China makes up a large chunk of the global marketplace, but many investors may be unintentionally underweighting their exposure to the country. With an exchange traded fund, anyone can access a diversified group of Chinese securities.

On the recent webcast, How to Take Advantage of the Expanding Chinese Equity Opportunity, Jared Rowley, research strategist at SSgA, and Matthew Bartolini, research strategist at State Street Global Advisors, point out that the Chinese economy is now the world’s second largest economy and its equity market is the third largest, behind the U.S. and Japan.

However, many remain underexposed to the Chinese market while maintaining their U.S. bias. Consequently, investors could miss out on a significant growth opportunity.

“We believe Emerging Market equities are a broad and evolving asset class and have taken a more prominent position in global equity market,” Rowley said.

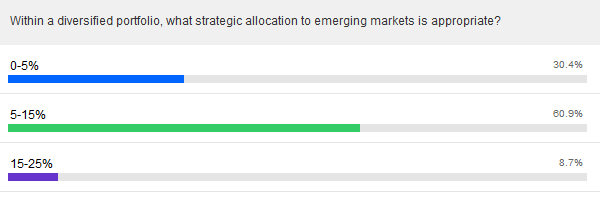

According to a recent ETF Trends and RIA Database survey of financial advisors, the majority of respondents point to a 5% to 15% allocation toward the emerging markets.

{kind=link}

As the country matures, Beijing has implemented greater reforms to liberalize the market. With more people taking an interest in the emerging market, investors may have noticed that performance and correlations vary among China share classes.

For instance, the Chinese A-shares, or securities incorporated in Mainland China that are listed on the Shanghai or Shenzhen stock exchange and traded in Renminbi, make up the largest portion of the Chinese equity market. [Issuers Want in on China A-Shares ETF Party]

U.S investors may be more familiar with the H-share class, which are China securities incorporated in the Mainland but listed on the Hong Kong stock exchange and denominated in the Hong Kong dollar. There are also N-shares that include China securities and ADRs listed on the NYSE, NASDAQ and AMEX. For example, some of the more well known recent Chinese equity IPOs include N-shares like Alibaba Group (NasdaqGS: BABA) and JD.Com (NasdaqGS: JD).

Additionally, Red-Chips include state-owned companies outside Mainland China that are listed on the Hong Kong stock exchange and P-chips cover China securities of non-government owned companies incorporated outside the Mainland that are listed in Hong Kong as well.

The strategists also note that the share classes exhibit varying levels of risk and returns. For instance, China A-shares have the highest returns since 2005, along with the lowest beta and correlation to the MSCI Emerging Markets index. Moreover, China H-shares and Red-Chips include larger companies, whereas China A-shares and P-Chips tilt toward companies with greater expected profitability.

The SPDR S&P China ETF (NYSEArca: GXC), which tries to reflect the performance of the S&P China BMI Index, includes a diverse breakdown of varying Chinese share classes, including 45% H-shares, 18% Red-Chips, 25% P-Chips and 12% N-shares. The China ETF also includes heavy exposure to financials at 30.1% of the overall portfolio, followed by tech names at 21.9%.

GXC could also eventually be home to Alibaba. Prior to the company’s September initial public offering, S&P Dow Jones Indices has confirmed that Alibaba will screen for inclusion in the S&P China BMI. [S&P Indices to Include Alibaba]

Financial advisors who are interested in learning more about investing in China can listen to the webcast here on demand.