Even after a rally that has yen hedged exchange traded funds ranking among the best global ETFs over the past month, Japan remains one of the most discounted developed markets in the world and those compelling valuations could be the catalyst for further upside for Japan ETFs.

At the end of October, the Bank of Japan unexpectedly boosted its annual target for expanding the monetary base to 80 trillion yen from 60 to 70 trillion yen while Japan’s Government Pension Investment Fund, which holds about $1.1 trillion in assets under management, increased its allocation to Japanese and overseas equities to 25% each, up from 12% each, and cut down its domestic bond allocations to 35% from 60%. [BOJ Boosts Japan ETFs]

Those actions ignited a rally in the dollar/yen currency that has the WisdomTree Japan Hedged Equity Fund (NYSEArca: DXJ), Deutsche X-trackers MSCI Japan Hedged Equity ETF (NYSEArca: DBJP) and the iShares Currency Hedged MSCI Japan ETF (NYSEArca: HEWJ) residing as three of the best developed market ETFs over the past month, but even with an average return north of 10% over the past 30 days for those ETFs, those funds hold some inexpensive stocks.

In fact, Japanese stocks are not only discounted relative to other developed markets, but their own history as well, note BlackRock’s Russ Koesterich and Heidi Richardson in new research on Japanese stocks. Valuations are not the only catalysts that could propel Japan ETFs in the coming months.

“We believe that Japan deserves a second look by investors. As noted, it is one of the few bargains out there. But more importantly, there are four catalysts that could support equities over the shorter term: a better-than-expected earnings picture, more share buybacks by Japanese companies, the Japanese central bank expanding its asset purchase program and the potential reallocation by major Japanese pension plans into stocks. In addition, there are some promising signs of reform on the horizon that could also support the longer term case for Japan,” according to Koesterich and Richardson.

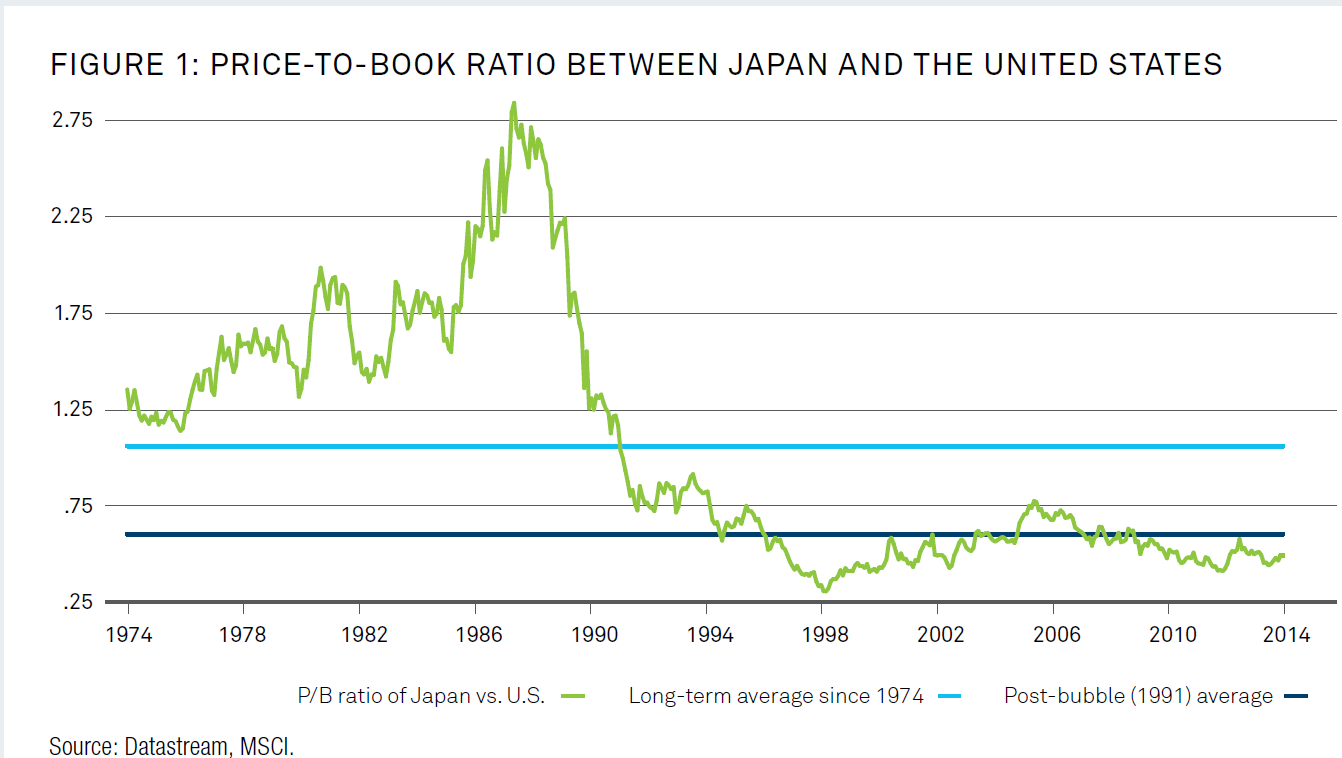

Since 1974, the long-term price-to-book ratio between Japanese and U.S. stocks is around 1.2, but even with a dip below 0.75 since 1991, Japanese stocks are currently deeply discounted compared to U.S. counterparts, according to BlackRock data.

{kind=link}

Chart courtesy: BlackRock

Those attractive valuations coupled with the weak yen are stoking substantial inflows to U.S.-listed Japan ETFs. Prior to the BOJ announcement late last month, HEWJ was a small ETF. Not it has over $220.5 million in assets under management, making it one of the most successful new ETFs to come to market this year. [Big Inflows to Japan ETFs]

One obvious benefit of the weak yen is that it boosts earnings for Japanese exporters, a significant portion of one of the largest equity markets in the world.

“However, Japanese firms have actually surprised to the upside with the April to June earnings season shaping up better than expected. On a year-on-year basis, Japanese corporate earnings have risen 53%, significantly outstripping the share price gain of 13%. For the same period, stocks in the United States and Europe have rallied 18% and 22%, respectively, primarily through multiple expansion with

little or even negative earnings growth Japanese corporate earnings have risen 53%, significantly outstripping the share price gain of 13%. For the same period, stocks in the United States and Europe have rallied 18% and 22%, respectively, primarily through multiple expansion with little or even negative earnings growth,” note Koesterich and Richardson.