It is becoming a familiar narrative: Oil prices are slumping, U.S. stocks are rising and energy equities along with the relevant exchange traded funds are reacting more to oil prices than broader market behavior.

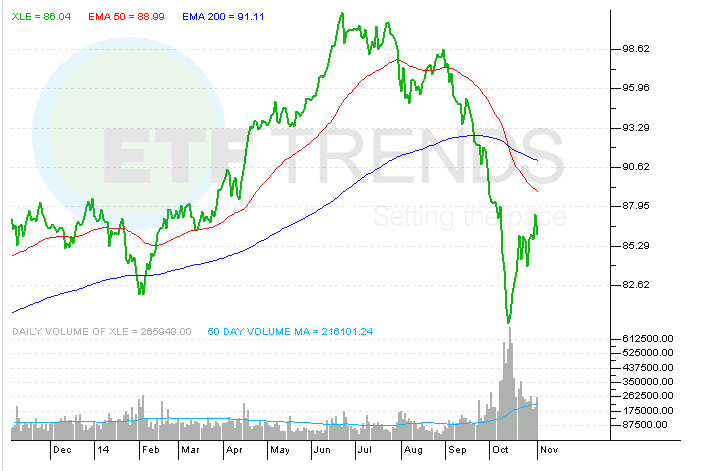

The Energy Select Sector SPDR (NYSEArca: XLE) was once the top performer among the nine sector SPDR ETFs earlier this year. Now, XLE, the largest equity-based energy ETF, is the only one of the nine SPDRs that is in the red year-to-date.

Underscoring just how painful the energy sector’s decline has been of the 20 worst-performing ETFs over the past 90 days, 12 are energy ETFs. Only downtrodden gold miners ETFs are keeping the First Trust ISE-Revere Natural Gas Index Fund (NYSEArca: FCG) and the SPDR Oil & Gas Equipment & Services ETF (NYSEArca: XES) from being among the worst of the worst ETFs over that period. [Natty’s Plunge Plagues This ETF]

However, sentiment surrounding the energy sector is perhaps overly negative and that could be creating a buying opportunity for savvy investors.

Portfolio manager Patrick O’Shaughnessy “said downward oil price moves generally cause broad stock price declines. But those declines are then followed an enduring run-up in prices, averaging 18.94% for all large energy stocks over a one-year time frame,” reports Trevor Hunnicutt for InvestmentNews.

Some investors are nibbling at energy stocks again. XLE has added nearly $333 million in new assets this quarter, a far cry from the time earlier this year when XLE was by far the top asset gatherer among sector ETFs, but still better than the $1.3 billion the fund bled in the third quarter.

Additionally, XLE’s payout ratio of just 32.1% indicates many of the ETF’s 46 holdings are not burdened by their payout and have room for future dividend growth. AltaVista’s P/E estimate for 2014 for the energy sector is 14.8 with a price-to-book ratio of 1.9. Those numbers are estimated to be 13.4 and 1.7 for 2015. [Value With Energy ETFs]

Still, the energy sector faces headwinds. Saudi Arabia, OPEC’s largest producer has not been rattled by lower oil prices and is not stemming production even as oil falls. However, those lower prices are crimping smaller exploration and production companies operating in U.S. shale formations where it is more expensive to extract oil.

Many of those smaller E&P firms are unable to generate free cash, leaving them vulnerable to not only declining oil prices but a potential rise in interest rates as well due to the large amount of high-yield commercial paper issued by these firms. About 15% of U.S. junk bonds hail from energy issuers. [Warnings for Junk Bond ETFs With Big Energy Exposure]

Saudi’s lower price targets are an attempt to push out U.S. shale oil producers, who require a higher oil price to maintain profitable margins. Recently, Citigroup argued that “full-cycle” costs, which include land, infrastructure, well drilling and operating costs, for new shale projects require oil prices of at least $70 to $80 per barrel.

Energy Select Sector SPDR

{kind=link}