF]

iShares MSCI Frontier 100 ETF

{kind=link}