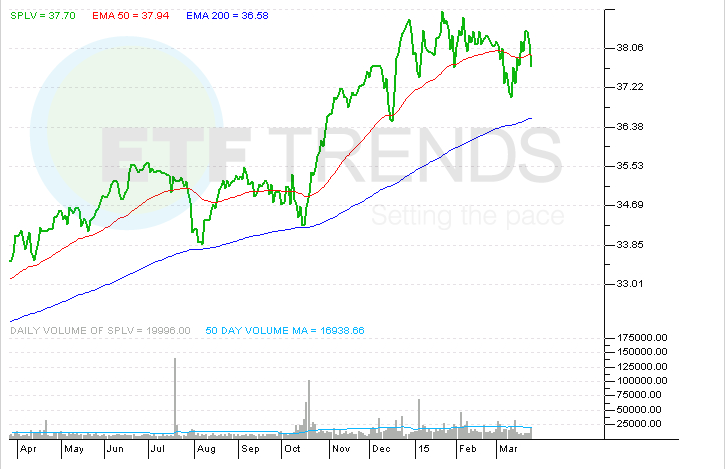

Low volatility entered the investment lexicon over four decades ago, but the concept has received increase attention over the last several years thanks in large part to advent of popular exchange traded funds, such as the PowerShares S&P 500 Low Volatility Portfolio (NYSEArca: SPLV).

With the growth of ETFs like SPLV, evaluation of low volatility as a beneficial investment concept has evolved more to understanding how various low volatility indexes are constructed from examination of the low volatility effect in a broader sense. Said another way, investors like knowing how and why ETFs like SPLV have outperformed at various as much or more than simply knowing the low volatility effect works. [Relax With Low Vol ETFs]

To be sure, the S&P 500 Low Volatility Index, SPLV’s underlying index, has notched notable out-performance of traditional benchmarks.

“In the U.S., for example, the S&P 500 Low Volatility Index outperformed its benchmark, the S&P 500, from 1991 to 2014 by 101 bps compounded annually—with 31% less volatility,” according to a note by S&P Dow Jones Associate Director of Index Strategy Fei Mei Chan.

Over its relatively short lifespan (it turns four in May), SPLV has been criticized as quasi-utilities ETF. Indeed, when Treasury yields tumbled in 2014, SPLV outperformed the S&P 500 by nearly 400 basis due in part to the ETF’s large weights to the utilities and consumer staples sectors.

However, SPLV has managed to again be less volatile than the S&P 500 this year with financial services as its top sector weight. SPLV’s weight to financials is over 37%, more than double the ETF’s weight to consumer staples and nearly triple its weight to utilities. [Surprises in Low Volatility ETFs]

Knowing that SPLV’s holdings are selected based on trailing 12-month volatility, it is not unreasonable to surmise that over that period, utilities were more volatile than financials and staples, SPLV’s two largest sector weights. That is anecdotal, but it underscores the importance of the sector effect on SPLV’s ability to deliver on the promise of reduced volatility.

“However, strategic sector tilts don’t paint the complete picture here. If we only apply the returns of the S&P 500 sectors to the respective sector weights in S&P 500 Low Volatility Index over the last 24 years, the “hypothetical” low volatility portfolio can account for 69% of the total risk reduction. This means that being in the “correct” sector during this period accounted for more than two-thirds of the volatility reduction achieved by the S&P 500 Low Volatility Index,” according to S&P Dow Jones Indices.

PowerShares S&P 500 Low Volatility Portfolio

{kind=link}