A smart-beta indexing approach to international exchange traded fund investments could help diminish volatility in a global equity portfolio and generate better risk-adjusted returns relative to traditional cap-weighted index funds.

On the recent webcast, Beyond Market Cap Investing: Strategic Beta ETFs, J.P. Morgan Asset Management’s Robert Deutsch, Managing Director and Global Head of ETFs, points out that as the ETF market evolved over the past two decades, we are seeing a shift from traditional market cap-weighted broad indices to sophisticated strategies, or so-called smart-beta and strategic-beta indexing methodologies. It has only been over the past five-years or so that strategic-beta index-based ETFs have become more mainstream.

The new breed of smart-beta indices try to address the potential inefficiencies left by market cap-weighted indices. Timothy Devlin, Executive Director and Client Portfolio Manager on Global Equities Team, said that market cap-weighted indices may overweight some sectors, which could expose an investor to greater risks. For instance, Devlin singles out the heavy overseas exposure to the financial sector, notably where risk is highly concentrated in continental European financials.

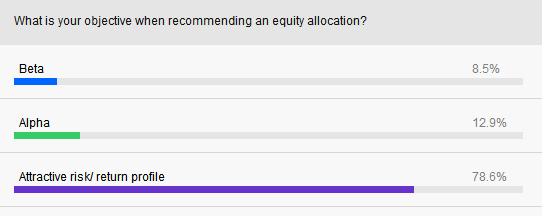

Consequently, Nigel Emmett, Managing Director and Senior Client Portfolio Manager for Global Equities Team, argues that a passive replication of a cap-weighted index may be a flawed strategy. Instead, the use of multiple beta factors could help explain alpha and capture diversified, risk-adjusted returns. Many financial advisors are seeking out new investment strategies that provide attractive risk-adjusted returns, according to a recent ETF Trends survey.

{kind=link}

“Research has uncovered other sources of systematic risk that help explain more of the equity market return, taking away from what some had referred to as alpha,” Emmett said. “Now multiple betas can be accessed cheaply through smart beta ETFs.”