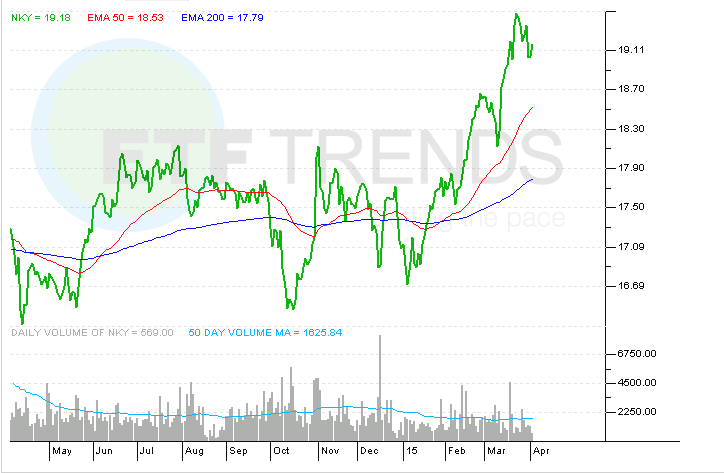

An ETF that we profiled back on February 24th, NKY (Maxis Nikkei 225) has seen substantial inflows early this week, with more than $1.75 billion entering the fund, leading all ETFs in the near term.

With the U.S. Dollar weakening to global currencies recently such as the Japanese Yen, this may be a timely trade in terms of passing on the “currency hedge” that has made ETFs such as DXJ (WT Japan Hedged Equity) so, so popular in the past couple years (the fund has >$16.1 billion in AUM including almost $3 billion that has been created just YTD). EWJ (iShares MSCI Japan, Expense Ratio 0.48%) is no slouch either, having pulled in about $1 billion in new assets via creation year to date, and still maintaining an edge over DXJ as the largest Japan Equity focused ETF in the U.S. listed landscape.

DBJP (Deutsche MSCI Japan Hedged Equity, Expense Ratio 0.45%) and HEWJ (iShares Currency Hedged MSCI Japan, Expense Ratio 0.48%) have also made their mark in recent times with $931 million and $356 million in assets under management respectively, primarily raised in an environment of a prolonged Yen slump against the U.S. Dollar.

As we mentioned, global currencies have largely rallied against the U.S. Dollar since the mid-March lows, but the question remains if this is simply a short term bear rally or the beginning of a trend reversal.

If global currencies, in particular the Yen begin to climb steadily versus the U.S. Dollar, we have to think that the Currency Hedged products in this Japan equity space become less appealing in general as investors may be more comfortable embracing unhedged products, such as NKY for instance, if not an EWJ or various other straight equity unhedged funds in the space including Japan Small Cap.

Thus, with appetite for Japan Equity exposure on the climb for the past several years, the future should be very bright for newer funds to the space such as NKY as well as smaller and lesser known funds that grant exposure to the Japanese equity market, hedged or unhedged, such as DFJ (WT Japan SmallCap, Expense ratio 0.58%), FJP (FT Japan AlphaDEX, Expense Ratio 0.80%), DXJS (WT Japan Hedged SmallCap Equity, Expense Ratio 0.58%), SCJ (iShares MSCI Japan Small-Cap, Expense Ratio 0.48%), DXJR (WT Japan Hedged Real Estate, Expense Ratio 0.43%), DXJF (WT Japan Hedged Financials, Expense Ratio 0.43%), DXJT (WT Japan Hedged Tech,

Media, and Telecom, Expense Ratio 0.43%), DXJH (WT Japan Hedged Health Care, Expense Ratio 0.43%), and DXJC (WT Japan Hedged Capital Goods, Expense Ratio 0.43%) for example.

Maxis Nikkei 225 Index Fund

{kind=link}

For more information on Street One ETF market commentary and ETF trade execution/liquidity services, contact Paul Weisbruch at pweisbruch@streetonefinancial.com

Street One Financial is an educational/research firm utilizing the Broker Dealer services of Precision Securities, a FINRA registered Broker/Dealer.