The last do not always wind up being first, but Russian stocks are giving it a go. Just look at the Market Vectors Russia ETF (NYSEArca: RSX).

One of last year’s worst-performing non-leveraged ETFs, RSX is, to this point in 2015, the year’s best non-leveraged ETF with a gain of 15.2%. Whether it is a case of bargain hunting, a hated asset class rebounding or a combination of the two, volatile Russian equities are rebounding this year and the results extend beyond Russia single-country ETFs.

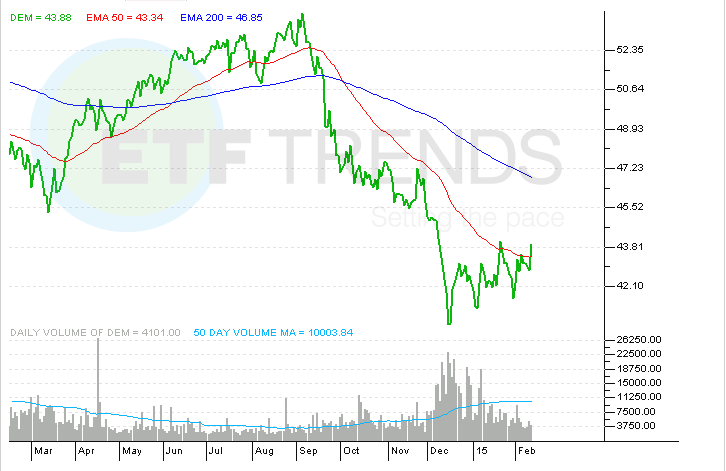

The WisdomTree Emerging Markets Equity Income Fund (NYSEArca: DEM) is a prime example of a diversified emerging markets ETF benefiting from resurgent Russian stocks. DEM, the godfather of emerging markets dividend ETFs, is up 4.1% year-to-date. That is not jaw-dropping, but DEM has outpaced theVanguard FTSE Emerging Markets ETF (NYSEArca: VWO) by 75 basis points and the iShares MSCI Emerging Markets ETF (NYSEArca: EEM) by 170 basis points. [A Return to EM ETFs]

DEM’s weight to Russia, sometimes a burden, sometimes a gift, makes the difference. The ETF allocates 17.1% to Russian stocks, nearly five times the weight allocated to that country by the MSCI Emerging Markets Index.

That sizable Russia weight explains DEM’s struggles last year, but Russia is no longer the ETF’s largest country weight. In November 2014, DEM’s Russia allocation was nearly 20.5%. China, the largest emerging markets dividend payer in dollar terms, is now DEM’s heftiest country allocation at 20.3%.

Constituents in DEM’s underlying index are weighed by annual dividends paid, indicating that if Russian dividends deteriorate relative to other emerging markets, the country’s presence in DEM could be reduced.

That is an important factor to consider at time when speculation is high that a combination of economic sanctions by the West and slack oil prices will crimp Russian dividend growth this year. Russia, once a star when it came to emerging markets dividend growth, is expected to see flat payout growth this year. [Sanctions Could Pressure Russia Dividends]

Flat dividend growth by Russian firms will not be the undoing of DEM. Although the South African rand and Brazilian real have traded lower against the U.S. dollar since May 2013, dividend growth in those countries has still been positive in dollar terms, an important factor because South Africa and Brazil combine for nearly 21% of DEM’s weight. [Emerging Markets Dividend ETF Keeps Emerging]

Dividends and Russia also give DEM a value feel. The MSCI Russia Index trades at around five times earnings compared to 13 times for the MSCI Emerging Market Index. Conversely, the WisdomTree Emerging Markets Equity income Index, DEM’s underlying index, trades at 9.46 times earnings, according to issuer data.

Not to mention, DEM’s distribution yield of 4.12% is almost 200 basis points higher than the trailing 12-month yield on EEM.

“EM high-dividend stocks are currently the cheapest part of global equity markets on a dividend yield and P/E ratio basis. But these stocks have high sensitivity to China’s growth rates and oil prices—two unknowns entering 2015. If oil prices rebound, I believe the EM high-dividend payers will be the biggest beneficiaries,” said WisdomTree Research Director Jeremy Schwartz in a research note out last month.

WisdomTree Emerging Markets Equity Income Fund

{kind=link}

Tom Lydon’s clients and Todd Shriber own shares of DEM.