There is still plenty of discord regarding when the Federal Reserve will officially hike interest rates. Perhaps it be September or maybe it will be next year.

One thing is clear and that is 10-year Treasury yields have surged 17.5% over the past month. Another thing that is clear is that as interest rates rise, investors do not need to flee all bonds and fixed income exchange traded funds.

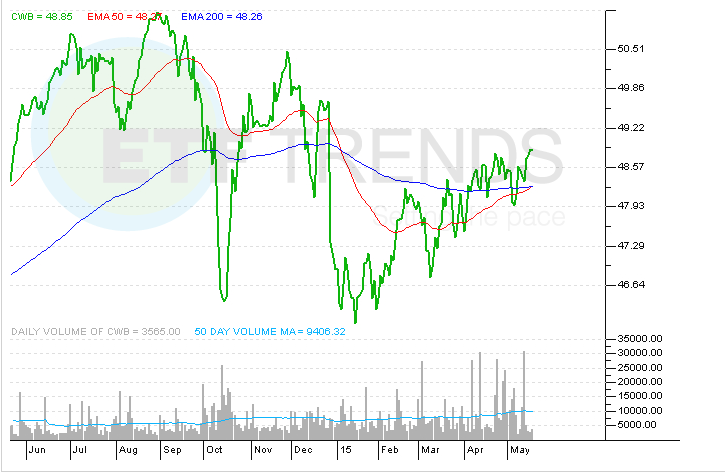

The SPDR Barclays Convertible Securities ETF (NYSEArca: CWB) is one of the, if not the premier bond ETF for rising rate environments. CWB’s one-month gain of nearly 1% is not jaw-dropping, but it does confirm the ETF’s durability when Treasury yields and it is undoubtedly better than the 8.4% lost by the iShares 20+ Year Treasury Bond ETF (NYSEArca: TLT) over the same period.

Convertible bonds are a type of hybrid fixed-coupon security that allow the holder the option to swap the bond security for common or preferred stock at a specified strike price. Due to the bond’s equity option, convertible bonds typically pay less interest than traditional corporate bonds. The fund, though, does not convert its holdings into shares, but investors are exposed to the equity premium due to the way the bonds are priced. [A Bond ETF To Diminish Volatility and Boost Yields]

Today, the $3.1 billion CWB is the lone dedicated convertibles ETF on the market and though the fund turned six last month, convertibles have been around longer than many investors realize.

“The first convertible bonds were issued in the mid-1800s to finance the new technology of the time, railroads,” said State Street Vice President and head of Research Dave Mazza. “A means of attracting interest in the asset class was the ability to provide a current income stream with the embedded option for potential upside if the venture was profitable.”

When the equities market dips, convertibles moves away from the price at which they can be exchanged for the stock and act more like fixed-income assets. On the other hand, as equities rise, convertibles will act more like stocks. Consequently, the asset class can have smaller up and down swings.

Because of its equity-like traits, CWB 30-day SEC yield is just 1.67% is closer to the dividend yield on the S&P 500 than the yield on 10-year Treasurys though below both. CWB’s yield is also low relative to other corporate bond ETFs sporting the junk label, of which CWB is one with an average credit rating of Baaa1 among its 103 holdings. Still, CWB has its advantages.

“As a result, the result of the allocation to consumer discretionary and information technology sector, the fund has a cyclical tilt,” said Mazza. “In our current, slow growth expansion, convertibles offer cyclical growth exposure, but have the added benefit of stable income and a bond floor if prospects go south.” [Convertibles on the Cheap]

Other CWB advantages include convertibles’ status as the top-performing bonds when rates rise and an expense ratio of just 0.4%, more than 70 basis points below the average actively managed convertible bond mutual fund.

SPDR Barclays Convertible Securities ETF

{kind=link}