Simply put, September was a dreadful month for emerging markets stocks and exchange trade funds. The Vanguard FTSE Emerging Markets ETF (NYSEArca: VWO) and the iShares MSCI Emerging Markets ETF (NYSEArca: EEM), the two largest emerging markets ETFs by assets, posted an average September slide of 8%.

Illustrating just how bad the ninth month of the year was for emerging markets equities, that 8% drop seems tame by comparison to the woes experienced by some single-country ETFs. For example, the three worst non-leveraged ETFs over the past month are all Brazil funds, “led” by a 22.2% drop for the iShares MSCI Brazil Capped ETF (NYSEArca: EWZ), meaning the largest Brazil ETF is now in a bear market. [Brazil, Russia ETFs Nearing Bear Markets]

Still, eight developing markets as measured by the S&P Global Broad Market Index were able to post positive gains last month. The best of the worst was India, easily the top performer among the four BRIC nations this year.

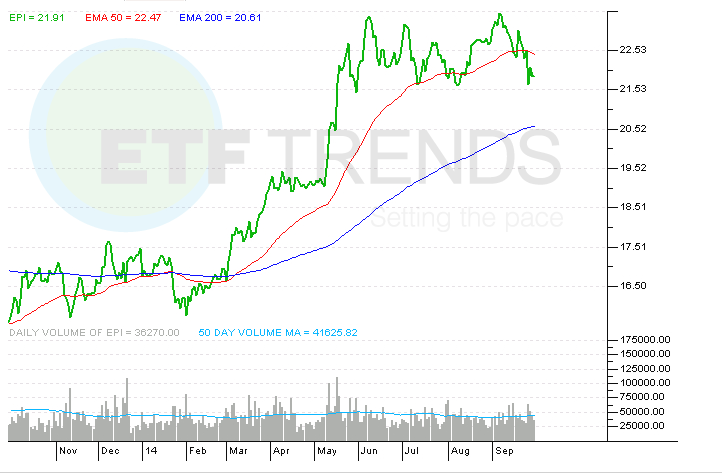

Yes, the WisdomTree India Earnings Fund (NYSEArca: EPI), the largest India ETF, was off 5.2% last month, but that is not even a quarter of the decline experienced by EWZ . EPI also outpaced the iShares China Large-Cap ETF (NYSEArca: FXI) in September. EPI’s recent relative strength could be a sign the ETF and its India counterparts are ready to rally into yearend.

One thing to remember about EPI is that while Indian are somewhat pricey compared to broader emerging markets benchmarks, the ETF’s weighting methodology ensures it is less sensitive to elevated valuations than cap-weighted rivals.

“The WisdomTree India Earnings Index (WTIND) seeks to provide exposure to the profitable core market of India’s equities but to do so while maintaining sensitivity to valuation. To help achieve this, WisdomTree weights companies in the Index by the profits they generate, rather than their market cap, and rebalances back to profitability on an annual basis,” wrote WisdomTree Associate Director of Research Christopher Gannatti in a note out Wednesday.

Gannatti points out that the most profitable companies in EPI’s selection universe will occupy the largest weights within the ETF while stocks that have been recent tears see their weights pared in favor of making room for laggards that have the potential to be the next batch of Indian leaders. That methodology helps EPI’s lineup appear inexpensive relative to other India benchmarks.

“WTIND’s P/E ratio is approximately 14.0x—reflecting the 2014 Index screening—i.e., almost 25% lower than the 18.4x P/E ratio of the S&P CNX Nifty Index (Nifty Index) or the 18.6x P/E ratio of the MSCI India Index,” said Gannatti.

The nearly $2 billion EPI currently allocates 24.2% to the financial services sector, about 550 basis points more than ETF’s energy allocation, its second-largest sector weight.

EPI’s financial services exposure could prove beneficial after S&P recently raised the country’s credit outlook, reducing the prospect of a downgrade to junk status any time soon, indicating higher borrowing costs are not an imminent threat for Indian firms. [India ETFs Look Worthy After S&P Outlook Boost]

India, like BRIC-mates Brazil and Russia, has a sovereign rating of BBB-, S&P’s lowest investment grade. Additionally, the improved outlook on Indian bond securities helps diminish the risk of a major sell-off once the U.S. hikes interest rates. Global investors pulled $8 billion out of rupee-denominated bonds last year after the Federal Reserve began tapering its bond purchasing program. [Emerging Asia ETFs Can Shake Off Effects of Rising U.S. Rates]

WisdomTree India Earnings Fund

{kind=link}

Tom Lydon’s clients own shares of EEM.