We scanned through the “Alternatives” category of U.S. listed ETPs, and the list is top heavy “Volatility” linked products in terms of the largest ETPs in terms of asset size, but there are a few non-vol linked products among the top ten funds as well.

One example is QAI (IQ Hedge Multi-Strategy Tracker, Expense Ratio 0.75%) which we have covered in this piece in the recent past, and that fund has gathered a notable $856 million now in assets under management since its 2009 inception.

When finely categorizing QAI, most services list the product not only in the greater realm of “Alternatives” but also under “Hedge Fund” ETFs. State Street also has an entry in this space that is not as well known as QAI, having launched in 2012, RLY (SPDR Multi-Asset Real Return ETF, Expense Ratio 0.70%).

The fund has managed to raise about $178 million since inception, and unlike most State Street funds which are straight up passive index (beta) products, is an “actively managed, tactical approach to real assets in one trade” according to fund literature. Real assets typically include precious metals, commodities, real estate, and land with tangible agricultural, or fuel energy/mining value.

Like other “Hedge Fund” ETFs, RLY invests in other ETFs, and we currently see top end portfolio exposure to the following: GNR (SPDR S&P Global Natural Resources, Expense Ratio 0.40%, >30.8% weighting), DBC (PowerShares DB Commodity Index Tracking Fund, Expense Ratio 0.93%, >17.8% weighting), IPE (SPDR Barclays TIPS, Expense Ratio 0.18%, >13.6% weighting), RWR (SPDR Dow Jones REIT, Expense Ratio 0.25%, >11.6% weighting), and RWX (SPDR Dow Jones International Real Estate, Expense Ratio 0.59%, >9.4% weighting).

The usage of other State Street ETFs is notable throughout the portfolio, with some PowerShares and Market Vectors peppered in in some places. With some “Hedge Fund” and “Alternatives” ETPs, trade execution can sometimes be a challenge thanks to lower daily trading volumes and sometimes unrealistically wide visual bid/ask spreads.

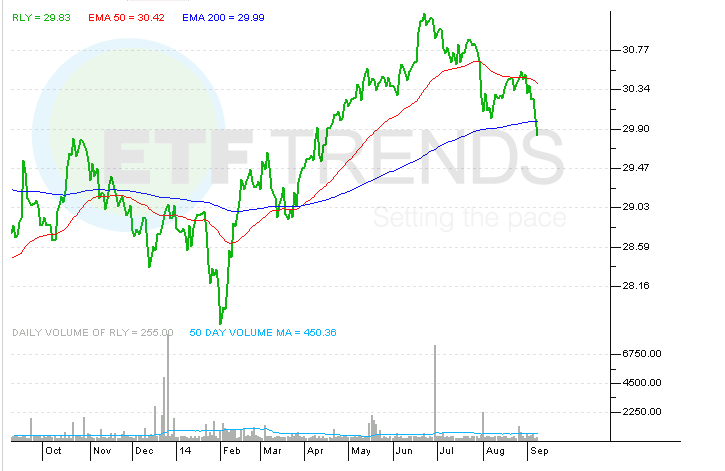

This is really not the case with RLY (and QAI for that matter), as both have bid/ask spreads that are only a few cents wide typically, with ample screen liquidity in most cases as well available, at least to the extent that most investors will not take issue with the consideration of making larger allocations to the funds. RLY has had a hard time in the short term, down three straight sessions and nearing its 200 day MA for the first time in recent recollection.

SPDR SSgA Multi-Asset Real Return ETF

{kind=link}

For more information on Street One ETF research and ETF trade execution/liquidity services, contact Paul Weisbruch at pweisbruch@streetonefinancial.com.

Street One Financial is an educational/research firm utilizing the Broker Dealer services of Precision Securities, a FINRA registered Broker/Dealer.