Some would argue there is almost no such thing as an “easy trade,” but over the past couple of year, shorting volatility has come close.

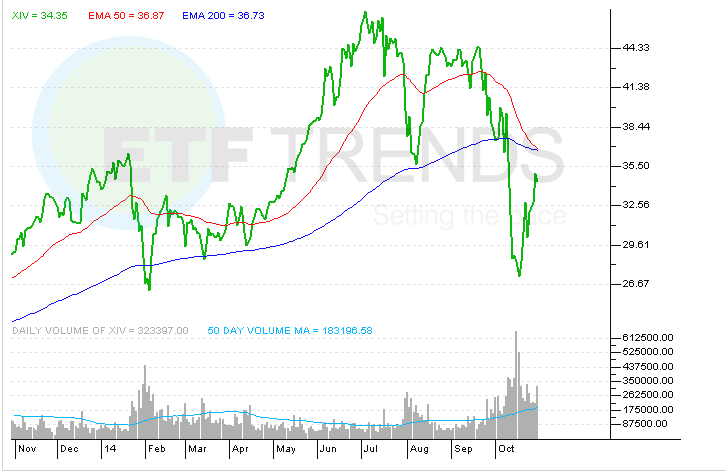

Over the past two years, the VelocityShares Daily Inverse VIX Short-Term ETN (NYSEArca: XIV) and the VelocityShares Daily Inverse VIX Medium Term ETN (NYSEArca: ZIV) have each more than doubled. At the close of U.S. markets on Oct. 28, XIV was a $1.4 billion ETN. ZIV, though far smaller, can at least say it is well above the $100 million in assets under management mark with nearly $144 million in assets. [Shorting Volatility Works With These ETNs]

XIV “ has more than doubled in size since the start of October. It crossed over the $1 billion mark for the first time ever on Oct. 16 and peaked on Oct. 21, at $1.33 billion, according to Morningstar,” reports Chris Dieterich for Barron’s.

If some hedge funds are right, the pleasantries afforded to short volatility ETNs could end in sour fashion. Just as some traders and investors are rushing to short volatility with XIV, ZIV and rival products, hedge funds are upping their bets on increased volatility.

“For the first time since 2011, the balance of futures owned by hedge funds and other large speculators on the Chicago Board Options Exchange Volatility Index represents wagers that equity turbulence will increase,” reports Callie Bost for Bloomberg, citing Commodity Futures Trading Commission data.

That could be a sign those daring enough to be involved with volatility ETNs should not be deceived by inflows to XIV and ZIV and departures from long volatility ETNs such as the iPath S&P 500 VIX Short Term Futures ETN (NYSEArca: VXX).

In just the past week, VXX has bled $414 million while the ProShares Short VIX Short-Term Futures ETF (NYSEArca: SVXY) has lost over $34 million.

However, there have been no departures from or inflows to the double-leveragedVelocityShares Daily 2X VIX Short-Term ETN (NYSEArca: TVIX) while the ProShares VIX Short-Term Futures ETF (NYSEArca: VIXY) added nearly $11 million over the past week.

The VIX typically moves higher when stocks plunge. Traders would turn to S&P 500 options to protect their portfolios against any sudden dips. Investors should also be aware that VIX-related ETFs are designed to track CBOE Volatility Index futures contracts, not the VIX spot price. Consequently, traders can lose money on this trade when longer-dated contracts are more expensive than the front-month contract, or when markets are said to be in “contango.” [VIX ETNs Love Volatile Markets]

VelocityShares Daily Inverse VIX Short-Term ETN

{kind=link}