The Reserve Bank of Australia surprised global financial markets in early February when it pared Australia’s benchmark interest rate by 25 basis points to a record low of 2.25%.

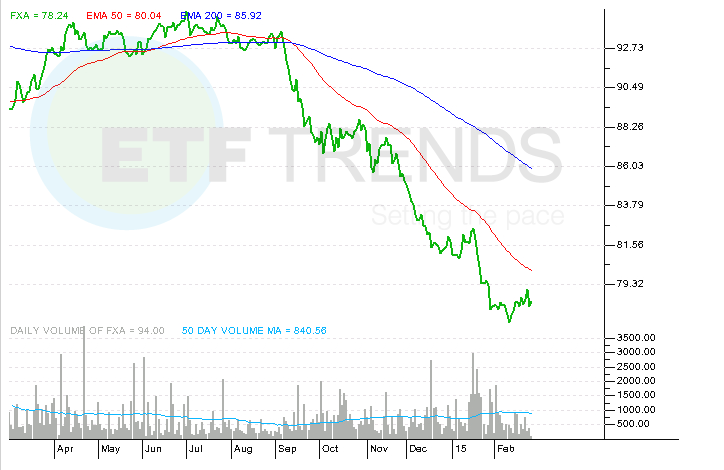

To its credit, the CurrencyShares Australian Dollar Trust (NYSEArca: FXA) was able to muster a modest February gain, but investors might do well to avoid big bets on the Aussie rallying against the U.S. dollar because RBA may not yet be done lowering interest rates.

“Australia has room for 9 quarter point cuts before zero is hit. But cuts won’t happen that way. Accompanied by some sort of shock-and-awe statement, I expect Australia to cut rates 100 basis points or more at some point,” writes Mike Shedlock of Mish’s Global Economic Trend Analysis.

While a 100-basis point cut at one meeting would be a stunning move by RBA, it is impossible to rule out more cuts from a central bank with a somewhat recent track record of doing just that.

RBA’s benchmark cash rate was 4.75% in October 2011. The central bank unveiled 25-basis point cuts at two consecutive meetings later that year. From November 2011 to August 2013, on its way to the 2.5% interest rate, RBA cut rates at eight of 20 meetings.

Now 2.25%, Australia’s benchmark interest rate is not even half the 6% level seen in October 2008 and not even a third of the 7.25% rate seen in March 2008. [Aussie ETFs Brace for More Rate Cuts]

With the RBA eying further downside for the Aussie, the ProShares UltraShort Australian Dollar (NYSEArca: CROC) merits consideration. CROC, which attempts to deliver twice the daily inverse performance of the AUD/USD pair, is down slightly this year.

There are reasons to consider the long CROC thesis.

“Thus, vagueness aside, I will bet on the “over” line, “way over” in fact. With no recession in 23 years, and with wages and prices of goods dramatically out of line with the rest of the world, and with one of the world’s biggest property bubbles, the upcoming recession in Australia will be a doozie,” according to Shedlock.

Assuming RBA is successful in weakening the Aussie further while skirting recession, there are options for investors looking to profit from upside in Australian equities and downside in the currency.

ETF issuers have yet to bring the ultra-hot currency hedging theme to a dedicated Australia ETF, but in lieu of such a fund, the Deutsche X-Trackers MSCI Asia Pacific ex Japan Hedged Equity ETF (NYSEArca: DBAP) is worth a look.

Among multi-country currency hedged ETFs, none can top DBAP’s 22.5% weight to Australian stocks. That makes Australia’s DBAP’s largest country weight. The ETF is up nearly 4% this year. [The Right Currency Hedged ETF for the Times]

CurrencyShares Australian Dollar Trust

{kind=link}