One of the most prominent themes in the exchange traded funds industry this year has been the proliferation of factor-based funds, a subset of the strategic beta genre that focuses on various investment factors, including size, momentum, quality and value.

While this year’s expansion of factor-based ETFs might be seen as a seen as sign of a new phenomenon, the reality is some of this space’s constituents have been around a few years. That includes the FlexShares Morningstar U.S. Market Factor Tilt Index Fund (NYSEArca: TILT).

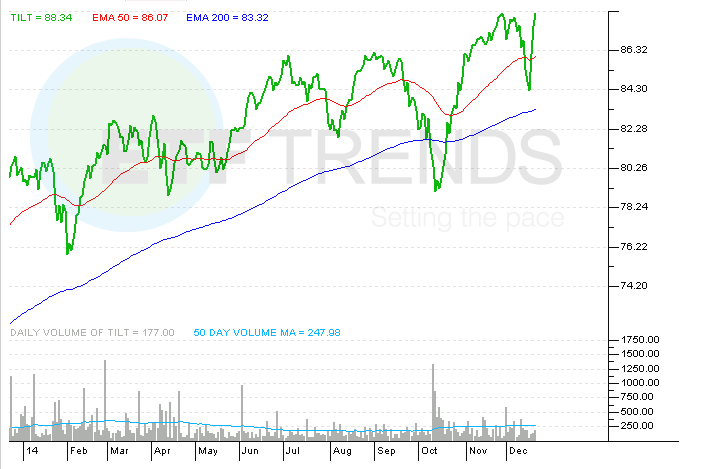

TILT, which debuted in September 2011, quietly hit an all-time high last Friday. TILT tries to reflect the performance of the Morningstar U.S. Market Factor Tilt Index, which provides enhanced exposure to U.S. equities by tilting the portfolio toward long-term growth potential of small-cap and value stocks. [Tilting the Right Way]

“The Morningstar U.S. Market Factor Tilt Index holds 99.5% of the investable U.S. equity universe. By going deeper than other market indexes, the Morningstar Index seeks to capture more of the size premium while still avoiding the very bottom of the market that may have illiquidity issues,” according to FlexShares.

While it would appear that TILT looks to capture the small-cap growth phenomenon so often associated with scores of smart beta ETFs by “tilting” toward smaller stocks. There is double-edged sword here. First, TILT has lagged the S&P 500 this year because small-caps have done the same.

Second, TILT’s small-cap lean is not enough (just 8.3% when factoring in micro-caps) to present excessive risk to investors. The ETF still allocates nearly 60% of its weight to large-caps and a look at TILT’s top 10 holdings reveals a group with littered with value plays including Dow components Exxon Mobil (NYSE: XOM), General Electric (NYSE: GE) and J.P. Morgan Chase (NYSE: JPM).

“The bottom line is that whether markets are efficient, the size and value premiums are well established phenomena that patient investors can take advantage of with portfolios that are tilted toward value-oriented, smaller-cap stocks,” according to Morningstar.

Heading into 2015, a compelling case can be made for TITL taking on a leadership role among broad market ETFs. Although value stocks and ETFs have been in favor with investors for much of this year, the iShares Russell 2000 ETF (NYSEArca: IWM) has recently been picking up the pace, adding 3.3% over the past month.

Smaller companies have been increasing capital expenditures, which would allow them to capitalize off an expanding economy. Small-caps are also raising cash returns to shareholders. Additionally, small-capitalization stocks are more likely to benefit from merger and acquisition activity. [Small Caps Can Rise in 2015]

TILT has established a following with investors. With nearly $759 million in assets under management, the ETF is one of the jewels in the FlexShares lineup. Importantly, $171 million of that total has come into the fund this year. [The Rise of FlexShares]

FlexShares Morningstar US Market Factor Tilt Index Fund

{kind=link}

Tom Lydon’s clients own shares of IWM.