Experienced dividend investors know the utility of adding some international holdings to their income portfolios, whether by way of individual stocks or exchange traded funds.

The explanation is straight forward: Ex-U.S. developed market dividend payers often feature larger yields than their U.S. counterparts, an assertion proven by comparing large- and mega-cap dividend stocks from familiar dividend sectors such as consumer staples, energy, financial services and telecommunications.

The PowerShares International Dividend Achievers Portfolio (NYSEArca: PID) is a compelling and conservative avenue for income investors looking for some international exposure.

PID, which turns nine years old this month, tracks the NASDAQ International Dividend Achievers Index, which is similar to other dividend achievers indices that benchmark popular U.S.-focused dividend ETFs, such as the PowerShares Dividend Achievers Portfolio (NYSEArca: PFM) and the Vanguard Dividend Appreciation ETF (NYSEArca: VIG).

However, stocks that find homes in PFM and VIG have dividend increase streaks of at least 10 years. PID requires five consecutive years of higher payouts. [A High Achieving Dividend ETF]

PID’s conservative posture comes by way of a 29.1% weight to U.S. stocks, indicating investors are not incurring significant geopolitical risk with this ETF. The U.S. is by far the world’s largest dividend market, but PID does feature ample exposure to other renowned dividend markets.

For example, the U.K. is PID’s third-largest country allocation with a weight of 17%. The U.K. is Europe’s largest dividend market and British listed companies paid $102.1 billion in dividends last year, and since 2009 have paid roughly $441 billion,” according to the Independent. [European Dividends are Rising]

Canada, a credible dividend market in its own right, is PID’s second-largest country weight at 19.2% and an important contributor to PID’s trailing 12-month yield of 3.04%. That is more than 60 basis points above the current yield on 10-year U.S. Treasuries.

The utility of Canadian exposure in PID shines through in the ETF’s telecom and energy sector weights. The average dividend yield on Canadian telecom firms BCE (NYSE: BCE), Rogers Communications (NYSE: RCI) and Telus (NYSE: TU) is 4.43%. Dow component Verizon (NYSE: VZ) sports a dividend yield of 4.2%. Those Canadian stocks combine for over 6% of PID’s weight. [Attractive Yields With Global Dividend ETFs]

PID’s international health care holdings (the sector is 11.4% of the ETF’s weight) also represent an important drive of the fund’s yield. Consider this: PID’s top-three holdings from that sector are GlaxoSmithKline (NYSE: GSK), Sanofi (NYSE: SNY) and Novartis (NYSE: NVS). The average dividend yield on those stocks is 4% compared to an average yield of 3.17% for Johnson & Johnson (NYSE: JNJ), Pfizer (NYSE: PFE) and Merck (NYSE: MRK).

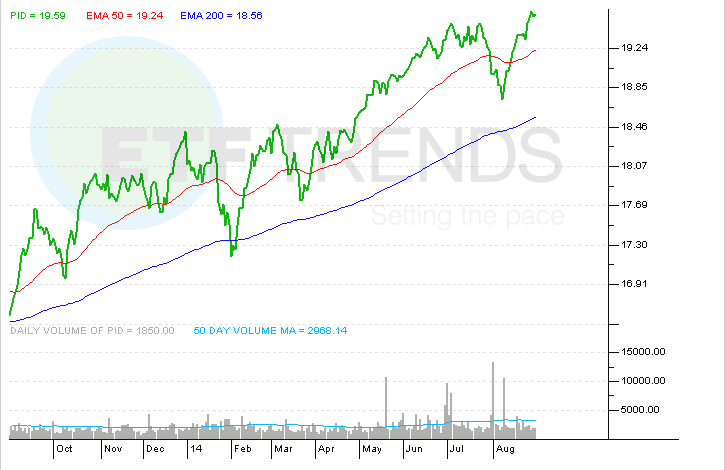

Up 3.2% since we profiled the ETF in late May, PID is up 8.3% year-to-date and after touching another 52-week high Monday, the fund finds itself within shouting distance of $20. PID has not closed above that level since May 2008.

PID’s two largest emerging markets exposures are China and Russia. China is the largest emerging markets dividend payer in dollar terms while Russia is one of the fastest-growing developing world dividend destinations because of government policy that is actively attempting to force cash-rich companies there to pay bigger dividends.

Some investors are taking note of the advantages of ex-U.S. developed market dividend stocks and PID. The ETF climbed more than 3% last month while adding $60.6 million in new assets, a number surpassed by only two other PowerShares ETFs — the PowerShares QQQ (NasdaqGM: QQQ) and the PowerShares FTSE RAFI US 1000 Portfolio (NYSEArca: PRF), according to issuer data.

PowerShares International Dividend Achievers Portfolio

{kind=link}

Tom Lydon’s clients own shares of QQQ.