High-yield bond exchange ETFs have recently endured investors’ wrath. Whether it has been plummeting equity markets or concerns the Federal Reserve will raise interest rates, junk bond ETFs been cast aside by some investors.

Conversely, some investors are bargain-hunting with high-yield debt, framing the recent sell-off as a buying opportunity because there have been no significant changes to high-yield fundamentals and no erosion to credit quality. [Investors Eye Cheap Junk Bond ETFs]

Moody’s Investors Service has pointed out that default rates remain low, with 1.85% of U.S. junk-rated companies defaulting in the year ended Aug. 31, compared to 14.1% at the end of 2009.

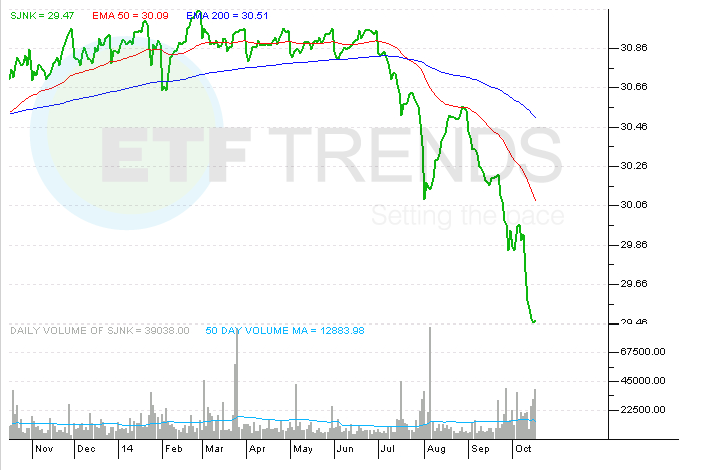

Although 10-year Treasury yields have tumbled 16.2% in the past month, some investors are still forecasting higher interest rates in 2015. If that scenario comes to pass, high-yield bond ETFs with lower durations, such as the SPDR Barclays Short Term High Yield Bond ETF (NSYEArca: SJNK), could come into style.

SJNK has a modified adjusted duration of just 2.5 years compared to 4.28 years on the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEArca: HYG). SJNK’s duration compares favorably with the broader high-yield ETF spectrum, indicating the ETF could prove durable for yield seekers even if the Federal Reserve does raise interest rates.

“We also continue to expect US growth to accelerate in 2015. Strong economic growth has historically not been accompanied by widening credit spreads. As we believe the recent sell-off is sentiment driven, investors may find this to be an opportunity to access a favorable income stream with muted interest rate risk,” said State Street Global Advisors Vice President and head of research Dave Mazza in an email to ETF Trends.

Investors have already shown they will depart longer-duration junk bond ETFs in favor of a fund like SJNK, which sports a 30-day SEC yield of 5.3%. In the first four months of 2014, as speculation increased the Fed would hike rates soon after the end of quantitative easing, SJNK added over $1 billion in new assets while HYG and the SPDR Barclays High Yield Bond ETF (NYSEArca: JNK) lost $2.1 billion and $444 million, respectively. [Short Duration High Yield Bond ETFs are in Style]

Looking forward, a stronger U.S. dollar could benefit SJNK, notes Mazza.

“Rising U.S. rates and accelerating economic growth is bullish for the dollar. We expect the dollar to strengthen against the Australian dollar, British pound and euro over the next 12 months. As the credits in SJNK are denominated in USD, they will not be directly impacted by the strength of the dollar,” he said.

SJNK holds 506 bonds, over 77% of which are rated BB or B. SJNK also offers investors a liquidity advantage, a trait that should not be underestimated when considering that liquidity is usually on the tips of critics’ tongues when question junk bond ETFs.

“Given the recent market volatility, liquid exposure is a must. SJNK tracks an index that is focused on exposure to the more liquid segments of the short term high yield market, holding issues with more than $350M of face amount outstanding and maturities of less than 5 years,” said Mazza.

Mazza adds that there is also a highly liquid secondary market for the bonds found in SJNK and that that liquidity can actually increase even as volatility rises. SJNK’s holdings’ “ratio of secondary market volume to primary market volume during the volatile month of September was 2.7x, which is higher than the since inception average,” he said.

SPDR Barclays Short Term High Yield Bond ETF

{kind=link}

Tom Lydon’s clients own shares of HYG and JNK.