Oil’s tumble has taken a toll on a bevy of equity-based exchange traded funds, perhaps none more so than oil services ETFs.

Earlier this year, Goldman Sachs estimated that $930 billion in global oil projects would not be profitable if Brent crude traded at a $70 handle. Brent for April delivery closed just under $57 per barrel during U.S. trading Thursday, indicating that if the price range (or lower) persists, more projects will be scrapped and more rigs will be sidelined. [Almost $1T in Oil Projects at Risk]

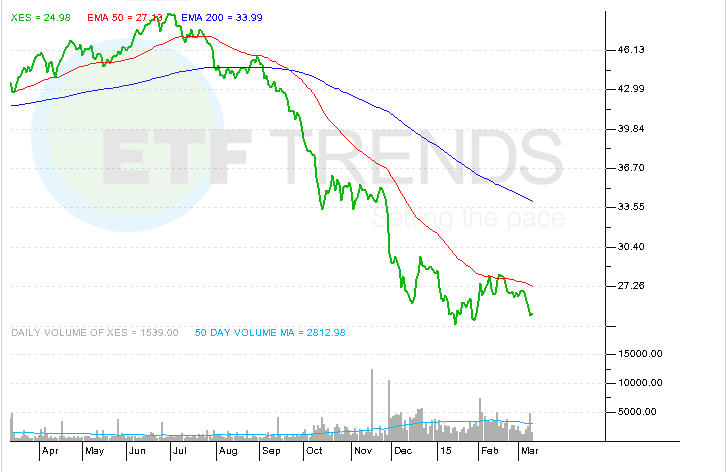

Oil services stocks and ETFs such as the SPDR Oil & Gas Equipment & Services ETF (NYSEArca: XES) have a tendency to overshoot moves in oil futures. For example, XES is down 11.8% over the past month, a decline that is 300 basis points worse than that of the United States Brent Oil Fund (NYSEArca: BNO).

Suspended dividends and dwindling rig counts are among the catalysts that have pressured oil services ETFs, but those lower rig counts are helping boost efficiency.

“Since last summer oil prices have fallen by more than 50% and one third of the oil rigs have been shut down,” said State Street Global Advisors Head of Research David Mazza in an email exchange with ETF Trends. “Fewer rigs should equal less oil; however, US energy forecasts show the US will pump almost 8% more oil this year, reaching levels not seen since 1972.”

Mazza notes that as older, less efficient rigs come offline, oil producers and the services providers held by XES can focus on more profitable areas of exploration, such as deep water and select shale plays.

“New wells can cost approximately $12 million to drill, which is paid up front with a long term payoff to recoup those costs. Thus, it is not practical to stop pumping oil from wells that have already been drilled. Between 2009 and 2012 the number of oil rigs increased 700%, meanwhile production increased 50%. We are seeing those investments results today in increased production,” adds Mazza.

XES is an equal-weight ETF and that methodology reduces the fund’s leverage to the industry’s largest names, XES could benefit more than its rivals if oil services mergers and acquisitions activity increases. Additionally, XES features no exposure to SeaDrill (NYSE: SDRL) and Transocean (NYSE: RIG), two of the now infamous dividend cutters from the oil services group. [A Different Type of Oil Services ETF]

There are some glimmers of hope for XES, particularly if West Texas Intermediate, the U.S. benchmark crude contract, can claw its way back above $50 per barrel after settling just under $47 on Thursday.

“The price of crude has fallen below $50 a barrel,; however, many shale fields remain profitable under a $50 price level and have a production cycle of about 18 months. So, there is a lag component to this environment of falling oil prices versus production output,” said Mazza.

SPDR Oil & Gas Equipment & Services ETF

{kind=link}