As energy prices plunged, U.S. producers are stashing away their hard-earned oil in storage tanks, fueling a wider spread in contango and potentially cutting into futures-based oil exchange traded fund returns.

In Cushion, Oklahoma, the delivery point for benchmark West Texas Intermediate futures, oil tanks with total capacity of 70.8 million barrels of crude have seen oil stocks double to 41.3 million barrels since October, Financial Times reports.

In a “few months, it will be full,” Alan Swanson, chief financial officer at tank owner Plains All American Pipeline, said in the FT article.

Meanwhile, U.S. commercial crude stocks have expanded at 1 million barrels per day over the past month, and currently sits at about 413.1 million barrels, the largest inventory for this time of year since the Great Depression.

The futures market reflects the current state of oversupply in oil. On Friday, WTI crude for March 2015 delivery was at $51.69 per barrel while delivery for March 2016 was $61.63 per barrel. When later dated contracts are higher than the spot price, the market is in a so-called state of contango. Fundamental factors, including storage costs and other financing costs, help contribute to the higher costs over time.

“When you’re looking at both flat price and at spreads, they’re pretty much indicators of the same thing,” Lawrence Eagles, BP’s head of North American and global crude analytics, said. “If you’ve got too much oil, you have to create conditions where you can store some of that oil. So you get a contango structure.”

WTI crude oil was at about $53.11 per barrel for March 2015 delivery on Monday, compared to $62.56 per barrel for March 2016 delivery, according to CME data.

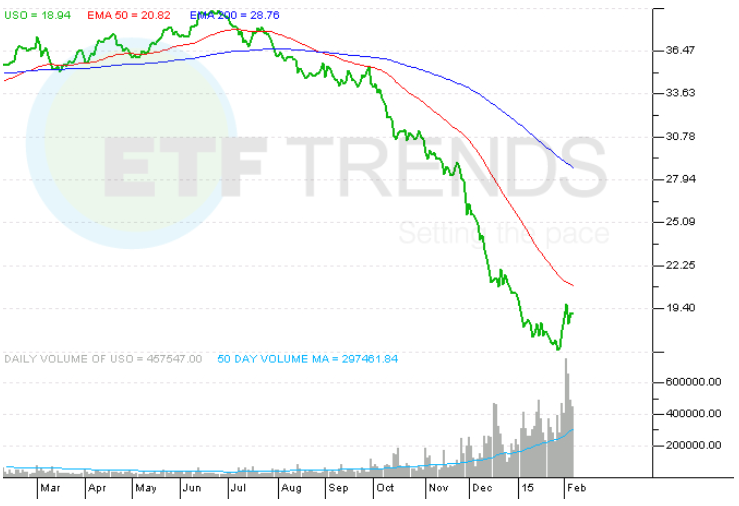

For futures-based ETFs, like the U.S. Oil Fund (NYSEArca: USO), which tracks West Texas Intermediate crude oil futures, the widening contango could eat away at long-term returns. Specifically, USO tracks near month crude oil futures, swapping out contracts within two weeks of expiration for the next month contract. Consequently, in a contangoed market, USO would essentially be selling low and buying high, which may cut into performance. [Positioning for an Oil ETF Rebound? Watch For Contango.]

Alternatively, the PowerShares DB Oil Fund (NYSEArca: DBO) and United States 12 Month Oil Fund (NYSEArca: USL) provide exposure to WTI oil but include a different weighting methodology to limit the negative effects of contango. DBO can include contracts as far out as 13 months and dump contracts at any point. USL, on the other hand, ladders 12 months of contracts to diminish the effects of backwardation and contango.

U.S. Oil Fund

{kind=link}

For more information on the oil market, visit our oil category.

Max Chen contributed to this article.