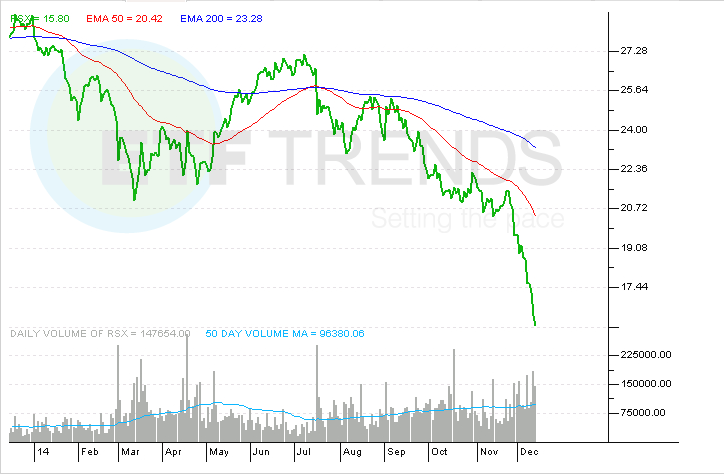

Shares of the Market Vectors Russia ETF (NYSEArca: RSX) are off nearly 9.8% Monday on volume that has already surpassed the average daily turnover on news that the probability of a Russian sovereign debt default is rising.

Underscoring just how tenuous the situation is with Russian equities, RSX is not Monday’s lone offender among Russia ETFs. The SPDR S&P Russia ETF (NYSEArca: RBL), which is off 9.3% while the iShares MSCI Russia Capped ETF (NYSEArca: ERUS) is lower by 9.4%. Of the five worst-performing non-leveraged ETFs to this point in Monday’s trading session, all five are Russia ETFs, or in the case of the iShares MSCI Emerging Markets Eastern Europe Index Fund ETF (NYSEArca: ESR), an ETF with significant exposure to Russian stocks.

Although Russia has $38 billion of dollar-denominated government of which just $6 billion of interest and principal payments is due next year, there concerns linger that Russia is flirting with another financial crisis.

“Last Monday, the probability of a default on the debt of the Russian Federation was ~20%. By the close of business on Friday that jumped all the way up to ~25%. Psychologically, a 1 in 5 probability changed to 1 and 4 likelihood in just five days. That is a big move. The default probability at the time of writing is ~28.5%, a 3.5% jump since last Friday,” said Rareview Macro founder Neil Azous in a research note out today.

Earlier Monday, the careening Russian ruble slid 4% to fresh lows against the U.S. dollar as the American depositary receipts of energy giant Gazprom and Sberbank tumbled. Those stocks combine for 13.7% of RSX’s weight. [Getting it Wrong With Russia ETFs]

Speculation is also rising that Russia will again intervene in the foreign currency market to stem the ruble’s slide, but currency interventions often prove ineffective for any substantial period of time. Additionally, the ruble and Russia ETFs have continued slumping even after the Russian central bank raised interest rates by 100 basis points last week. Over the past week, RSX has plunged 17.4%.

Russia depends on oil revenue for about half of government receipts, the largest percentage of any major non-OPEC producers, which highlights the vulnerability of the ruble and Russian equities to sliding oil prices. Last week alone, the ruble plunged 10%. The United States Brent Oil Fund (NYSEArca: BNO) is off 7.3% over the past week.

Expectations for a near-term rebound in Russian stocks are hard to come by. In fact, some traders are betting more losses are in store. As was reported last Friday, options traders were spotted gobbling up RSX January $12 puts when the ETF was trading over $16. Today, the ETF trades just over $14.20 and at its lowest levels since the first quarter of 2009. [Options Traders See More Declines for Russia ETFs]

Market Vectors Russia ETF

{kind=link}