After the sudden surge in Hong Kong-listed Chinese equities and related exchange traded funds, some are beginning to question the fundamentals, notably the potential weakness among China’s big banks.

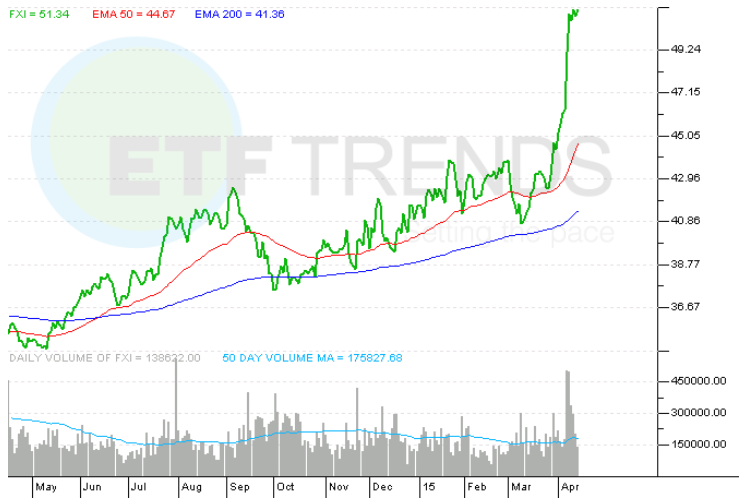

Over the past month, the iShares China Large-Cap ETF (NYSEArca: FXI), the largest China-related ETF that tracks Chinese companies listed on the Hong Kong stock exchange, rose 20.6% Similarly, other China H-shares ETFs have strengthened, with the SPDR S&P China ETF (NYSEArca: GXC) up 19.3% and the iShares MSCI China ETF (NYSEArca: MCHI) 20.3% higher so far this year. [China H-Shares ETFs Get Their Moment in the Limelight]

Meanwhile, the Hang Seng China Enterprise Index, a gauge of mainland large-cap stocks traded in Hong Kong, has gained 21% this year.

Analysts, though, are predicting an earnings decline for these mainland Chinese companies for the year, the Wall Street Journal reports.

“Earnings growth has been pedestrian, and earnings estimates have been progressively settling down,” Manishi Raychaudhuri, BNP Paribas’s Asia equity strategist of Hong Kong-listed China stocks, said in the WSJ article. “This equity rally has been uncorrelated with the economic fundamentals and corporate earnings, which are supposed to be the lifeblood of all equity-market rallies.”

Many bullish investors are pointing to the cheap valuations in the Chinese stocks. The Hang Seng was trading around an estimated 9.2 forward earnings, which was below its 10-year average even after the recent rally. Looking at the China H-shares ETFs, FXI has a 10.7 P/E, GXC has a 10.8 P/E and MCHI has a 11.1 P/E.

However, observers have pointed out that the Index is so cheap because of its significant tilt toward big banks and other state-owned companies that are trading at low multiplies, which reflect the companies’ slowing profit growth and uncertain outlook.

“The earnings-growth outlook is now highly variable by sector—in particular, the outlook for big index [sectors]such as banks and energy is highly opaque driven by [nonperforming-loan] recognition, credit costs and oil prices,” Charlie Awdry, a manager at Henderson Global Investors, said in the article.

China ETF investors should take not as the financials sector makes up a significant portion of the related fund products. For instance, financials make up 47.1% of FXI, 28.8% of GXC and 37.6% of MCHI.

Nevertheless, this has not deterred investors as many are looking at the cheap discounts in Chinese company shares listed in Hong Kong. According to the Hang Seng China AH Premium Index, stocks on the Hong Kong bourse are trading at a 32.89% discount to mainland markets. In comparing valuations, the db X-trackers Harvest CSI 300 China A-Shares Fund (NYSEArca: ASHR), which tracks mainland Chinese A-shares, is showing a 14.4 P/E ratio. [Surprising Drivers of the A-Shares ETF Surge]

“Sometimes it happens in the last leg of a rally where people don’t look at fundamentals,” Rahul Chadha, co-chief investment officer at Mirae Asset Global Investments of China equities, said in the WSJ article. “If you chase momentum, it can hurt very badly.”

iShares China Large-Cap ETF

{kind=link}

For more information on China, visit our China category.

Max Chen contributed to this article.