When investing in the commodities market, exchange traded fund investors should understand how the underlying market works to best diversify an investment portfolio and optimize potential returns.

On the recent webcast, The Evolved Commodity ETF Landscape and Diversification Benefits, Kevin Baum, vice president and senior portfolio manager at Invesco PowerShares, points out that commodities act as a diversifier to traditional asset classes. Specifically, over past 15-years, commodities have shown a 0.03 correlation to U.S. bonds, 0.38 correlation to U.S. equities and a 0.51 correlation to developed markets – a 0 reading would correspond to perfectly uncorrelated assets while a 1 reading reflects perfectly correlated assets.

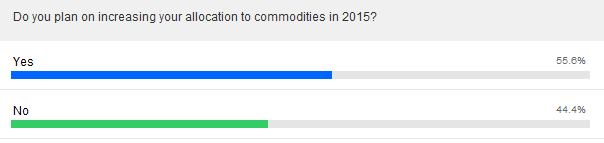

Consequently, since commodities help dampen a portfolio’s volatility, an investor with something like a 48% equity, 32% bond and 20% commodity portfolio would have generated an improved absolute and risk-adjusted return than a portfolio of just equities or one with the traditional 60/40 equity/fixed-income split, Baum said. According to a recent ETF Trends and RIA Database survey, most financial advisors are also looking to increase their commodities positions next year.

{kind=link}

Moreover, once inflation picks up, commodities will act as a good portfolio hedge and potentially outperform equities and fixed-income. Specifically, commodities show a 0.32 correlation to inflation, whereas U.S. stocks h ave a 0.09 correlation and bonds have a -0.18 correlation. The inverse bond correlation makes sense since higher inflation would translate to lower real returns for bonds.

Baum also argues that as we shift into the later stages of a market expansion, commodities will outperform. During the eight business cycles from 1959 to 2013, equities and bonds generated an average 14.5% and 8.6% return, respectively, while commodities rose 6.0%. However, during the late expansion period, commodities outperformed with a 22.7% return, compared to equities falling off 1.7% and bonds rising 1.0%.

“Strong commodity performance has historically followed strong equity markets,” Baum said.

Investors interested in commodities-related ETFs will notice that many track the futures market. ETFs that hold futures contracts generate returns based on spot returns, collateral returns and the roll yield. Spot return refers to the return from selling a commodity for cash, collateral return refers to the returns from holding securities to secure a futures contract, and the roll return refers to the return generated from rolling a maturing contract for a later-dated contract.

If the futures market is in contango, a commodities contract that is set to expire will cost less than later dated contracts. If the futures market is in backwardation, the contract that is set to expire costs more than later-dated contracts. Consequently, it would be in the best interest of a futures-based ETF to limit the negative effects of contango and profit off backwardation.

For instance, the actively managed PowerShares DB Optimum Yield Diversified Commodity Strategy Portfolio (NasdaqGM: PDBC) tries to maximize potential roll returns by selecting the futures contract with the highest implied roll yield in an attempt to maximize the benefits of a backwardated market and minimize losses from rolling in a contangoed market, according to and Lorraine Wang, head of global ETF products & research at Invesco PowerShares.

PDBC is comprised of futures contracts on 14 heavily traded commodities, including aluminum, Brent crude, copper, corn, gold, heating oil, light crude, natural gas, RBOB gasoline, silver, soybean, sugar, wheat and zinc.

Unlike other ETFs that track commodities contracts, PDBC is structured as a 1940s Act Registered Investment Company, Wang added. Consequently, investors will not have to report taxes on a the onerous K-1 form. Instead, the ETF will issue a form 1099-DIV. [PowerShares Kicks the K-1 With New Commodity ETF]

Financial advisors who are interested in learning more about the commodities market can listen to the webcast here on demand.