Russia’s oil conundrum is well-known. So are its compelling valuations and decent dividends, which have been battle cries of Russia bulls for over two years. Russia’s benchmark Micex Index currently trades at less than half the P/E of the MSCI Emerging Markets Index. Although Western sanctions and lower oil prices are expected to hamper Russian dividend growth this year, the country remains one of the highest-yielding emerging markets. RSX sports a 30-day SEC yield of 2.5%, nearly 50 basis points above the MSCI Emerging Markets Index.

PXH has a trailing 12-month yield of 3.17%, nearly 100 basis points above the MSCI index. Additionally, Russia’s default risk is arguably overstated.

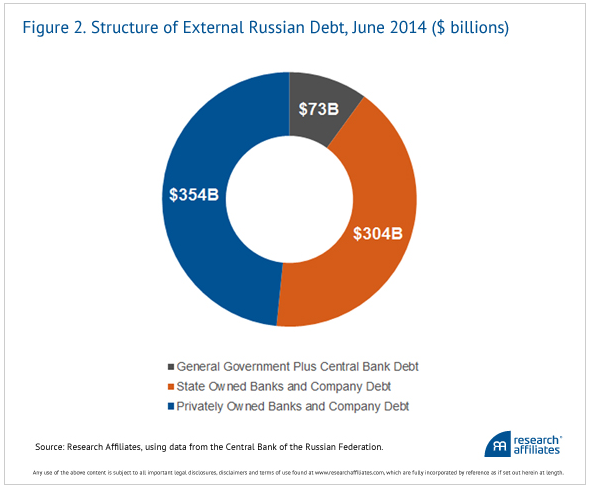

“Russia’s current foreign debt is not large: $731 billion, or about 34% of Russia’s annual GDP. Direct government debt is $73 billion and state-owned banks and corporations owe an additional $304 billion. By international standards this is benign. U.S. external debt is close to 100% of GDP, for example. In consideration of Russia’s $478 billion currency reserves, accumulated over the past decade, it seems absurd to worry about default,” said Research Affiliates. [A Contrarian EM ETF Idea]

Russian Debt

{kind=link}

Chart Courtesy: Research Affiliates