With Monday’s 2.6% drop, the Market Vectors Russia ETF (NYSEArca: RSX) is close to losing all of its modest 2015 gains, but while Russia, a notoriously volatile equity market, is fraught with well-documented risk, some market observers see potential rewards to go along with that risk.

“While prudence cautions against concentrating one’s investments in Russia, current market prices offer alluring risk premiums. The ruble is cheap, interest rates are high, and dividend yields of Russian companies are among the highest in the world,” according to a new research piece by Research Affiliates entitled The Wild, Wild East: Risks and Opportunities in Russia.

Chief among those risks are falling oil prices and a rising risk of a sovereign debt, an offense Russia committed twice last century. Last Friday, Fitch Ratings lowered Russia’s sovereign credit rating to BBB-, the lowest investment grade, with a negative outlook. Fitch previously rated Russian sovereign debt BBB. [Russia ETFs Stung by Fitch Downgrade]

Prior to the Fitch downgrade, speculation was intensifying that Russia was headed for a junk credit rating. On Dec. 23, Standard & Poor’s placed Russia’s sovereign debt on CreditWatch with negative implications, indicating Russia could lose its already tenuous grasp on its investment-grade credit rating.

Investors looking to minimize some of the risk inherent with Russian equities can do so with a broader emerging markets ETF, such as the $350.1 million PowerShares FTSE RAFI Emerging Markets Portfolio (NYSEArca: PXH).

PXH is a fundamentally-weighted ETF focusing on the virtues of book value, cash flow, sales and dividends. Russia is 8.3% of PXH’s weight, making it the ETF’s fifth-largest country allocation. Translation: PXH is overweight Russia by nearly 500 basis points compared to the MSCI Emerging Markets Index.

PXH features an almost 19% energy sector weight with two Russian energy firms found among the ETF”s top 10 holdings. That positions the ETF firmly in the Russia risk/reward scenario.

“Close to 70% of Russian exports are energy related. When energy prices fall, the country’s revenue stream tends to dry up,” according to Research Affiliates.

Russia depends on oil for nearly half of over government receipts, by far the largest percentage of any non-OPEC producer. [Oil’s Fall Drains Frontier ETFs]

Russia’s oil conundrum is well-known. So are its compelling valuations and decent dividends, which have been battle cries of Russia bulls for over two years. Russia’s benchmark Micex Index currently trades at less than half the P/E of the MSCI Emerging Markets Index. Although Western sanctions and lower oil prices are expected to hamper Russian dividend growth this year, the country remains one of the highest-yielding emerging markets. RSX sports a 30-day SEC yield of 2.5%, nearly 50 basis points above the MSCI Emerging Markets Index.

PXH has a trailing 12-month yield of 3.17%, nearly 100 basis points above the MSCI index. Additionally, Russia’s default risk is arguably overstated.

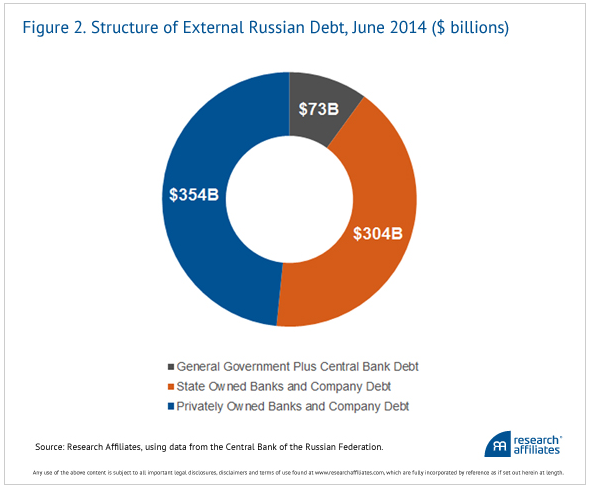

“Russia’s current foreign debt is not large: $731 billion, or about 34% of Russia’s annual GDP. Direct government debt is $73 billion and state-owned banks and corporations owe an additional $304 billion. By international standards this is benign. U.S. external debt is close to 100% of GDP, for example. In consideration of Russia’s $478 billion currency reserves, accumulated over the past decade, it seems absurd to worry about default,” said Research Affiliates. [A Contrarian EM ETF Idea]

Russian Debt

{kind=link}

Chart Courtesy: Research Affiliates